ElevenLabs is dominating voice AI — can anyone catch up?

.webp)

New Signals data shows ElevenLabs dominating voice AI adoption, usage, and spend across 1,300+ companies. See how Murf AI, LOVO, and others compare.

New Signals data on voice AI platforms shows ElevenLabs is defining the category, driving nearly all entry, usage, and spend across 900+ mid-market companies.

This week our analysis showed that ElevenLabs has essentially turned voice AI into a one-vendor category. Across 900 companies in our mid-market panel, ElevenLabs accounts for 98% of observed spend, captures 95% of first-time buyers, and retains 90% of its customers exclusively.

Our analysis is powered by Signals, our proprietary B2B spend panel that tracks real software usage and spend across 1,300+ mid-market and enterprise companies to provide data insights for ~250,000 vendors.

We used our new Insight Agent to accelerate the work of analyzing ElevenLabs, Murf AI, LOVO AI, and Resemble AI, to understand category entry, where demand is coming from, and how spend is evolving. With the Insight Agent, we’re able to quickly surface trends like switching behavior, multi-vendor adoption, and cohort growth directly from the data.

Voice AI Background

Voice AI platforms like ElevenLabs, Murf AI, LOVO AI, and Resemble AI enable companies to generate synthetic speech, clone voices, and power conversational experiences across applications.

This category has seen rapid early adoption as companies experiment with AI-driven content, customer interactions, and automation workflows. The barrier to entry is relatively low, and the use cases are broad, ranging from marketing content to product integrations.

ElevenLabs, founded in 2022, has quickly become the dominant platform in the voice AI category. The company has raised significant capital, including a $180M Series C in January 2025 and a $500M Series D more recently in February 2026.

The key question now is less about early traction and more about durability: Can ElevenLabs maintain its lead as competitors push into adjacent workflows and larger platforms begin bundling voice capabilities?

