Is Granola the new leader in AI notetaking?

.webp)

Granola is outpacing Fathom, Otter, and Fireflies.ai in mid-market AI notetaking — with 3x spend growth and near-zero churn. See what real B2B transaction data reveals.

New Signals data shows Granola rapidly gaining ground in AI notetaking, with accelerating mid-market adoption, near-zero churn, and 3x spend growth over the last six months.

Granola is pulling ahead in the AI notetaking market. YipitData's Signals data — drawn from real software transactions across 900+ mid-market companies — shows Granola posting 3x spend growth over the last six months, near-zero churn, and a pattern of displacing competitors like Fathom, Otter, and Fireflies.ai.

This analysis uses Signals, YipitData’s proprietary B2B spend panel, which tracks real software usage and spend to break down who's gaining traction, how monetization is evolving, and where competitive dynamics are intensifying across the five leading AI meeting assistants.

Because the data reflects actual transactions — not surveys or self-reported usage — it captures real momentum as it builds, often months before it shows up in funding or headlines.

To accelerate the analysis, we leveraged our Insight Agent to surface trends like switching behavior, multi-vendor adoption, and cohort dynamics directly from the data.

AI Meeting Assistant Background: Why Granola Stands Out

AI-native notetaking platforms are reshaping how teams capture and utilize meeting insights, enabling users to focus on conversation while AI handles transcription and synthesis. They’re becoming a core part of team workflows, but not all approaches are the same.

Granola is positioned as a “no-bot” AI notepad, focused on transcription-first workflows. That positioning appears to be resonating as we see Granola showing some real momentum – in and out of our Signals data. They just raised a $125M Series C in March 2026 at a $1.5 billion valuation, up 6x from their last round in May 2025. Headcount has increased 49% over the last six months. And Signals data shows strong adoption and growth spend within the mid-market.

Granola’s competitors:

Fathom, launched in 2020, was an early category leader, with a strong prosumer and mid-market presence. Over the last six months, headcount has declined 6% and their most recent raise was a $17M Series A in September 2024.

Otter.ai is a legacy transcription player that has heavily pivoted into AI assistants. Their latest funding round was in February 2021 for $50M Series B. And in the last six months, their headcount has dropped a bit to a total of 278 employees in April 2026.

Fireflies.ai was built as a meeting intelligence platform to automatically record, transcribe, and surface insights from conversations across teams. They haven’t raised primary capital since 2021, but announced a valuation of over $1B in June 2025. Fireflies.ai has grown headcount conservatively at 5% over the last six months, reaching a total employee count of 117 in April 2026.

Avoma was founded as an AI meeting assistant tailored for revenue teams, combining note-taking with call analysis, coaching insights, and pipeline visibility. Their last raise was a $12M Series A in December 2021. But their headcount has grown 14% over the last six months, to a total of 66 current employees.

This divergence between company narratives and actual usage/spend trends becomes clearer as we dive into the data.

