Which beauty brands are breaking out right now?

By Jenny Liu, Director of Product @Yipitdata

Clinical K-beauty, TikTok-native skincare, and wellness-adjacent beauty brands are scaling rapidly across Amazon and TikTok Shop. Our latest consumer data reveals the brands, categories, and retail channels driving the next wave of beauty momentum.

Breakout Beauty Brands

Until now, much of our analysis for private investors has focused on AI and software markets. But the same underlying question applies equally well to consumer brands: which companies are scaling faster than the broader market recognizes, and where is that momentum first appearing?

That’s why we’re launching a new series for private investors focused on emerging consumer brands, leveraging our proprietary dataset to identify the companies, categories, and retail channels showing breakout momentum earliest.

Our analysis is powered by our proprietary consumer dataset, which provides visibility into more than 50,000 brands across both tracked and historically under-covered retail channels, including Amazon, Sephora, Ulta, TikTok Shop, Costco, Walmart, Target, and DTC. Our panel combines receipt data, credit card data, Amazon data, and web-scraped retailer data to help investors identify emerging brands and benchmark performance at the retailer, brand, category, and SKU level.

For our first edition, we analyzed the beauty category to identify:

Beauty brands scaling fastest right now

Beauty categories disproportionately driving beauty growth

Retail channels surfacing the next generation of beauty winners

Key Takeaways (Data through April 2026)

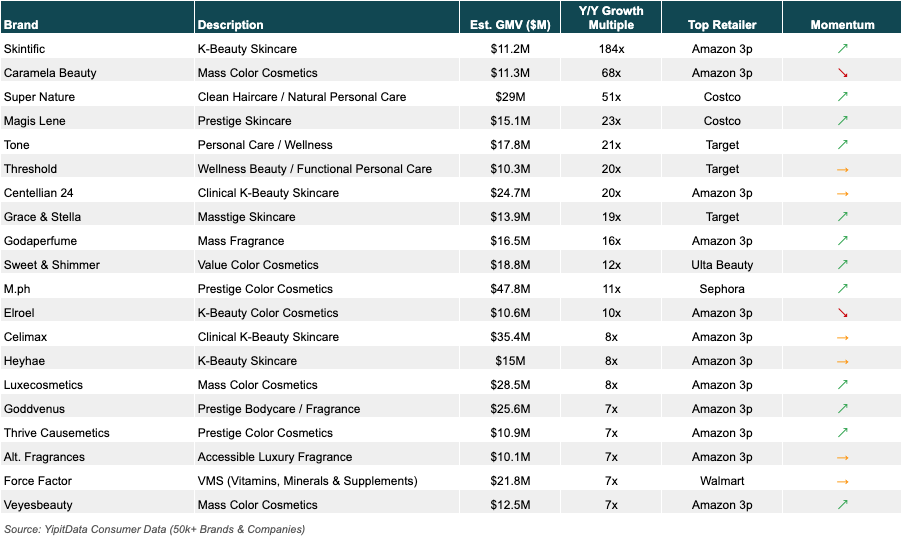

Clinical K-beauty and skincare brands dominate the fastest-growing cohort. Skintific, Celimax, Centellian 24, Drreju-all, Phofay-skin Care, and Heyhae all showed strong scale and growth in our panel.

TikTok Shop continues to function as an early beauty incubation platform. Bare Anatomy Haircare (~50X growth in last 6M) and Phofay-skin Care (~5X growth in last 6M) both showed highly concentrated exposure to TikTok Shop while already surpassing meaningful GMV scale.

Amazon 3P is one of the most important retailers for emerging beauty brands. Many brands showing meaningful momentum — including Skintific, Godaperfume, Luxecosmetics, Goddvenus, and Veyesbeauty — had Amazon 3P as their largest observed retailer.

Wellness-adjacent beauty categories continue gaining share. Tone, Threshold, Based, and Force Factor all showed meaningful scale and momentum, suggesting consumer spend continues converging across beauty, supplements, and functional personal care.

Clinical, K-Beauty, and Wellness Brands Drive Outsized GMV Growth

The brands showing the strongest trailing 3-month GMV growth skew heavily toward three overlapping themes: clinical skincare, K-beauty, and wellness-adjacent categories.

K-beauty in particular continues to generate disproportionate momentum relative to the broader beauty market. Brands including Skintific (~184x Y/Y GMV growth), Centellian 24 (~20x), Celimax (~8x), Heyhae (~8x), and Elroel (~10x) all screened among the fastest-growing companies in our panel.

