Who’s Winning Compliance AI in 2026: Vanta or Drata?

By Jenny Liu, Director of Product @Yipitdata

The compliance AI market is splitting by segment. Signals data tracking real software spend across 1,300+ companies shows Vanta maintaining a commanding mid-market lead while Drata gains momentum in enterprise adoption and monetization.

Key Takeaways From Compliance AI Data (through February 2026):

Vanta dominates mid-market adoption and spend, reaching nearly 2x Drata’s 77 customers.

Drata leads enterprise adoption, reaching 45 customers vs. 31 for Vanta after a prolonged period of near parity through 2024 and early 2025.

Drata also ahead in enterprise spend, with ~$242K vs. ~$159K for Vanta.

Switching remains negligible — direct moves between Vanta and Drata are rare.

Sprinto is the fast-moving challenger: Sprinto adoption has surged +233% since May 2025, carving out a significant niche among mid-market growth companies driven primarily by new customer adoption rather than competitive displacement.

Vanta is dominating mid-market adoption and spend while Drata has taken the lead in enterprise in the compliance AI category.

That’s what we saw this week when we analyzed the fast-growing compliance AI category — including Vanta, Drata, Sprinto, and Secureframe. What the data suggests is that the category isn’t evolving as a single competitive race. Instead, the market is increasingly split by segment.

Our analysis is powered by Signals, YipitData’s proprietary B2B spend panel, which tracks real software usage and spend across 1,300+ mid-market and enterprise companies and provides visibility into ~250,000 AI and software vendors.

We dug into the data to understand which platforms are gaining traction, how monetization is evolving, and where competitive positioning is beginning to solidify across mid-market and enterprise customers.

Compliance AI Category Background

The trust management category has become one of the more important infrastructure layers in modern software. As security reviews and compliance requirements become increasingly standardized across SaaS procurement, companies are investing earlier in platforms that can automate audit readiness and reduce ongoing operational burden.

Several vendors have emerged as category leaders, though they are now following notably different trajectories.

Vanta remains the scale incumbent. The company last raised a $150M Series D at a roughly $4B valuation in July ’25 and has continued aggressive expansion, growing headcount 29% over the past six months to approximately 1.5k employees.

Drata has increasingly positioned itself as Vanta’s primary enterprise competitor. Despite relatively flat hiring — with headcount declining 10% over the past six months to 707 employees — the company’s enterprise momentum appears to be accelerating in the underlying spend data. It last raised $200M Series C in Dec 2022.

Secureframe, one of the earlier entrants in the category, appears to have plateaued more recently. Headcount has been gradually declining since 2024, falling 4% over the last six months to 106 employees. Secureframe last raised a $56M Series B in Feb 2022.

Meanwhile, Sprinto has emerged as a newer AI-first challenger focused on continuous compliance automation. Sprinto raised a $20M Series B in Apr 2024 Despite a 9% decline in headcount over the last six months, the company is showing some of the fastest relative growth in the category — reinforcing a pattern we continue to observe across AI and software markets: headcount growth alone is often an unreliable signal of business momentum.

Vanta Maintains a Commanding Mid-Market Lead

Our data suggests the compliance AI market is increasingly splitting into separate competitive races by customer segment. In other words, we’re looking at a “winner-take-all” reality vs a “winner-take-all” narrative.

