12 early breakout AI and software companies right now

.webp)

YipitData's Signals panel tracks ~250,000 vendors to identify breakout AI and software companies. See which early-stage companies show the strongest spend and adoption growth in 2026.

New Signals data across ~250,000 software and AI vendors highlights a small group of early-stage companies converting rapid adoption into real spend.

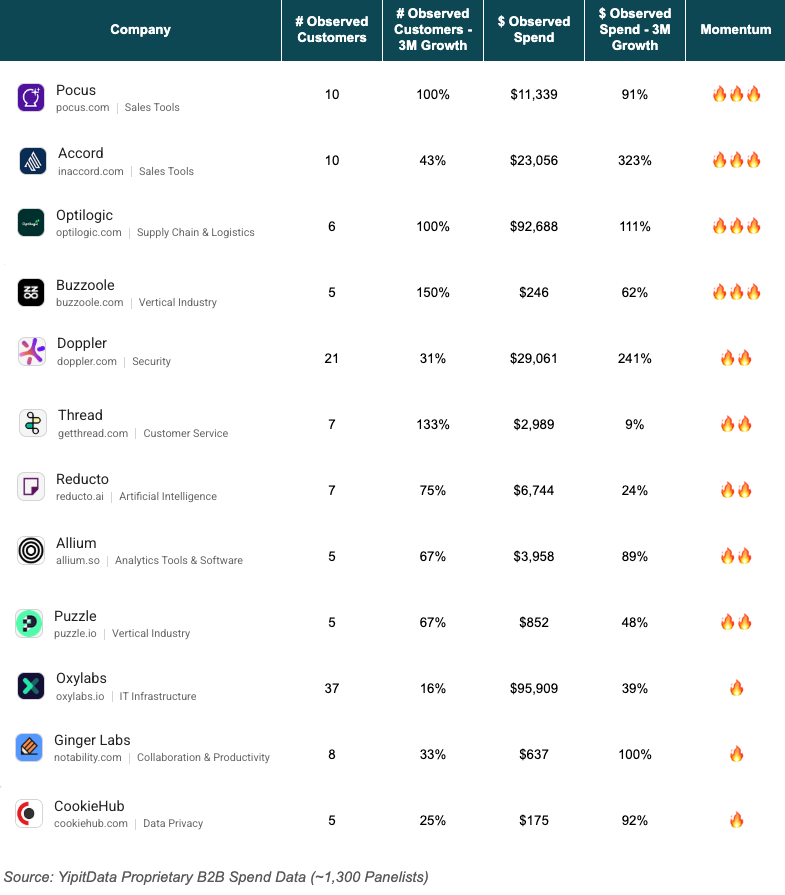

A small group of early-stage AI and software companies are breaking out in early 2026, showing rapid customer adoption paired with real spend growth across YipitData's panel of 1,300+ mid-market and enterprise companies. Pocus, Accord, and Optilogic lead the momentum rankings out of ~250,000 vendors tracked, while Buzzole (+150% customer growth) and Accord (+323% spend growth) are among the fastest movers over the trailing three months.

To surface these companies, we analyzed the cohort for two signals growing in tandem: customer adoption and spend, using a weighted view to surface early momentum. This approach enables us to pinpoint breakout signals before they show up in broader market awareness or funding cycles.

About the data: This analysis is powered by Signals, YipitData's proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies, covering approximately 250,000 software and AI vendors. Companies are cited as breakouts when they have crossed the 5+ paying customer threshold in the panel and are showing strong growth on both customer count and observed spend over the trailing three months. The Momentum ranking used within this analysis weights customer growth at 75% and spend growth at 25%.

Breakout AI and software winners right now

The companies below are still in their early innings, but all of them are showing a consistent pattern: rapidly expanding adoption paired with clear signs of monetization.

This combination — rising adoption + early monetization — is where breakout winners typically emerge. Many companies can drive initial usage, but far fewer are able to convert that usage into meaningful spend. When both are increasing together, it’s often an early signal that a company is moving beyond experimentation and into real traction.

To quantify this, we assigned an overall “Momentum” ranking based on a 75% / 25% weighting of customer growth and spend growth over the last three months.

Pocus, Accord, and Optilogic rank highest in terms of customer and observed spend growth which puts them at the top of our momentum rankings. Breaking down customer growth and spend into two distinct metrics, Buzzoole, Thread, Pocus, and Optilogic are leading the pack with more than 100% increase in observed customers over the past three months. And Accord, Doppler, Optilogic, and Ginger Labs are seeing more than 100% increase in observed spend within the last three months.