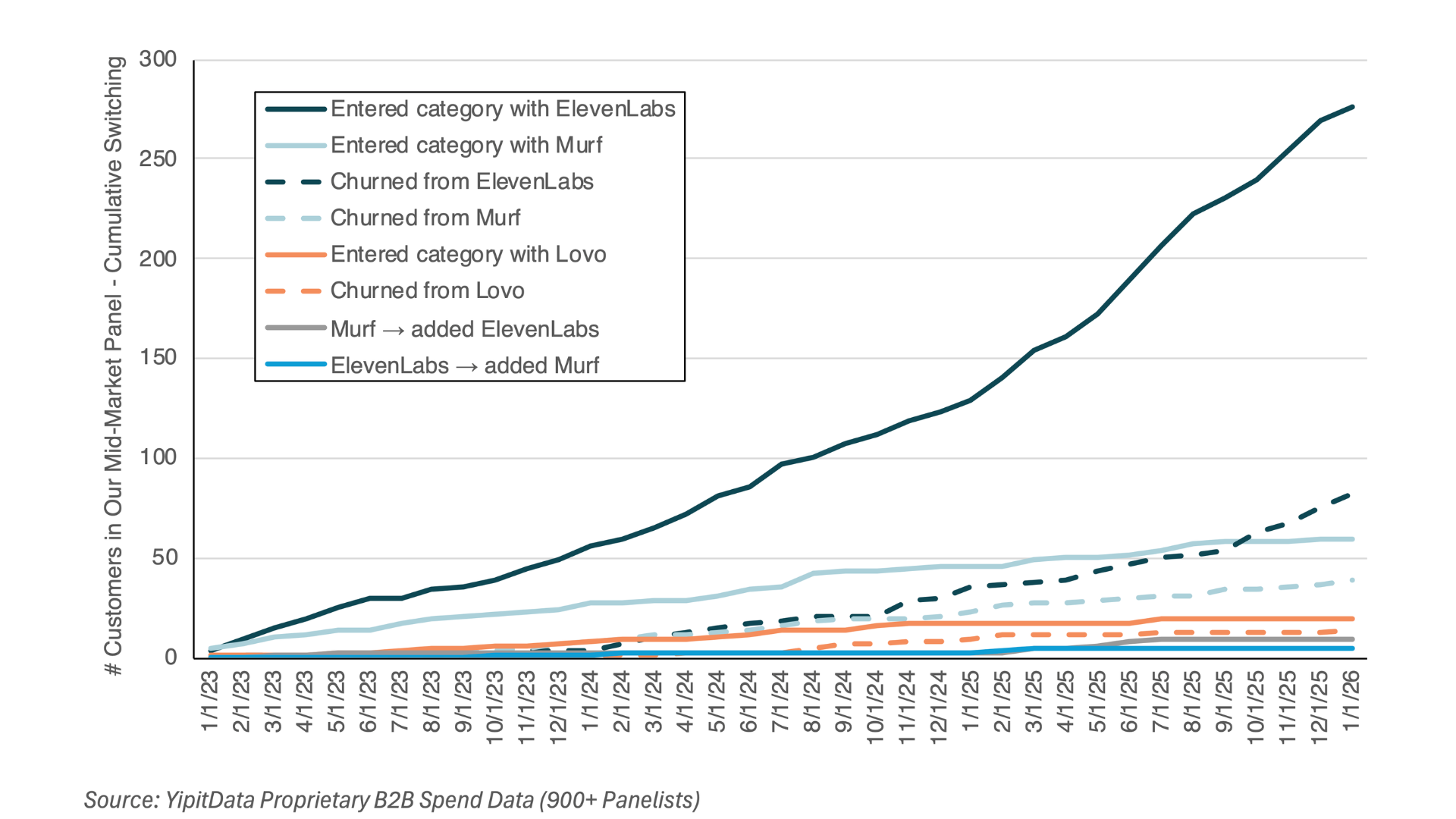

ElevenLabs Drives the Majority of Category Entry

One of the clearest signals in the data is where companies begin their voice AI adoption.

Our data shows that ElevenLabs is the primary entry point into the category, particularly in the mid-market: 95% of first-time voice AI customers entered the category with ElevenLabs in the three months ending in January 2026, up from 81% in the year prior. And cumulative adds are more than 3.5x cumulative churn.

Murf AI is the next largest driver of entry, but at only ~20% of ElevenLabs’ volume.

Source: YipitData Proprietary B2B Spend Data (900+ panelists)

This data demonstrates concentration and leadership. When nearly all new demand flows through one vendor, that vendor effectively shapes the category.

In practical terms, this also creates a reinforcing loop: more users lead to more feedback, more product iteration, and stronger default positioning for future buyers.

ElevenLabs’ Growth Continues to Accelerate

That early dominance is translating into sustained and accelerating growth.

The data shows that ElevenLabs continued to consistently grow their mid-market customer base roughly ~100% Y/Y in every month throughout 2025, with growth accelerating to ~120% entering 2026. Importantly, there are no clear signs of deceleration.

In contrast, Murf AI’s growth slowed from ~10% Y/Y to a -20% decline entering 2026.

This divergence suggests that while competitors can attract some demand, they’re not keeping pace with the category leader.

The pattern here is familiar in emerging software categories: One platform captures early momentum and continues compounding while others struggle to establish a differentiated foothold.