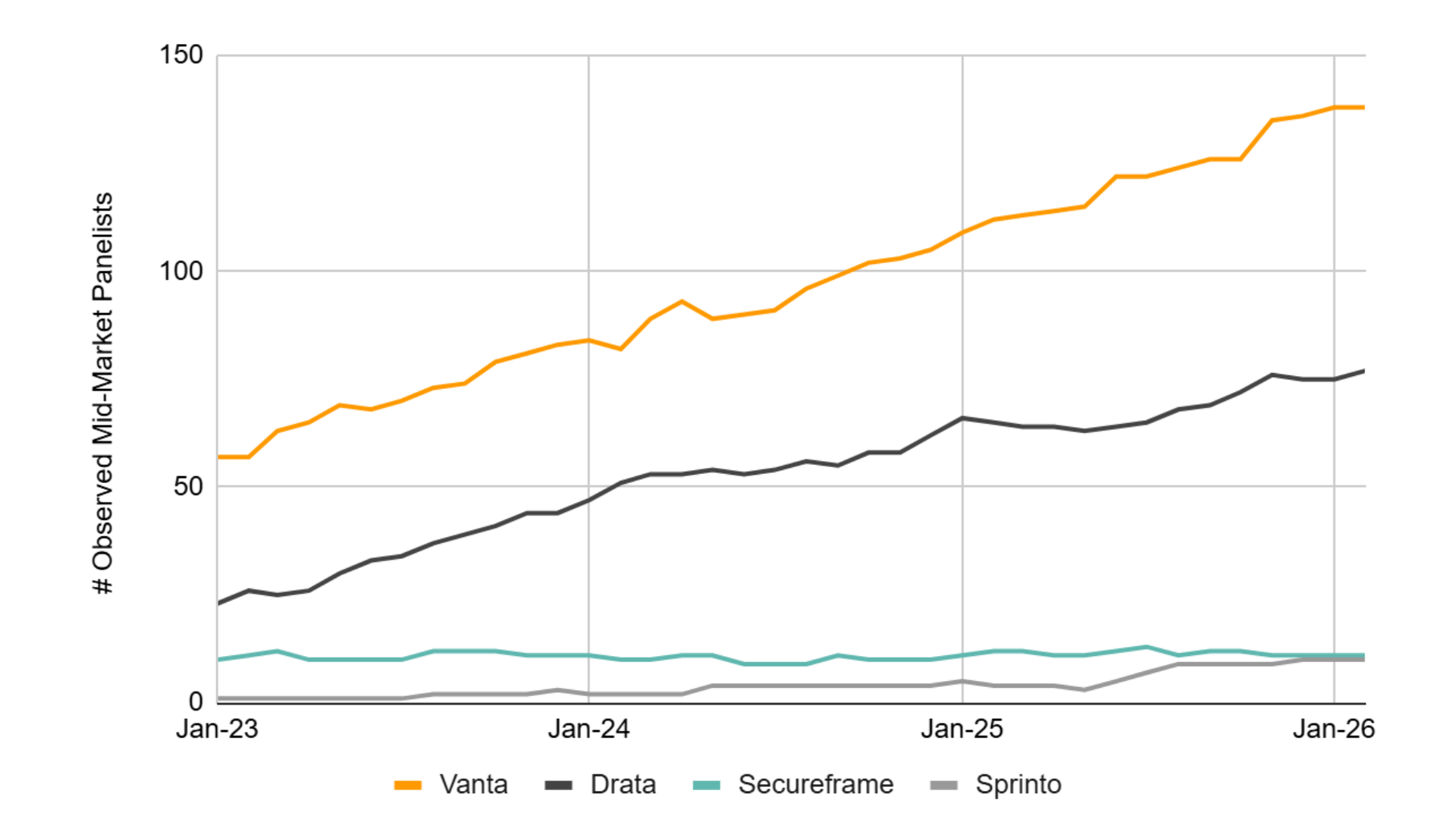

In the mid-market, Vanta continues to operate from a position of clear scale advantage. The company reached 138 observed mid-market customers in February 2026, maintaining nearly 2x the customer footprint of Drata, which remained relatively flat at 77 customers.

Sprinto remains significantly smaller overall, but its growth trajectory stands out. The company increased from just 3 observed mid-market customers in May 2025 to 10 by February 2026 — a relatively small base, but one of the fastest growth rates in the category.

Exhibit 1: Vanta Extends Mid-Market Adoption Lead; Sprinto Remains Small but Shows Early Momentum

