Building & Lumber Subcategory Breakdown

Building & Lumber Subcategory Breakdown. Data-backed consumer insights and market analysis from YipitData's research team.

As the building and lumber industries continue to evolve and shift in the post-pandemic era, examining underlying subcategory trends is more important than ever. Understanding what retailers are positioned well and growing in important subcategories can give brands a competitive advantage.

In 2Q23, lumber & composites accounted for 23.8% of building & lumber category GMV, followed by fasteners at 9.8%, doors at 7.2%, asphalt, concrete & masonry at 6.2%, and vinyl flooring at 5.3%.

United States | Online + Offline Sales | 3Q21 - 2Q23

Among online and offline home improvement retailers, consumers have increased spend on fasteners, doors, and asphalt, concrete & masonry, while spending less on lumber and vinyl flooring. While fasteners and lumber have historically trended similarly in year-over-year growth, the fasteners subcategory separated itself in 4Q22, and has seen consistently positive year-over-year growth since 4Q21.

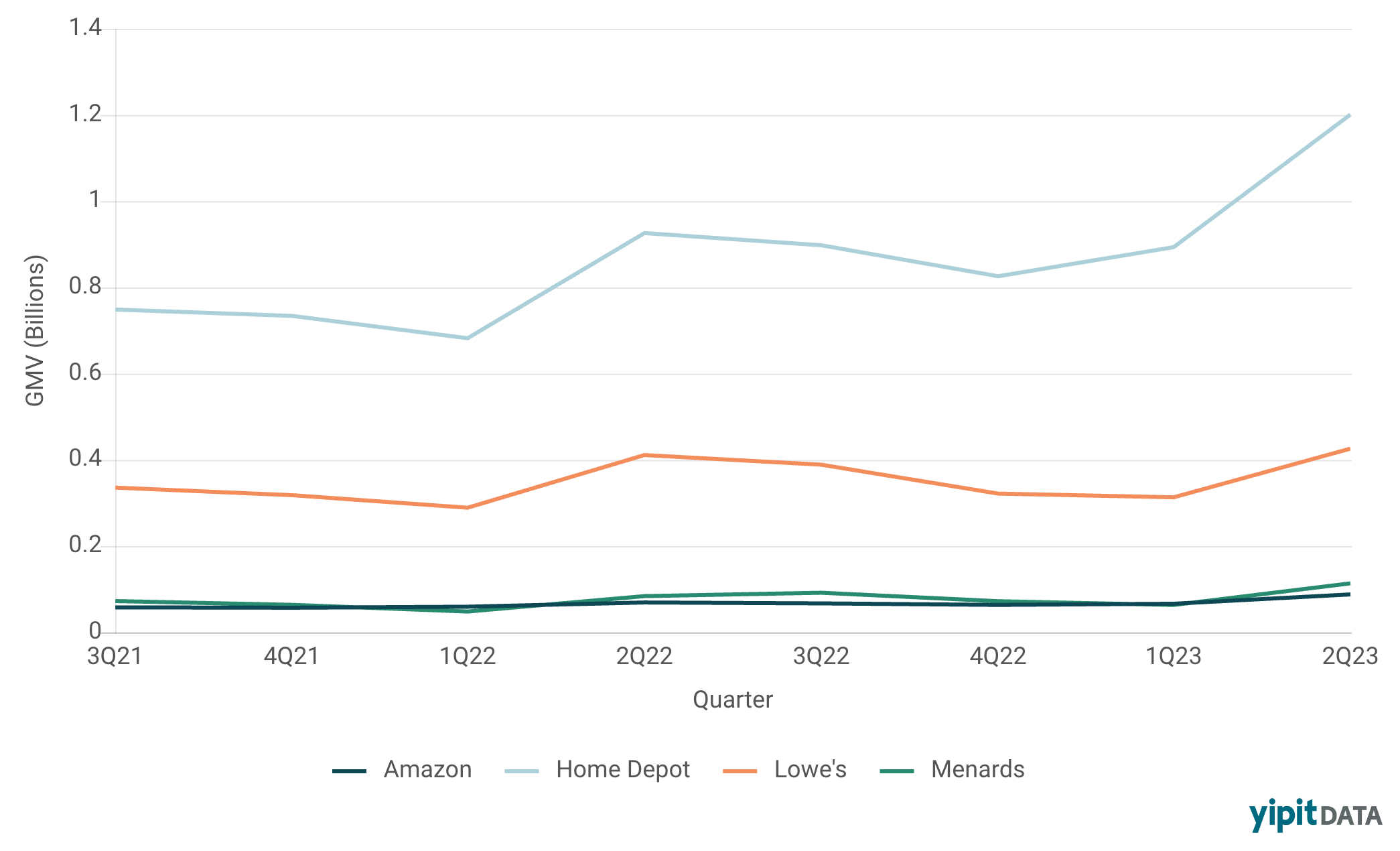

Focusing on the rapidly expanding fasteners space, Home Depot has held a strong position, outperforming Lowe’s and maintaining a dominant market share (65.7% in 2Q23). Menards (6.2% in 2Q23) and Amazon (4.8% in 2Q23) and have been neck and neck as the third and fourth largest market share players in the space.

United States | Online + Offline Sales | 3Q21 - 2Q23

While all four players in the fastener space have seen consistently positive year-over-year GMV growth since 2Q22, Home Depot has managed to do so as the existing market share leader by leveraging its strong reputation and wide product coverage to attract a large range of consumers.

.png)

United States | Online + Offline Sales | 3Q21 - 2Q23

Sources: Email Receipt Data, Physical Receipt Data

Interested in which products and brands are driving fastener and other subcategory growth at Home Depot, Lowe’s, Menards, and Amazon? Fill out the form to get started.

Speak to our Insights team

.svg)