Three AI & Software Companies Losing Momentum

Lavender AI, Sketch, and Workable are losing customers. See what YipitData’s B2B spend data reveals about software consolidation and buyer behavior.

Customer declines can be just as revealing as customer growth. Our latest B2B spend data highlights Lavender AI, Sketch, and Workable — three AI and software companies showing signs of slowing momentum as buyers consolidate tools, reassess spending, and shift toward new workflows.

While much of the software conversation focuses on identifying the next breakout company, every shift in buyer behavior creates two sides of the story: winners gaining momentum and vendors losing it.

This week, we reviewed the latest spend data from 1,300+ businesses to identify companies where momentum is slowing or reversing. Three companies stood out: Lavender AI, Sketch, Workable.

The group spans sales AI, recruiting software, design software, and marketing technology, but the common thread is the same: these are categories where buyers appear to be reassessing solutions, consolidating workflows, or shifting budget toward newer platforms.

The companies operate in very different categories, but the underlying themes are surprisingly similar. Buyers appear to be consolidating tools, reevaluating point solutions, and increasingly favoring broader platforms over standalone products.

Key Takeaways

- Not all AI solutions are winning. Lavender AI shows the most negative trend among this group, with total observed customers falling ~30% over the last 6M and all enterprise customers churning off by early 2026.

- Mature software categories are showing consolidation pressure. Workable and Sketch are not collapsing, but each is below recent customer peaks — suggesting ATS, design, and martech buyers may be pruning vendors or reassessing ROI.

- Switching activity will determine whether this is normal volatility or real competitive share loss and who might benefit. Customer declines are only the first signal.

- The next question is where churned customers went – email me at jenny@yipitdata.com if you want to see.