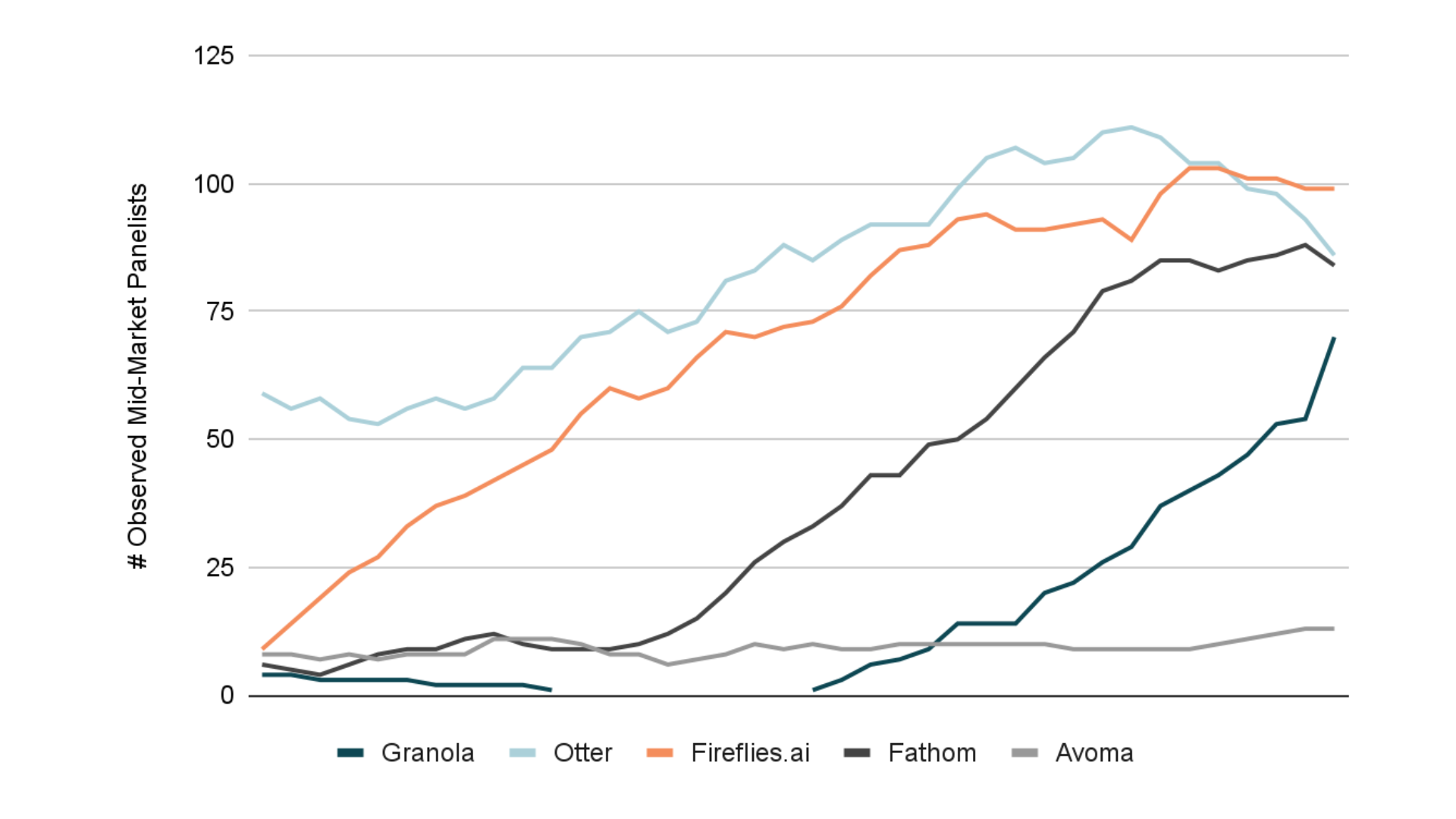

Granola Is Breaking Out in Mid-Market Adoption

Signals data shows a clear inflection in Granola’s growth trajectory, with accelerating customer growth and rapidly expanding spend per customer.

In February 2026, net new customers surged to 4x the prior six-month average, marking a step-change in adoption rather than incremental growth.

While three of Granola’s competitors still maintain larger total customer bases — with Fireflies.ai at ~40% more customers and Otter and Fathom at ~20% more — their growth is slowing. Granola, on the other hand, continues to accelerate.

Avoma is at the bottom of the pack with a relative flatline at just 13 mid-market customers. While its recent growing headcount might indicate momentum, here we clearly see that headcount alone is not a reliable indicator of product traction.