The common thread across many of these brands is a strong emphasis on efficacy-oriented skincare — products positioned around clinical ingredients, barrier repair, hydration, and functional outcomes rather than traditional prestige beauty branding.

At the same time, wellness-adjacent beauty categories continue gaining momentum as consumer purchasing behavior increasingly blurs the line between beauty, supplements, and functional health products.

Tone (~21x Y/Y GMV growth), Threshold (~20x), and Force Factor (~7x) all showed meaningful scale and momentum in our panel, reinforcing the idea that consumers are increasingly approaching beauty through a broader wellness lens.

Exhibit 1: Top Beauty Brands by Trailing 3-Month GMV Growth (Data Through April 2026)

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

Amazon and TikTok Shop Emerge as Beauty Incubation Infrastructure

One of the clearest patterns across the dataset is the growing importance of marketplace-led brand formation.

Amazon 3P overwhelmingly dominates the breakout cohort. Eleven of the twenty brands in Exhibit 1 showed Amazon 3P as their top observed retailer, including Skintific (~184x Y/Y GMV growth), Celimax (~8x), Godaperfume (~16x), and Thrive Causemetics (~7x).

The data increasingly suggests Amazon is functioning not just as a retail destination, but as a discovery and scaling engine for emerging beauty brands.

TikTok Shop appears to be playing a complementary — and in some cases even earlier-stage — role.

Brands like Bare Anatomy Haircare (~50x growth in the last six months) and Phofay-skin Care (~5x growth in the last six months) remain heavily concentrated within TikTok Shop while already reaching meaningful GMV scale.

This matters because it potentially changes the speed and economics of consumer brand emergence. Platforms like Amazon and TikTok Shop increasingly appear to function as customer acquisition and product validation infrastructure, allowing brands to scale much faster than traditional retail pathways historically allowed.

The retail story is not limited to marketplaces alone. Costco also appears to be emerging as a meaningful beauty scaling channel.

Super Nature (~51x Y/Y GMV growth) and Magis Lene (~23x) both showed Costco as their top observed retailer while maintaining elevated growth rates, highlighting growing beauty penetration within warehouse retail.

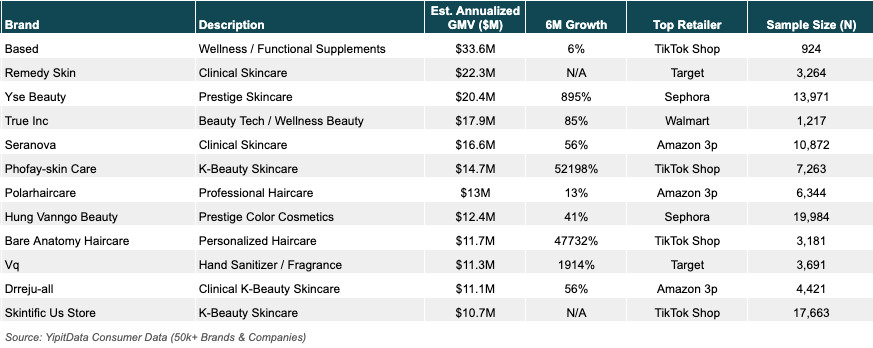

The Next Wave of Beauty Winners Is Already Reaching Meaningful Scale

Many of the brands in Exhibit 2 (below) had no observable spend in our panel just one year ago, but have now already scaled into the $10M–$50M annualized GMV range.

This cohort skews heavily toward Amazon-native beauty, clinical skincare, prestige cosmetics, and TikTok-native consumer brands.

Bare Anatomy Haircare (~$12M GMV) and Phofay-skin Care (~$15M GMV) stand out as particularly notable examples of TikTok Shop-native scaling dynamics, posting roughly ~50x and ~5x six-month GMV growth respectively while remaining highly concentrated within the platform.

The broader category patterns from Exhibit 1 continue to show up here as well.

Remedy Skin (~$22M GMV), Seranova (~$17M), Drreju-all (~$11M), Skintific (~$11M), and Phofay-skin Care (~$15M) all screened among the strongest emerging brands in the dataset, with Amazon 3P and TikTok Shop repeatedly surfacing as the dominant retail exposure across the cohort.