Data Highlights

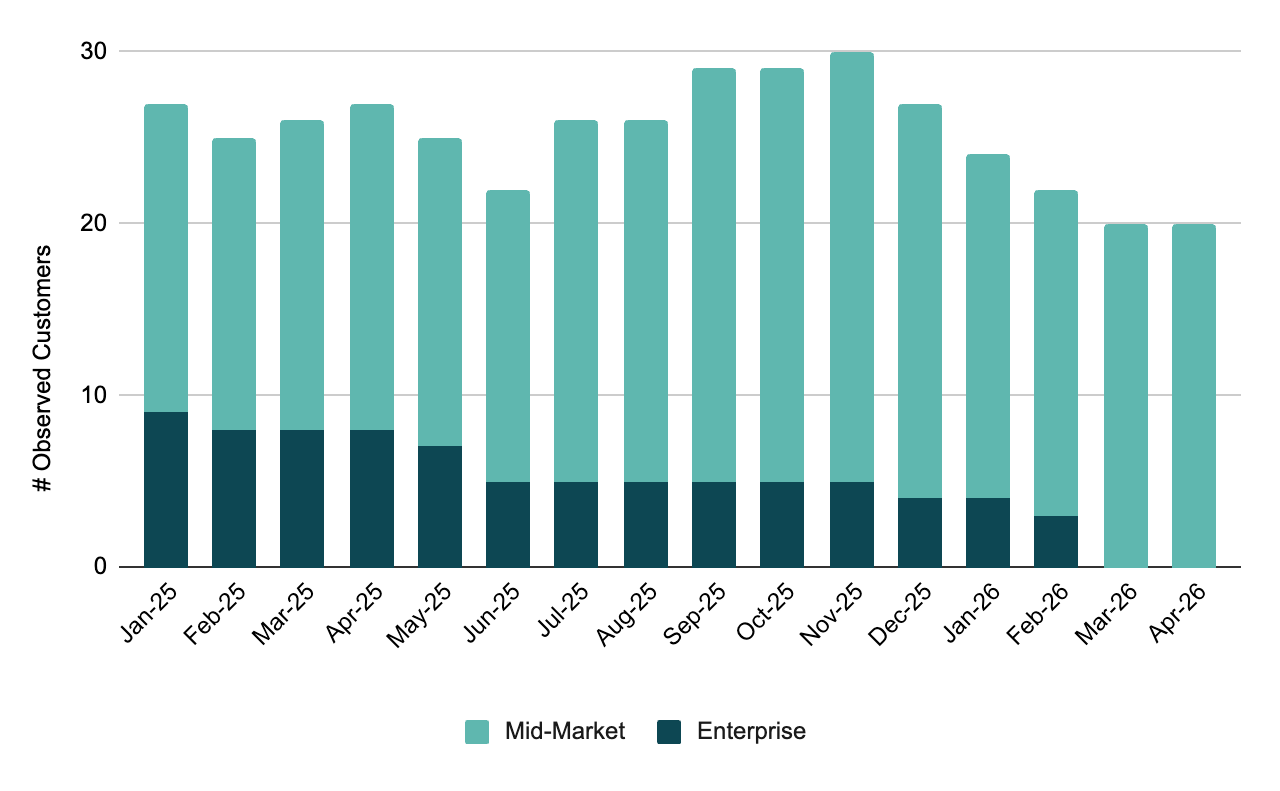

Lavender AI

Last Raised $13M Series A in Feb'23 | Headcount +29% Y/Y over last year (+2% in last 6M)

AI Sales Assistant | Lavender AI provides an AI-powered sales email assistant that helps go-to-market teams write, score, personalize, and improve outbound emails.

Lavender sits in a crowded sales AI category where many tools are competing to automate email writing, prospecting workflows, and rep productivity. The customer decline suggests Lavender may be struggling to sustain adoption as sales teams consolidate tools or shift spend toward broader GTM platforms.

What B2B data shows:

- Observed customer growth inflected negatively in late 2025, declining ~30% over the last 6M

- Enterprise customer count fell to zero in the latest two months, after showing visible adoption throughout 2025

- Mid-Market customers have been more resilient, but total customer momentum has clearly turned negative

This data seems to indicate that sales AI point solutions may be struggling to retain customer attention as buyers consolidate around broader GTM platforms.

Is Lavender AI churn benefiting core GTM platforms like ZoomInfo, Gong, and Outreach? How many have decided to shift budget over to Clay? Email me at jenny@yipitdata.com to find out.

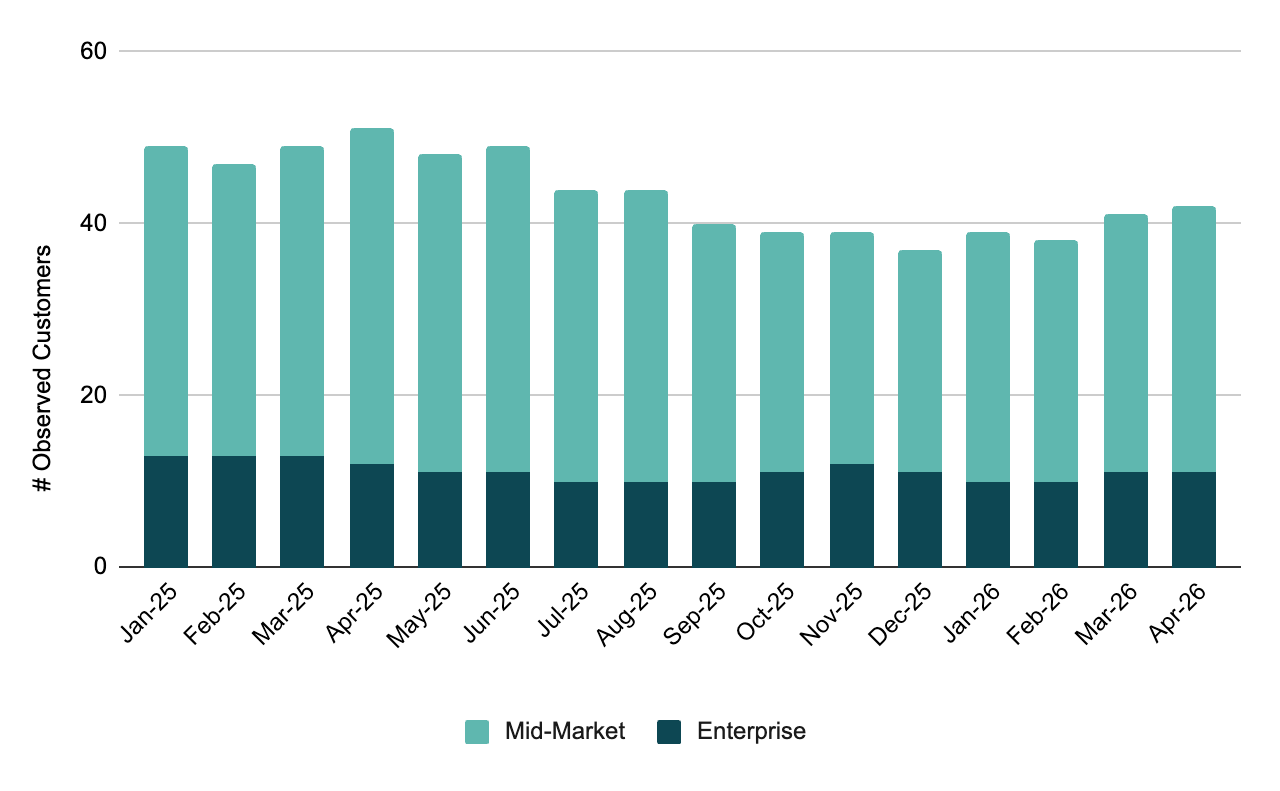

Sketch

Last raised $20M Series A in Mar ‘20 | Headcount +2% Y/Y over last year (+0% in last 6M)