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

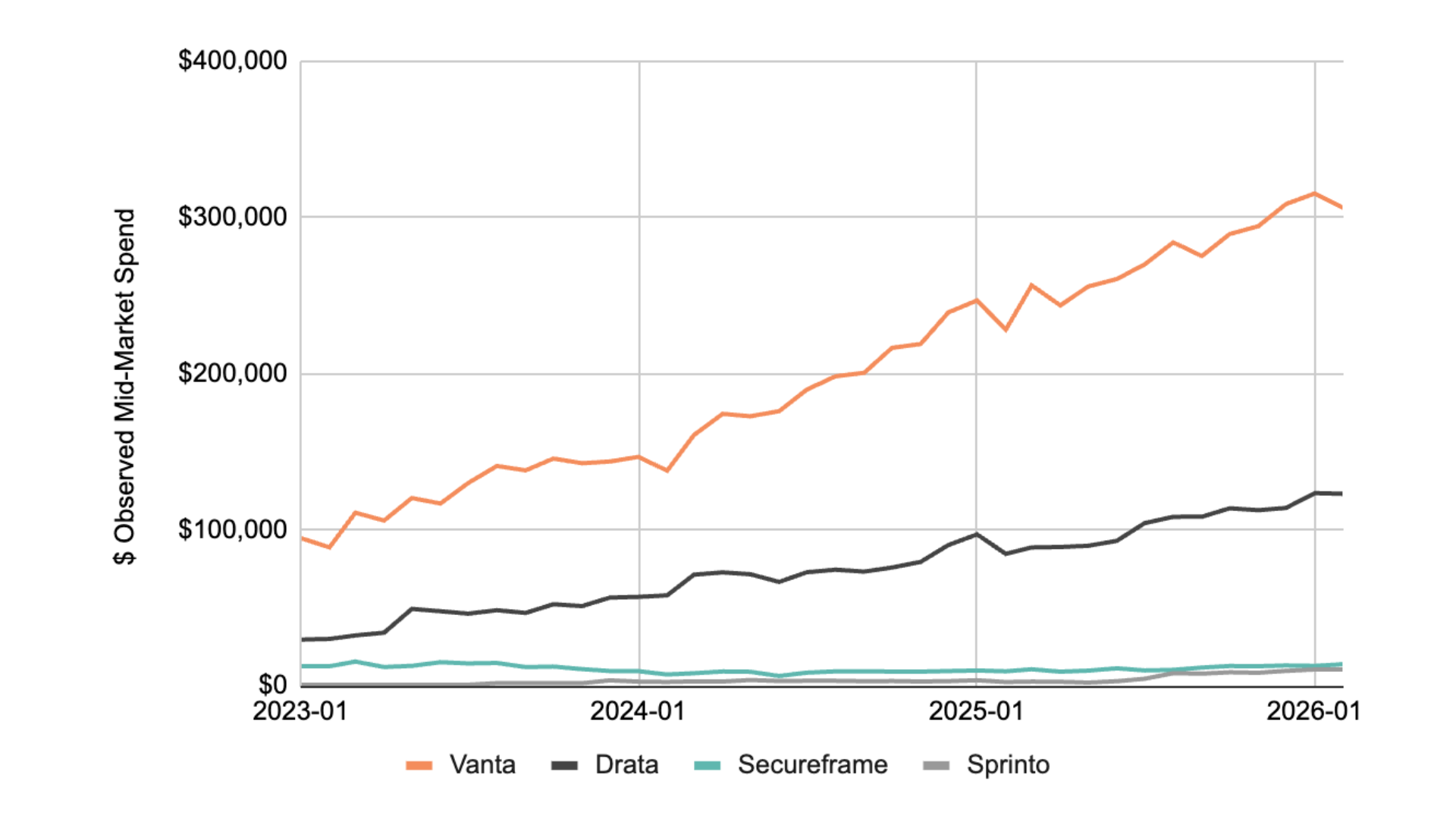

The monetization story largely mirrors adoption trends.

Vanta remains the clear mid-market spend leader, reaching approximately ~$306K in observed spend in February 2026, up roughly 24% YoY from ~$247K in February 2025.

Drata continues to grow steadily as well, reaching approximately ~$123K in spend in February 2026, representing ~45% YoY growth. But despite healthy growth, Drata’s total observed mid-market spend still sits at only about 40% of Vanta’s current level.

Sprinto’s absolute spend remains small at roughly ~$10.6K in February 2026, but its growth trajectory is notable. Spend levels entering 2026 were already roughly 3–4x higher than early 2025 levels.

What makes Sprinto particularly interesting is that this momentum is occurring despite declining headcount. In many private markets, headcount growth is often treated as a proxy for company performance. But cases like Sprinto continue to reinforce that operational efficiency and product traction can significantly diverge from hiring trends.