We also see some standout individual signals at the extremes: Accord posted the highest spend growth in the cohort at 323%, and Buzzoole led on customer growth at 150% — both within a three-month window. Thread's 133% customer growth is also notable given that it sits alongside Buzzoole as one of only four companies in this cohort to more than double their observed customer count in that period.

To better understand these signals in context, we selected just three for a deeper dive: Pocus, a sales tool with 100% customer and spend growth; Optilogic, an interesting supply chain and logistics company with consistent percentage increase across customers and spend; and Allium, standing out within the rapidly growing blockchain infrastructure category, with its 67% customer growth and 89% spend growth over the last three months.

Breakout Highlights: Pocus, Optilogic, Allium

Pocus

Pocus is a revenue data platform that empowers go-to-market teams to analyze and act on revenue data from prospects and customers without requiring engineering support. The company raised a $23M Series A in June 2022 and has a team of ~40 employees, with headcount remaining relatively flat over the past year.

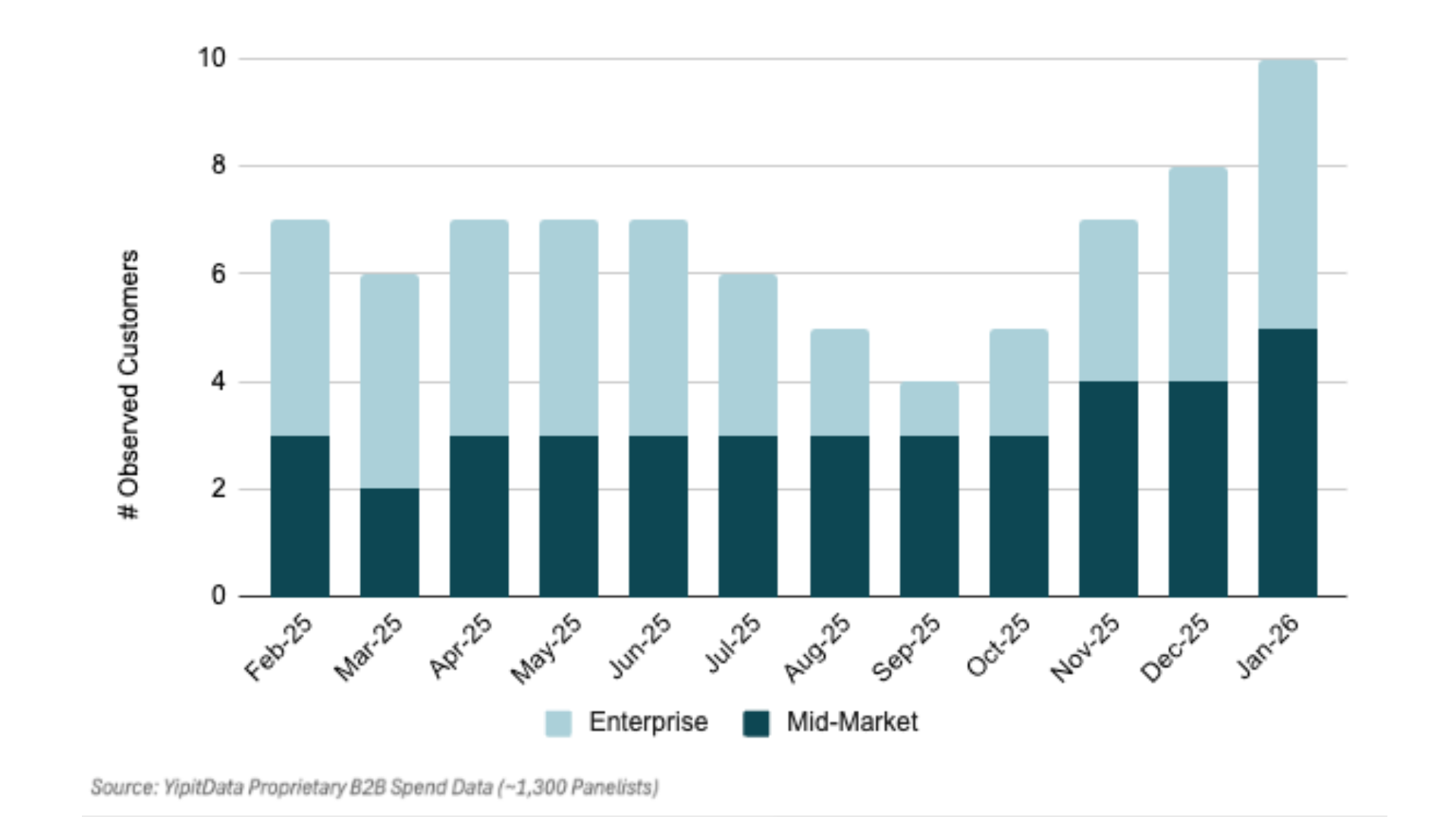

Despite limited headcount growth, Pocus has recently seen a notable acceleration in traction. Customer count reached 10 panelists (across both mid-market and enterprise), growing 100% over the last three months following an inflection point in late 2025. Spend is scaling alongside adoption, increasing 91% over the same period.