Design Software | Sketch provides a collaborative design platform for digital product design, prototyping, developer handoff, and design systems.

Sketch remains a meaningful design-tool incumbent, but customer count remains below early-2025 levels. The company likely faces continued pressure from Figma, Canva, and AI-native design workflows that are reshaping how teams create and collaborate on visual assets.

What B2B data shows:

- Sketch bled customers in the back half of 2025, with observed customer counts declining 25% over the period

- Customer count has modestly recovered in recent months, though still ~15% below peaks in early 2025

- Enterprise customers have been relatively stable, while Mid-Market customers have driven most of the volatility

In design and martech, mature incumbents appear more exposed to category disruption from collaborative, AI-native, and workflow-consolidation tools.

Are Sketch customers consolidating around Figma, or experimenting with newer AI-native design tools? Email me at jenny@yipitdata.com to find out.

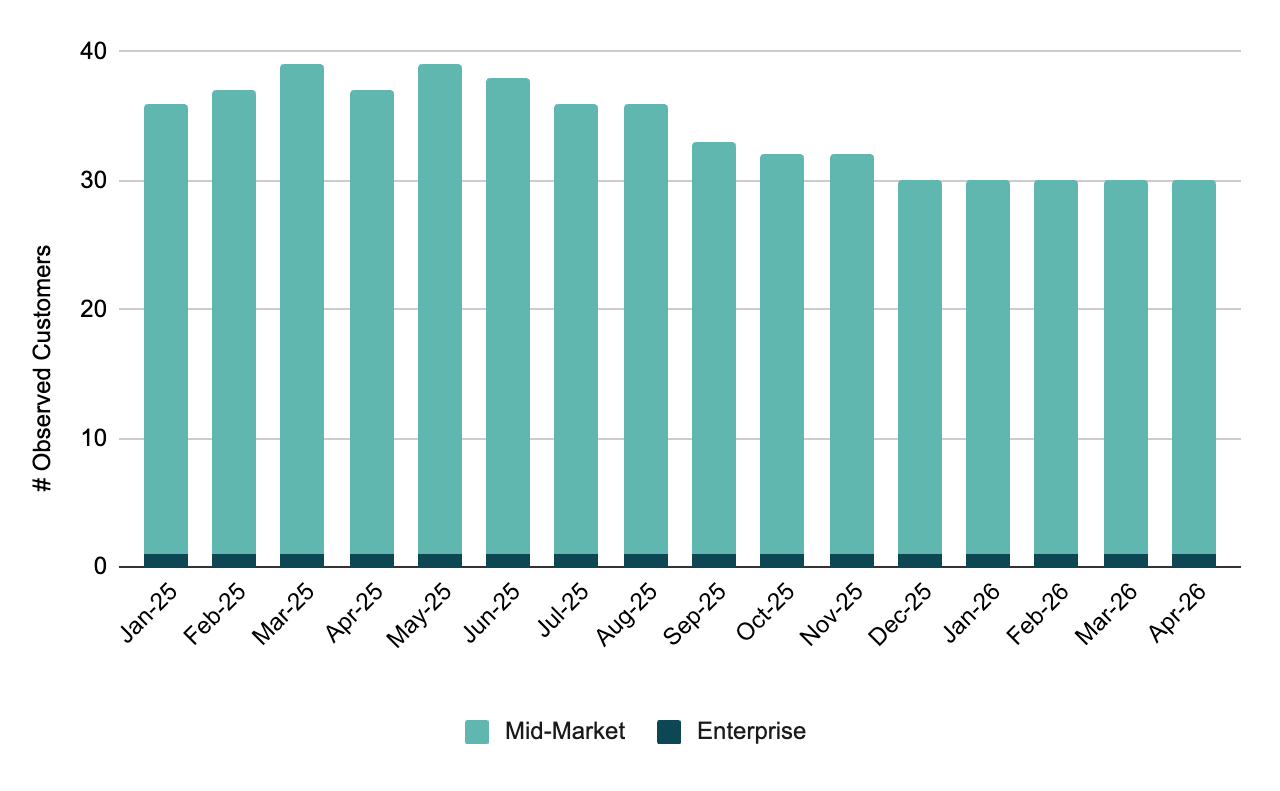

Workable

Last raised $50M Series C in Nov ‘18 | Headcount +13% Y/Y over last year (+6% in last 6M)

Recruiting Software / ATS | Workable provides recruiting and HR software, including applicant tracking, candidate sourcing, onboarding, employee management, and hiring workflows.