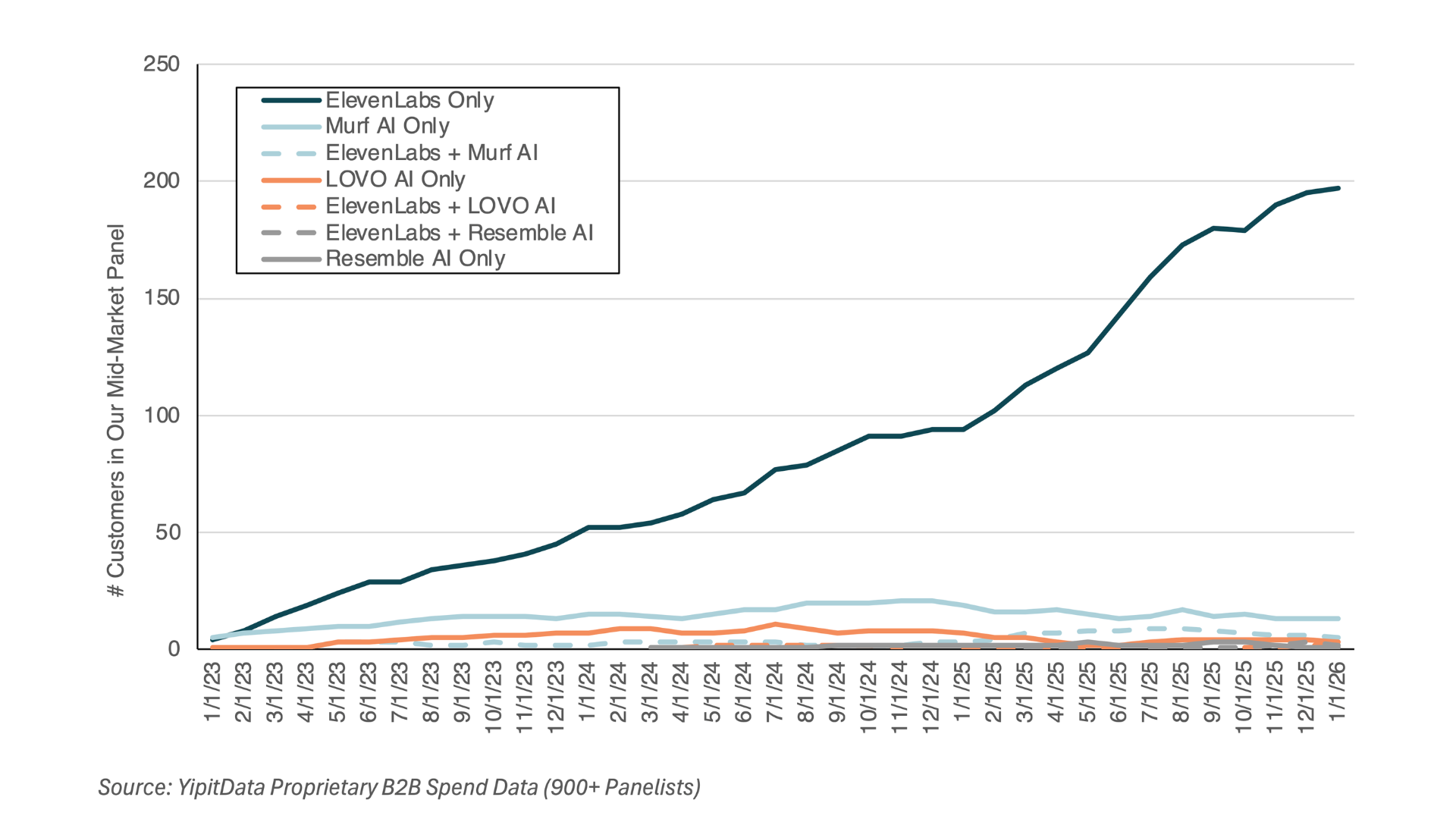

Most Mid-Market Customers Use ElevenLabs Exclusively

Despite the presence of multiple vendors, most companies are not actively experimenting across tools. While we do see some multi-vendor usage between ElevenLabs, Murf AI, LOVO AI, and Resemble AI, co-usage exists only at a small scale.

Meanwhile, 90% of mid-market customers use ElevenLabs exclusively.

Source: YipitData Proprietary B2B Spend Data (900+ panelists)

This is an important signal. In many early-stage categories, multi-vendor experimentation is common as buyers evaluate options. That behavior is relatively muted here.

Instead, ElevenLabs is functioning as the default solution.That dynamic makes it harder for competitors to gain traction. Without meaningful co-usage, there are fewer opportunities to displace the incumbent over time.