Exhibit 2: Emerging Beauty Brands Already at $10M+ Annualized Revenue (Data Through April 2026)

From early marketplace momentum to durable multi-channel consumer business

The data suggests beauty brand formation is becoming increasingly marketplace-native.

Across both exhibits, Amazon 3P and TikTok Shop repeatedly appear as the dominant scaling channels for emerging brands — particularly among clinical skincare, K-beauty, and wellness-adjacent categories. In many cases, brands are reaching meaningful GMV scale while still heavily concentrated within a single marketplace ecosystem.

That matters because it potentially changes both the speed and economics of brand emergence. Platforms like Amazon and TikTok Shop increasingly appear to function not just as distribution channels, but as early customer acquisition and product validation infrastructure for the next generation of beauty brands.

At the same time, the concentration risk is real. Many of these companies remain highly dependent on a narrow set of viral products, performance marketing dynamics, and marketplace algorithms.

The key question from here is which brands can successfully transition from early marketplace momentum into durable multi-channel consumer businesses with repeat purchasing power, broader retail expansion, and sustained brand equity.

Want to see which other beauty brands are scaling?

FAQ’s

-

The fastest-growing beauty brands in 2026 according to YipitData’s proprietary consumer dataset skew heavily toward clinical K-beauty and wellness-adjacent categories, with Skintific (~184x year-over-year GMV growth), Tone (~21x), Centellian 24 (~20x), and Bare Anatomy Haircare (~50x growth over the last six months) among the top performers in consumer panel data through April 2026. Many of these brands share an emphasis on efficacy-oriented skincare — barrier repair, clinical ingredients, and functional outcomes — rather than traditional prestige branding. Wellness-adjacent brands like Force Factor and Threshold are also scaling rapidly as consumer spend blurs across beauty, supplements, and functional personal care.

-

Amazon third-party marketplace and TikTok Shop have emerged as the dominant scaling channels for breakout beauty brands in 2026 according to YipitData’s proprietary consumer dataset, functioning as customer acquisition and product validation infrastructure rather than just distribution. Eleven of the twenty fastest-growing brands in the dataset had Amazon 3P as their top observed retailer, while TikTok Shop is acting as an even earlier-stage incubation platform for brands like Bare Anatomy Haircare and Phofay-skin Care. Costco is also emerging as a meaningful beauty scaling channel, with brands like Super Nature (~51x Y/Y GMV growth) and Magis Lene (~23x).

-

YipitData’s proprietary consumer dataset shows that K-beauty is growing faster than the broader US beauty market largely because its products align with a consumer shift toward efficacy-first skincare — formulas built around clinical ingredients, barrier repair, and measurable outcomes rather than brand prestige or packaging. Brands like Skintific, Celimax, Centellian 24, and Heyhae have all shown outsized GMV growth in consumer panel data, with Amazon 3P serving as the primary discovery and scaling channel for many of them. The rise of marketplace-native brand formation has also lowered the barriers for K-beauty brands to reach US consumers without traditional retail partnerships.

-

Based on YipitData’s proprietary consumer dataset, we see TikTok Shop functioning as an early-stage incubation platform for beauty brands, allowing companies to reach meaningful revenue scale while remaining almost entirely concentrated within the platform. Bare Anatomy Haircare reached approximately $12M in annualized GMV with roughly 50x six-month growth, and Phofay-skin Care reached approximately $15M with roughly 5x growth — both heavily dependent on TikTok Shop. The platform appears to accelerate brand formation by combining viral content discovery with in-app purchasing, compressing the timeline from product launch to meaningful consumer traction.

-

The biggest risk for marketplace-native beauty brands is concentration. Many of the fastest-growing companies remain highly dependent on a narrow set of viral products, a single retail platform, and performance marketing or algorithm-driven discovery. YipitData’s consumer panel data shows that while brands like Skintific and Bare Anatomy Haircare have reached impressive GMV scale quickly, their revenue is still heavily concentrated within one marketplace ecosystem. The central question for these brands is whether they can translate early marketplace momentum into durable multi-channel businesses with repeat purchasing, broader retail distribution, and sustained brand equity.

-

Our analysis is powered by our proprietary consumer dataset, which provides visibility into more than 50,000 brands across both tracked and historically under-covered retail channels, including Amazon, Sephora, Ulta, TikTok Shop, Costco, Walmart, Target, and DTC. Our panel combines receipt data, credit card data, Amazon data, and web-scraped retailer data to help investors identify emerging brands and benchmark performance at the retailer, brand, category, and SKU level.