Exhibit 2: Vanta Leads Mid-Market Spend As Well

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

Drata Has Emerged as the Enterprise Leader

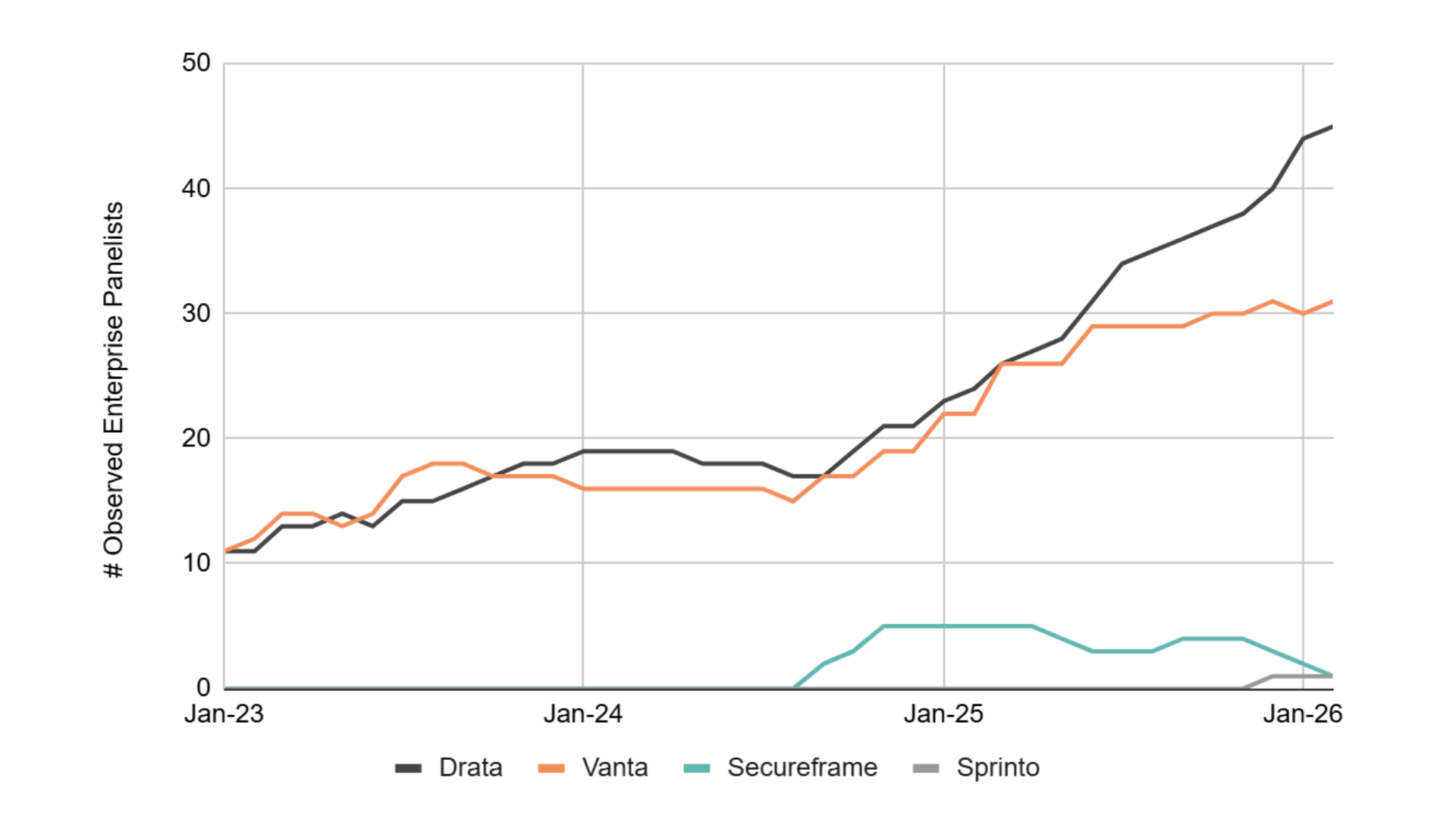

While Vanta continues to dominate mid-market adoption, the enterprise segment tells a very different story.

Throughout much of 2024 and early 2025, Vanta and Drata remained effectively tied across both enterprise adoption and enterprise spend. But over the past year, Drata has increasingly separated itself from the pack.

Signals data now shows Drata reaching 45 observed enterprise customers in February 2026 compared to 31 for Vanta. Since early 2025, Drata has added more than 20 net new enterprise customers, while Vanta added roughly 9 over the same period.

Exhibit 3: Drata Breaks Through In Enterprise Adoption

Source: YipitData Proprietary B2B Spend Data (350+ Enterprise Panelists)