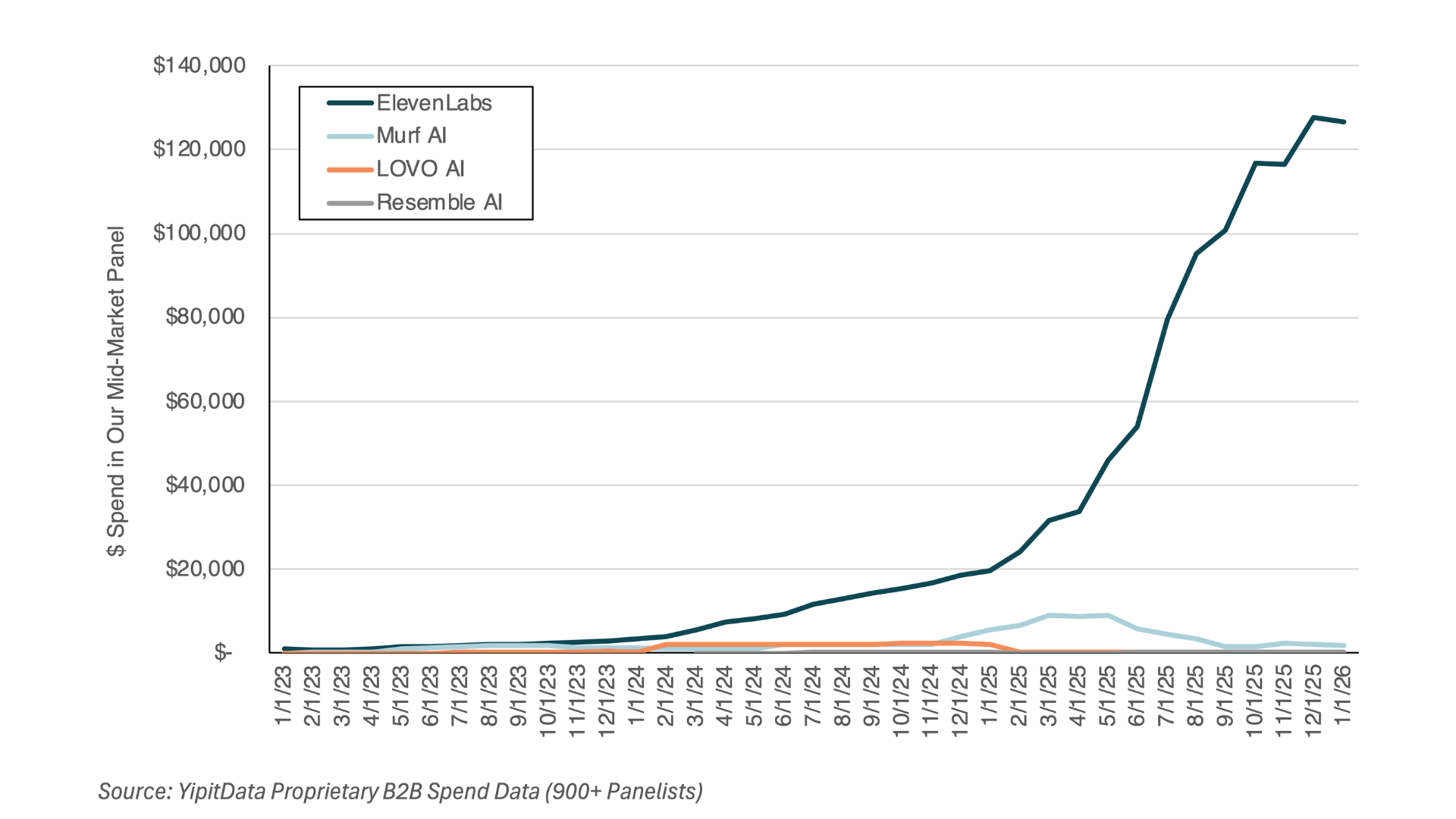

ElevenLabs Dominates In Mid-Market Monetization

The clearest indication of category leadership is not just adoption, but monetization.

Here, the gap widens further with ElevenLabs leading competitors in mid-market monetization, accounting for 98% of category spend in January 2026 after growing over 6x Y/Y following a period of sharp acceleration in early 2025.

Meanwhile, Murf AI, LOVO AI, and Resemble AI have yet to show any meaningful monetization.

Source: YipitData Proprietary B2B Spend Data (350+ panelists)

This level of concentration is high, even for a fast-moving AI category. And it suggests that competitors are struggling to convert usage into revenue, whether that’s a potential reflection of pricing strategy, product capabilities, or customer willingness to pay.

(See actual ElevenLabs pricing based on real contract data from 169 SMB, mid-market, and enterprise teams.)

The Competitive Question: Can Any Voice AI Competitors Break Through?

With ElevenLabs dominating entry, adoption, and spend, the competitive question within the voice AI category is whether or not a meaningful challenger can emerge.

For that to happen, a challenger would likely need a differentiated use case that expands beyond ElevenLabs' core strengths, distribution advantages through platform bundling, or a meaningful shift in buyer behavior toward multi-vendor usage. So far, the data shows limited evidence of any of these dynamics taking hold to unseat ElevenLabs as the current category leader.

How are the private AI and software companies in your portfolio doing?

FAQ’s

- What is voice AI software?

- Voice AI software enables companies to generate synthetic speech, clone voices, and power conversational interfaces using machine learning models. These tools are increasingly used across marketing, customer support, and product experiences.

- How does ElevenLabs compare to Murf AI and other competitors?

- Based on Signals data from 900 mid-market companies, ElevenLabs leads across adoption, usage, and spend. Competitors like Murf AI, LOVO AI, and Resemble AI have significantly smaller footprints and limited monetization.

- Why is ElevenLabs the primary entry point into voice AI?

- YipitData’s B2B spend data shows that 95% of first-time mid-market voice AI customers start with ElevenLabs. This likely reflects a combination of early market entry, product quality, and strong default positioning among buyers.

- Do companies use multiple voice AI platforms?

- Based on YipitData’s B2B spend data, multi-vendor usage does exist in the category of voice AI, but it’s limited. Nearly 90% of mid-market customers use ElevenLabs exclusively, suggesting low levels of active experimentation across competitors.

- Is ElevenLabs also leading in revenue?

- According to YipitData Signals data, ElevenLabs isn’t just leading in adoption and usage. It’s also leading in spend, accounting for approximately 98% of observed category spend, with revenue growing more than 6x Y/Y. Competitors have not yet demonstrated meaningful monetization.

- Where does YipitData’s voice AI data come from?

- These insights are derived from YipitData’s proprietary B2B spend panel, which aggregates anonymized ERP transaction data from 1,300+ mid-market and enterprise companies, covering approximately 250,000 software and AI vendors.

Connect with us!

.svg)