This places Pocus among the fastest-growing companies in this cohort by combined customer and spend growth. The divergence between strong panel growth and flat headcount highlights a broader pattern we regularly observe: headcount alone isn’t always a meaningful signal for business momentum.

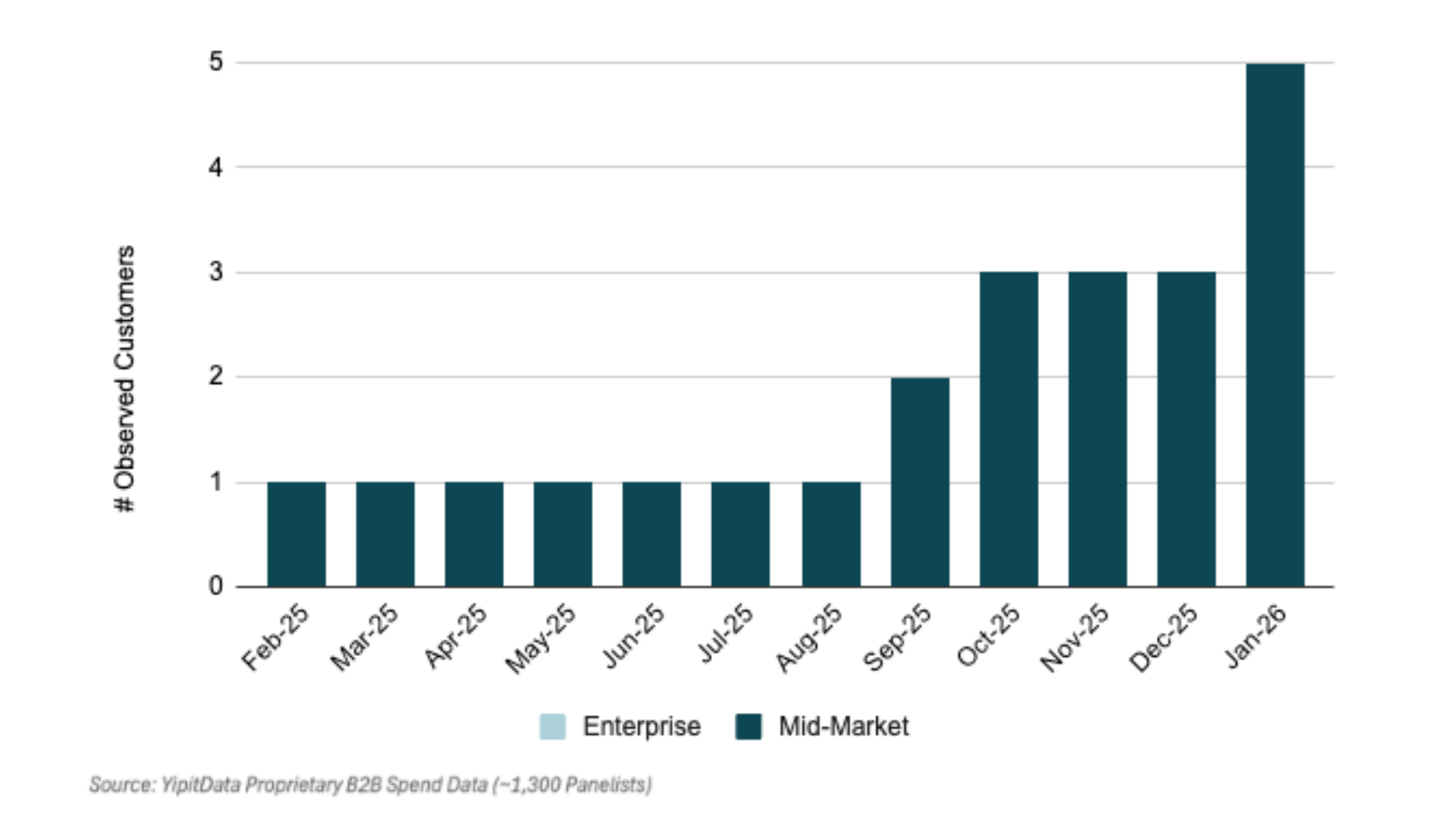

Optilogic

Optilogic provides AI-driven optimization SaaS for supply chain and operations, including modeling tools, tariff optimization, and consumption-based computing for mid-market and enterprise customers.