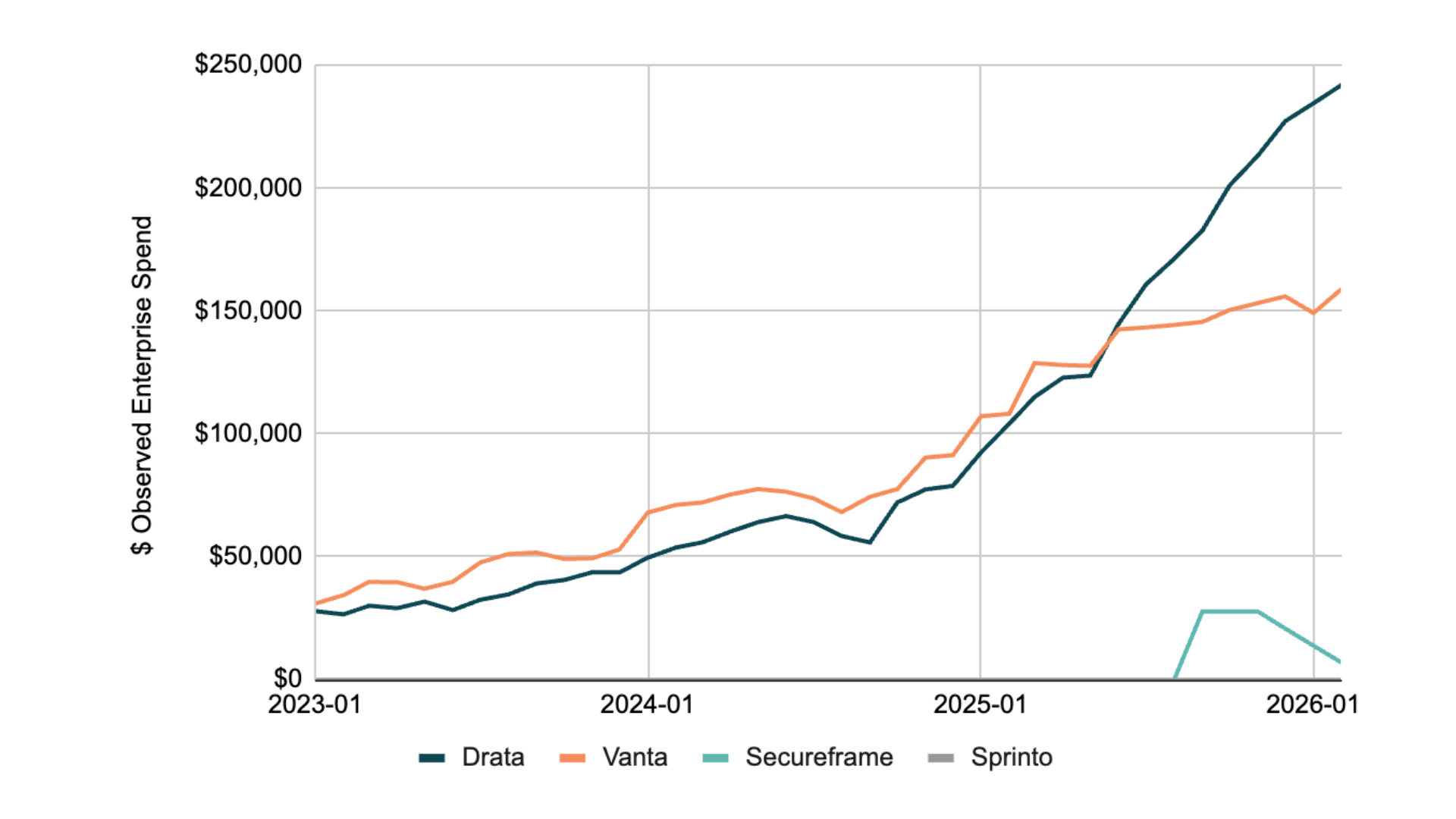

The enterprise monetization gap has also widened alongside adoption gains.

Drata reached approximately ~$242K in enterprise spend in February 2026 versus roughly ~$159K for Vanta. More importantly, Drata’s spend growth trajectory has accelerated substantially faster over time.

Since January 2024, Drata’s observed enterprise spend has grown roughly +387%, compared to approximately +134% for Vanta.

The combination of rising customer counts and rapidly expanding spend suggests Drata is not simply winning more enterprise accounts, it’s also securing larger enterprise contract values as it scales.

The speed of the shift is particularly notable. Drata trailed Vanta through much of 2024 before overtaking the company around mid-2025 and continuing to widen the gap through early 2026.

(See actual Drata pricing for 2026 – and check out other real contract costs in SpendHound’s marketplace.)

Exhibit 4: Drata Leads In Enterprise Spend

Source: YipitData Proprietary B2B Spend Data (350+ Enterprise Panelists)