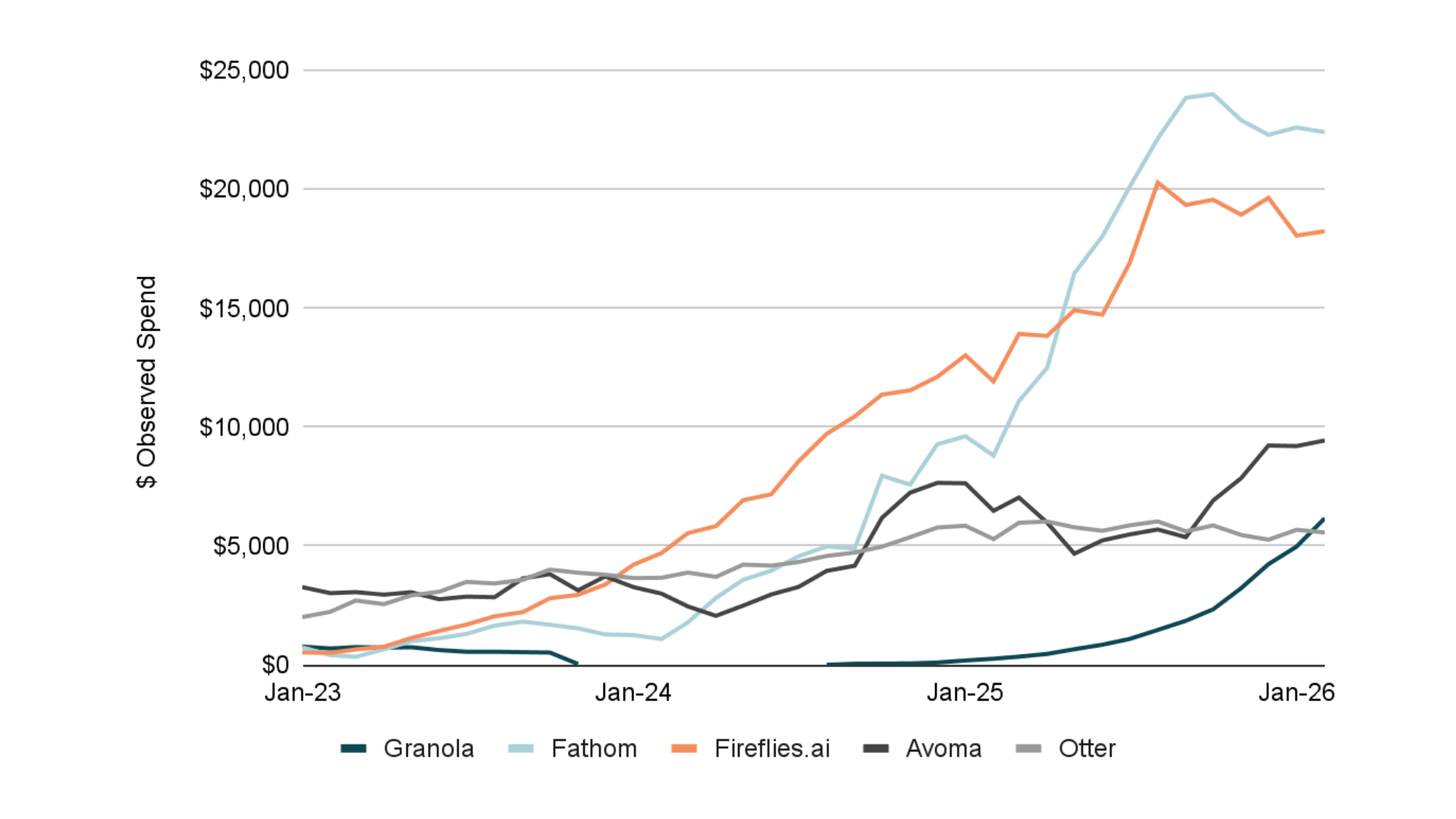

Monetization Is Catching Up to Adoption

Adoption alone can signal experimentation. Spend growth indicates commitment. Granola is showing both according to Signals data.

Their observed mid-market spend reached ~$6K in February 2026, representing a 3x increase over the last six months.

In contrast, while some of Granola’s competitors have higher overall dollar spend, they’ve seen spend levels plateau (Otter), decline (Fathom and Fireflies.ai), or fluctuate (Avoma) in recent months as they face increased competitive pressure.

This divergence suggests that while competitors may still have scale, they are struggling to convert usage into the kind of expanding revenue that signals long-term durability.