The company raised a $40M Series B in April 2025, and headcount has grown 19% over the past year to 152 employees.

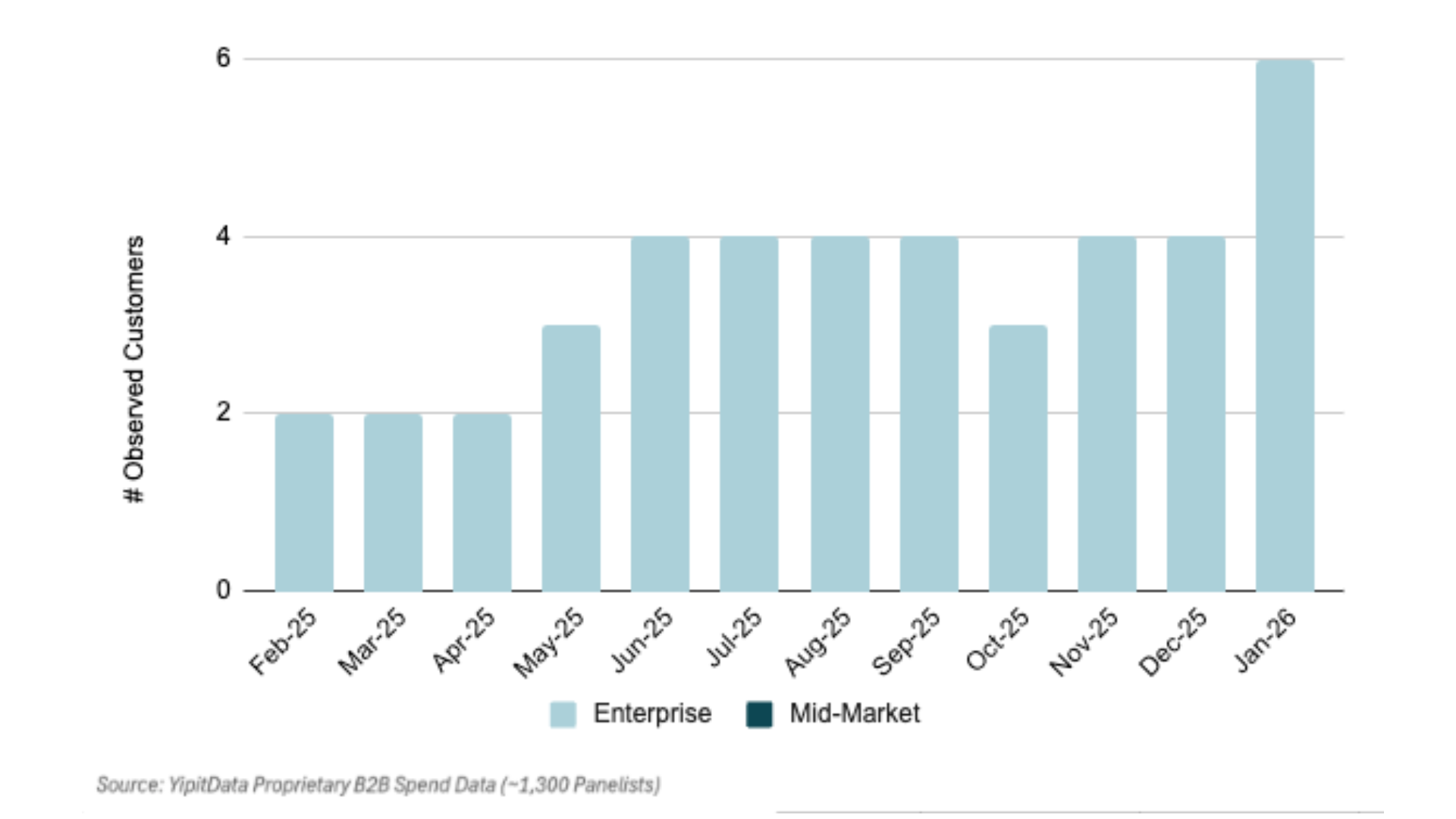

More recently, customer count doubled over the last three months to reach 6 panelists, all within the enterprise segment. Spend reached approximately $93K in our panel, increasing 111% over the same period.

At this stage, adoption appears concentrated entirely in enterprise, with no mid-market customers observed in our data.

Allium

Allium offers blockchain data infrastructure and APIs, including real-time cross-chain data, datastreams, decoded logs, Wallet360, and tools supporting analytics, DEXs, NFTs, and broader integrations.