Retention Trends Reinforce the Segment Divide

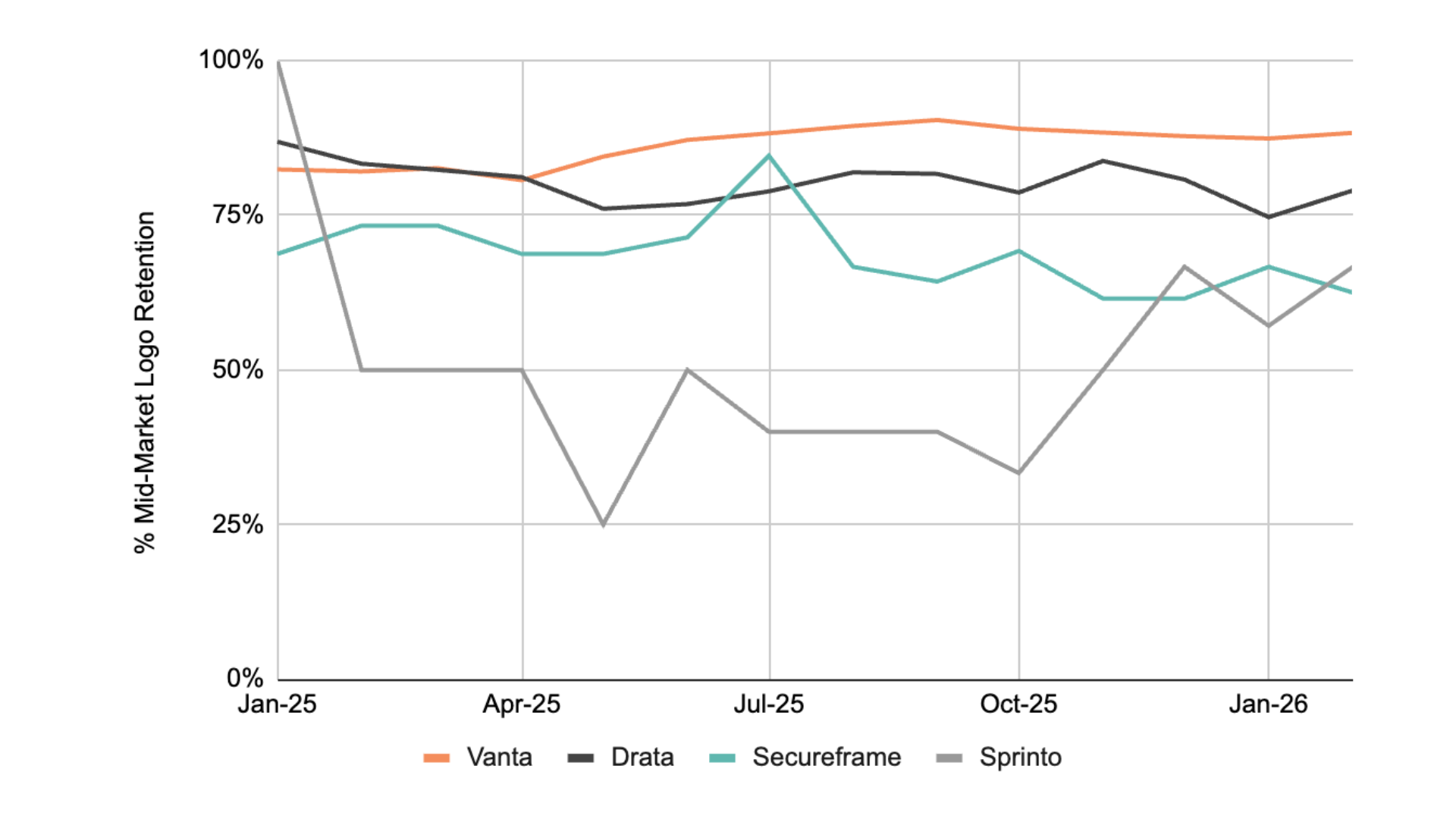

Logo retention data shows a clear divergence by segment — mirroring broader adoption trends. Logo retention is measured as % of panelists that were customers one year ago that are still customers.

In the mid-market, Vanta maintains the strongest and most stable retention profile, generally sustaining retention levels in the ~85–90% range across most of the observed period.

Drata trails somewhat behind Vanta but still maintains relatively healthy retention levels in the ~75–80% range. Secureframe and Sprinto show more variability and lower overall retention consistency.