Workable is a mature ATS platform in a crowded category. A declining-to-flat customer count could indicate hiring softness, competitive pressure from Greenhouse / Lever / Ashby / BambooHR, or customers consolidating recruiting workflows into broader HR systems.

What B2B data shows:

- Observed customers are down ~20%+ from 2025 peak levels

- Customer growth has been flat in 2026, with ~0% growth from Dec ’25 to Apr ’26

- Minimal Enterprise presence in our panel suggests Workable has not meaningfully offset Mid-Market weakness with upmarket expansion.

In recruiting software, hiring softness and HR-suite consolidation may be weighing on standalone ATS vendors.

Which ATS vendors are capturing Workable churn? Is Greenhouse or Ashby the main beneficiary? Email me at jenny@yipitdata.com to find out.

What We’re Watching Next

The biggest question is whether these are temporary customer count fluctuations or the beginning of a more durable slowdown.

For Lavender AI and Workable, the latest data points look more concerning. Lavender’s Enterprise customer disappearance is a clear red flag, while Workable’s decline has now settled into a multi-month plateau.

For Sketch, the story is more nuanced given its recent reacceleration, but it’s still below

The next layer of analysis is switching activity — and the early read suggests churn is not created equal. For customers that churned each of these vendors, our Signals B2B spend data can show where their spend went next. In some cases, the data points to clear competitive displacement.

Want to see where customers are going after they churn Lavender AI, Workable, Sketch, or any other AI & software company in our coverage?

See our B2B spend data in action

FAQ’s

- Why are some software companies losing customers in 2026?

- Customer declines can happen for many reasons, including increased competition, software consolidation, budget scrutiny, changing buyer priorities, or category disruption. In this analysis of our Signals B2B spend data, we took a closer look at three companies that are losing customers. Lavender AI, Sketch, and Workable all showed customer counts below recent peaks, suggesting buyers may be reevaluating existing tools and shifting spend toward broader platforms, AI-native alternatives, or consolidated workflows.

- Does declining customer count mean a software company is in trouble?

- When our B2B spend data shows customer declines for a given AI or software company, this can be read as an early signal that an AI or software company is in trouble, but it’s not a verdict. Some companies experience temporary fluctuations due to seasonality, budget cycles, or changing market conditions. The more important questions are whether declines persist over time, whether customer spend is also falling, and whether customers are leaving for competitors or simply reducing software budgets overall. So we keep our eye on the spend data in real-time to follow the trends.

- Why is switching behavior important when evaluating software companies?

- Customer churn is an important signal to both investors and companies considering investing in an AI or software company, but it only tells part of the story. Our B2B spend data also reveals switching behavior which shows where customers go after leaving a vendor. This can help identify competitive winners and losers, emerging category leaders, and broader shifts in buyer preferences. In many cases, switching data provides a clearer picture of market dynamics than customer counts alone.

- What does the data suggest about software consolidation trends?

- The companies highlighted in this analysis based on our Signals B2B spend data operate in different categories, but they appear to be facing similar pressures. Buyers are increasingly scrutinizing AI and software spend, consolidating overlapping tools, and favoring platforms that can solve multiple problems within a single workflow. This trend may be particularly challenging for standalone point solutions operating in crowded categories.

- Which software categories appear most exposed to disruption?

- Based on the trends discussed in this analysis pulled from our B2B spend data, categories such as sales productivity tools, recruiting software, and design software may be experiencing increasing competitive pressure. In some cases, buyers are consolidating around broader platforms. In others, AI-native tools and changing workflows may be reshaping how companies evaluate software purchases.

- Where does YipitData's AI and software data come from?

- YipitData's insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors, including customer adoption, spend growth, retention, churn, and switching activity. By tracking how businesses actually allocate software budgets, YipitData can identify emerging trends and competitive shifts earlier than traditional signals such as funding announcements, headcount growth, or media coverage.

Connect with us!

.svg)