They are well-positioned within this rapidly growing category tied to blockchain and on-chain data, with usage spanning analytics, payments, and financial infrastructure use cases.

The company raised a $16.5M Series A in July 2024, and headcount has grown 83% over the past year to 64 employees.

Customer count grew to 5 mid-market customers, increasing 67% over the last three months within our panel. And spend rose 89% over the same period, showing strong alignment between adoption and monetization. At this stage, we didn’t observe enterprise adoption in our data.

Growing adoption + growing spend = early breakout signals

These companies are still in the early stages of their growth trajectories, but the signals are consistent: adoption and spend are scaling together. That combination is what YipitData's Signals data is designed to capture — real transaction data that surfaces breakout momentum before it becomes visible in funding announcements or headcount reports. Customer growth plus spend growth, tracked together, is one of the strongest early indicators of sustained breakout potential.

How are the private AI and software companies in your portfolio doing?

FAQ’s

- Which AI and software companies are breaking out right now?

- Based on YipitData's Signals data across ~250,000 vendors, a subset of early-stage AI and software companies are identified as breakouts based on their combined adoption and spend growth rates. As of early 2026, companies including Pocus, Accord, and Optilogic are among those demonstrating the fastest momentum — defined as rapid customer growth alongside rising spend within a panel of 1,300+ mid-market and enterprise companies. Breakout signals at this stage often precede broader market recognition.

- How do you identify a software company that is about to break out?

- The strongest early breakout signal is when customer adoption and spend are growing together. Adoption alone can reflect experimentation; spend growth alongside it indicates that customers are committing real budget which is a meaningful distinction at the early stage. For the purposes of this analysis, we weighted customer growth at 75% and spend growth at 25% to surface companies crossing the breakout threshold, focusing on those that have recently reached 5+ paying customers while showing strong momentum across both metrics.

- The strongest early breakout signal is when customer adoption and spend are growing together. Adoption alone can reflect experimentation; spend growth alongside it indicates that customers are committing real budget which is a meaningful distinction at the early stage. For the purposes of this analysis, we weighted customer growth at 75% and spend growth at 25% to surface companies crossing the breakout threshold, focusing on those that have recently reached 5+ paying customers while showing strong momentum across both metrics.

- What is the difference between software adoption and software spend growth?

- Software and AI adoption measures how many companies are using a product, while spend measures how much they are paying for it. A company can show strong adoption — many customers trying the product — without those customers converting to meaningful paid usage. When spend grows alongside adoption, it indicates the product is delivering value. This alignment between adoption and monetization is typically where durable breakout trajectories begin.

- How can investors track traction in private AI and software companies?

- One of the most reliable methods for investors who need to track traction in private AI and software companies is by looking at real B2B transaction data — anonymized ERP spend data across mid-market and enterprise companies — rather than relying on self-reported metrics, headcount signals, or funding announcements. YipitData's Signals panel covers ~250,000 vendors across 1,300+ companies, making it possible to observe customer growth and spend trends in private companies well before they surface in public disclosures or press coverage. This approach surfaces momentum earlier and with more precision than traditional methods.

- Why is headcount alone not the most reliable signal for software company growth?

- Headcount growth has historically correlated with business momentum, but the relationship has weakened significantly as software companies operate more efficiently. Pocus, for example, grew customer count 100% and spend 91% over three months while headcount remained flat. As AI reduces the operational overhead required to scale, early-stage companies can expand their customer base and revenue without proportional team growth — making spend and adoption data more reliable leading indicators than hiring trends.

- Headcount growth has historically correlated with business momentum, but the relationship has weakened significantly as software companies operate more efficiently. Pocus, for example, grew customer count 100% and spend 91% over three months while headcount remained flat. As AI reduces the operational overhead required to scale, early-stage companies can expand their customer base and revenue without proportional team growth — making spend and adoption data more reliable leading indicators than hiring trends.

- Where does YipitData's software and AI spend data come from?

- YipitData's insights are powered by Signals, a proprietary B2B spend panel that tracks real software usage and spend derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This gives visibility into actual software purchasing behavior — not surveys or self-reported metrics — across approximately 250,000 vendors. Because the data reflects real transactions, it captures momentum in early-stage companies before it becomes visible through funding announcements, headcount changes, or press coverage.

- YipitData's insights are powered by Signals, a proprietary B2B spend panel that tracks real software usage and spend derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This gives visibility into actual software purchasing behavior — not surveys or self-reported metrics — across approximately 250,000 vendors. Because the data reflects real transactions, it captures momentum in early-stage companies before it becomes visible through funding announcements, headcount changes, or press coverage.

Connect with us!

.svg)