Exhibit 5: Vanta Leads Mid-Market Retention With the Most Stable Performance

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

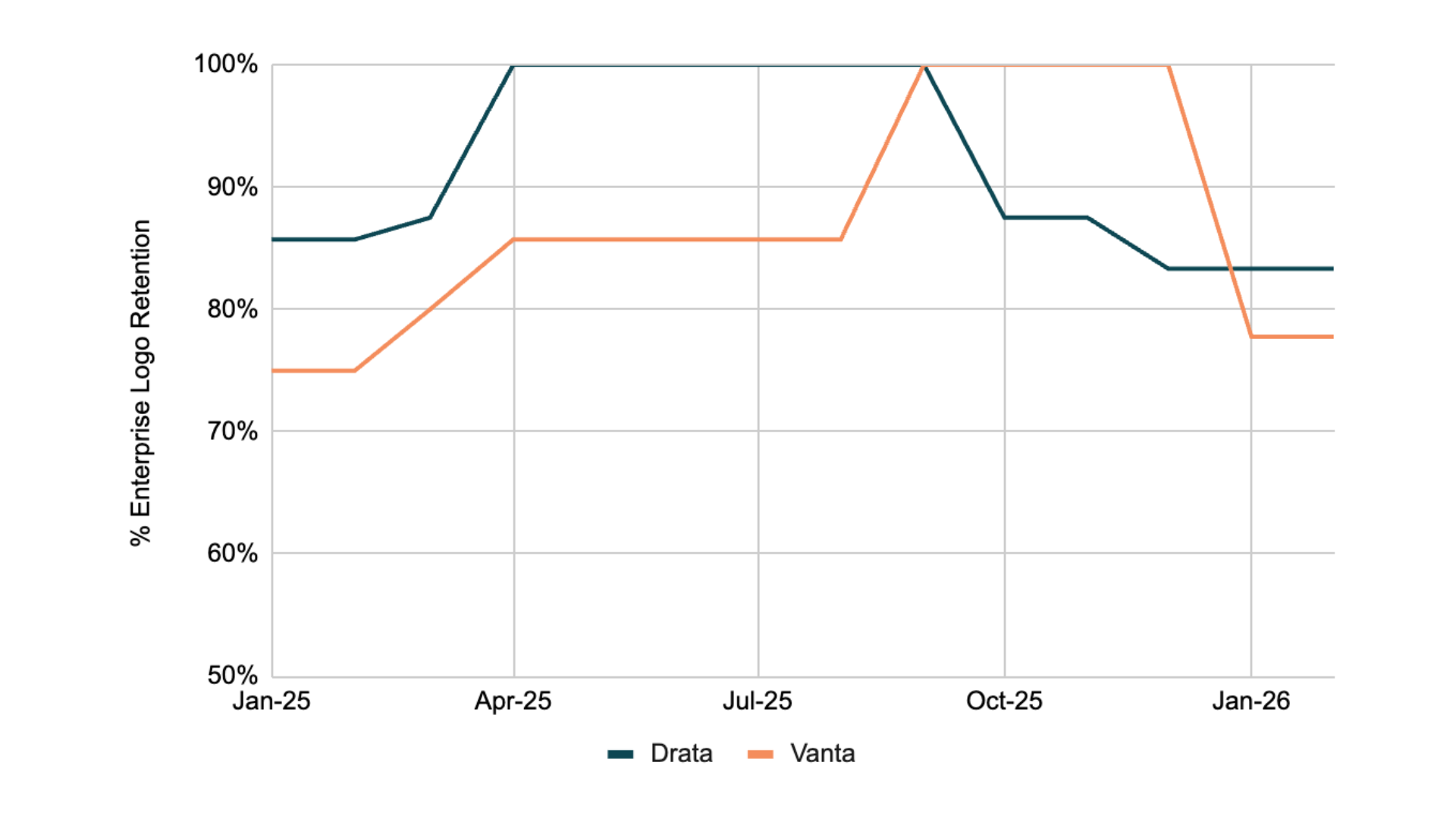

Enterprise retention dynamics are tighter overall, but Drata appears to hold a modest edge in terms of consistency.

Drata maintained retention rates between roughly ~85–100% across most of 2025 with fewer significant drops. Vanta reached similarly strong levels at certain points, but exhibited greater variability and sharper recent declines.

Exhibit 6: Drata Shows Slight Edge in Enterprise Retention

Source: YipitData Proprietary B2B Spend Data (350+ Enterprise Panelists)

Taken together, the retention data helps explain why competitive positioning in the category has remained relatively stable over time. Once companies adopt a compliance platform and integrate it into audit workflows, vendor relationships appear highly durable.