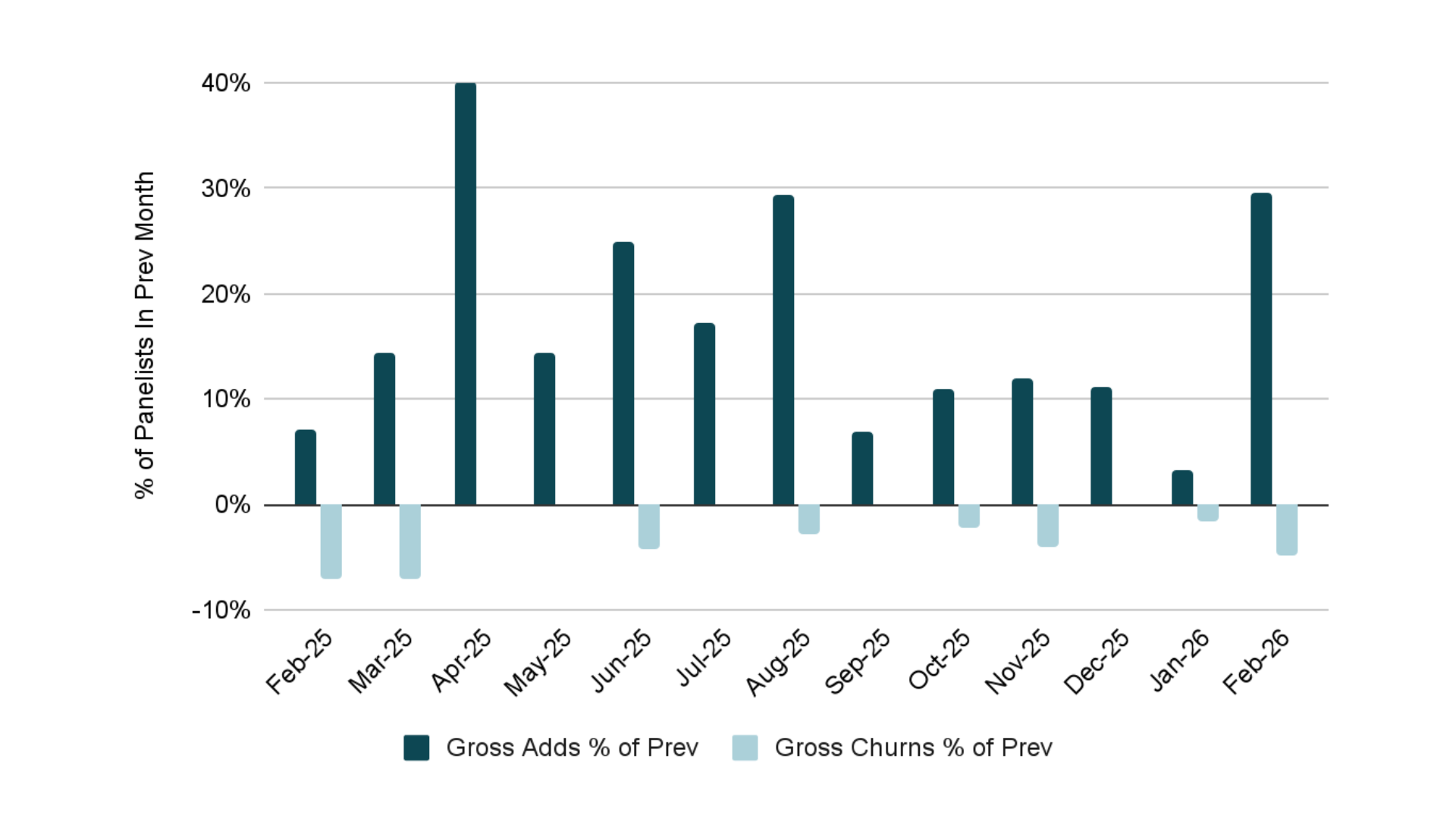

Growth Is Being Driven by Adds — Not Churn

Granola’s growth profile is notable for retention as well as acquisition.

- Gross adds increased 9x from Jan 2026 to February 2026

- Customer count grew 25% month-over-month in February 2026

- Churn remains near zero

This combination — strong new customer acquisition with minimal churn — is rare. It indicates that net growth is not being offset by customer losses, which is often what limits early-stage momentum.

Switching Behavior Suggests a Product Advantage

Direct switching remains relatively rare across the category of AI notetaking, but our panelist behavior reveals a clear pattern: After adopting Granola, customers frequently drop competing tools (Fathom, Fireflies.ai, Otter) whereas the reverse — with customer dropping Granola in favor of competitors — is seldom true.

This asymmetry suggests that Granola is replacing alternatives, not just being added for a test run.

In other words, Granola’s impressive adoption numbers aren’t just additive. Granola is displacing incumbents, which is one of the strongest indicators of product-market fit in a competitive category.

From Experimentation to Core Workflow

Despite a crowded market that includes platform-level competitors like Zoom and Microsoft, Granola is emerging as a high-growth disruptor in the mid-market segment.

The combination of accelerating adoption, expanding spend, near-zero churn, and asymmetric switching behavior suggests an important shift: Granola is moving from an experimental tool to become a core part of the productivity stack.

This is exactly the type of momentum and transition Signals data is designed to capture — before it becomes obvious in funding rounds, hiring trends, or broader market awareness.

Want to see what other companies are really taking off?

Want to see what other companies are really taking off?

See our B2B spend data in action

FAQ’s

- Which AI notetaking tool is best for mid-market teams in 2026?

- Based on YipitData's spend panel, Granola is showing the strongest momentum in 2026 — with accelerating customer growth, 3x spend growth over six months, and near-zero churn. Fathom, Otter, and Fireflies.ai all currently have larger customer bases but are seeing growth slow or spend decline.

- How does Granola compare to Fathom, Otter, and Fireflies.ai?

- Granola is gaining ground on both Fathom and Otter. YipitData's B2B Signals data shows that after teams adopt Granola, they frequently drop Fathom, Otter, or Fireflies.ai — while the reverse is rare. This asymmetric switching pattern indicates Granola is displacing incumbents, not just being trialed alongside them.

- Is Granola worth it for business teams?

- Yipit B2B Signals data suggests that for mid-market business teams, Granola is a good investment. Granola's near-zero churn rate and expanding spend per customer indicate that once teams adopt it, they commit. This is a strong signal that the product is delivering workflow value.

- Why do both customer count and spend growth matter when evaluating AI tools?

- When evaluating AI tools, customer count and spend growth together tell a more complete story than either metric alone. Customer count signals breadth of adoption, but can include free trials or low-commitment pilots. Spend growth signals that teams are actively paying and expanding — an indicator of embedded workflow value. Granola is showing both accelerating customer count and accelerating spend simultaneously, which is why its momentum reads as durable rather than experimental.

- Where does YipitData’s AI and software data come from?

- YipitData’s insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors — capturing momentum earlier than traditional signals like funding or headcount.

Connect with us!

.svg)