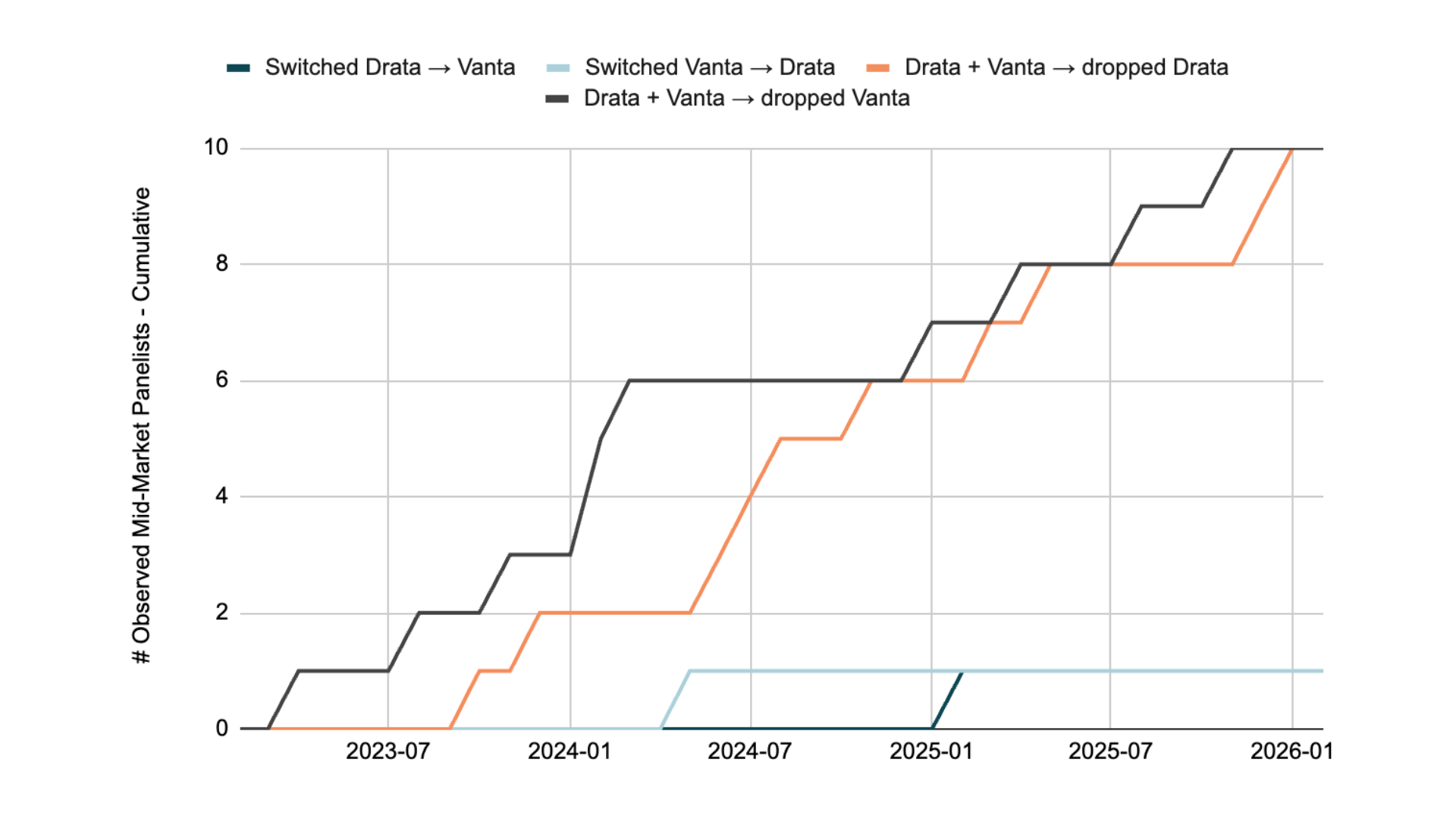

Switching Between Platforms Remains Rare

While some categories see frequent "add/drop" behavior, compliance platforms are proving to be exceptionally sticky.

Direct switching between Vanta and Drata remains very limited in the observed panel data, suggesting high operational switching costs and deep integration into internal compliance processes.

Interestingly, companies that evaluate both vendors do not appear to show a clear systematic preference toward either platform. Selection outcomes remain relatively balanced when both vendors are considered simultaneously.

Instead, the majority of category growth continues to come from entirely new customer adoption rather than competitive takeaways.

This dynamic matters because low switching environments tend to reward early segment leadership. If customers rarely move once implemented, then advantages in adoption and retention can compound over time.

Exhibit 7: Switching Behavior Low Across Category in Mid-Market

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

What the Data Suggests About Long-Term Compliance AI Leadership

The compliance AI category is increasingly reading like a tale of two markets.

Vanta continues to dominate the mid-market with scale, stable retention, and significantly larger spend volumes. Meanwhile Drata has successfully converted years of close competition into clear enterprise leadership, outperforming Vanta on both adoption growth and monetization among larger customers.

Perhaps most importantly, the category remains exceptionally sticky. Switching between vendors is still rare, suggesting that early segment leadership may compound over time as compliance platforms become more deeply embedded into company infrastructure and audit workflows.

Want to see what other companies are really taking off?

FAQ’s

-

According to YipitData B2B Signals data, Vanta dominates mid-market adoption and spend. As of February 2026, Vanta had 138 observed mid-market customers — nearly double Drata's 77 — and approximately $306K in mid-market spend compared to roughly $123K for Drata. Vanta also leads mid-market retention, generally sustaining logo retention in the 85–90% range.

-

YipitData’s B2B Signals data shows that Drata has emerged as the enterprise leader based on real software spend data. As of February 2026, Drata reached 45 observed enterprise customers versus 31 for Vanta, and led in enterprise spend at approximately $242K versus $159K. Since January 2024, Drata's enterprise spend grew roughly +387% compared to approximately +134% for Vanta.

-

Our YipitData B2B spend data showed Vanta and Drata effectively tied in enterprise adoption and spend through most of 2024 and into early 2025. Drata began pulling ahead around mid-2025 and continued widening the gap through early 2026. Since early 2025, Drata added more than 20 net new observed enterprise customers compared to roughly 9 for Vanta over the same period.

-

Sprinto is significantly smaller than Vanta or Drata but YipitData B2B Signals spend data is showing that Sprinto has some of the fastest relative growth in the compliance software category. Mid-market customer adoption increased from 3 observed customers in May 2025 to 10 by February 2026 — roughly +233% growth — and spend levels entering 2026 were approximately 3–4x higher than early 2025 levels.

-

Direct switching between Vanta and Drata remains very rare according to YipitData B2B Signals spend data. Most growth across the category is driven by entirely new customer adoption rather than competitive displacement. Compliance platforms become deeply embedded in security operations, audit workflows, and evidence collection processes, creating high operational switching costs once implemented.

-

YipitData’s insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors — capturing momentum earlier than traditional signals like funding or headcount.