Who’s Winning and Losing as Anthropic Scales?

.webp)

YipitData Signals data across 1,300+ companies shows which software vendors Anthropic-heavy companies are adding — and dropping.

We analyzed software spending patterns among Anthropic-heavy companies to identify which vendors are gaining momentum — and which ones may be getting displaced — as Claude adoption accelerates.

Anthropic's recent growth has been unprecedented.

So the question we're focused on this week isn't whether Anthropic is winning. It's what Anthropic’s rise is doing to the AI & software market around it.

Last week, we published our first AI Early Adopter report, tracking how the 100 most AI-aggressive companies in our panel are reshaping their software budgets. One finding stood out: "The most consistent examples of AI-driven replacement we saw weren’t large platforms — they were internal tools and workflows."

This week, we went a level deeper, looking specifically at Anthropic-heavy customers to understand which software vendors are gaining and losing as Anthropic embeds itself into enterprise workflows.

The pattern is still early, and this analysis doesn’t prove Anthropic directly caused any specific vendor churn or add. But it does highlight where Anthropic customers are behaving differently from the rest of the market.

Key Takeaways (Data through early Q1 2026)

- Companies focused on narrower, horizontal workflow tools are seeing disproportionate churn from Anthropic-heavy users. Vendors like Polly, Aha!, Coefficient, Elfsight, Data Axle, Dripify, and Clari appear more exposed where Claude can help automate, summarize, or rebuild work internally.

- Developer infrastructure is the clearest winner, with new customers skewing heavily toward Anthropic users. Railway, ngrok, Blacksmith, Supabase, Harness, MongoDB, and SmartBear all screen as beneficiaries as AI-heavy teams build and ship more software.

- Collaboration & Productivity is getting reshaped: Polly, Aha!, and Punchbowl appear exposed, while Fireflies.ai, Evernote, and Smartsheet screen as winners — suggesting spend is shifting away from narrower tools toward ones that capture, organize, and coordinate AI-enabled work.

- The displacement pattern mirrors last week's finding — internal and horizontal tools bear the most churn pressure; infrastructure and compliance tools are gaining alongside Anthropic adoption.

Anthropic Analysis Methodology

To identify where Anthropic's rise is creating winners and losers, we analyzed spend behavior among Anthropic-heavy mid-market companies which we define as those that:

- Grew Anthropic spend significantly between Q4 2025 and early Q1 2026

- Spent at least $1,000 per month — a threshold we use to identify serious, production-level users rather than experimenters

We focused on categories most likely to be affected by Anthropic adoption: Analytics Tools & Software, Development, Governance, Risk & Compliance, Collaboration & Productivity, Sales Tools, IT Infrastructure, Artificial Intelligence, Marketing, Design, and Hosting.

To identify vendors at risk due to the popularity of Anthropic, we compared the share of a vendor's churning customers that had Anthropic overlap against the share of the vendor's existing customer base with Anthropic overlap. A higher delta — what we call "Churn Overexposure to Anthropic" — means churning customers are disproportionately Anthropic-heavy relative to retained customers. This is the signal that Anthropic adoption may be a contributing factor to churn.

To identify vendors benefiting from Anthropic’s success, we ran the same analysis in reverse: which vendors are being added disproportionately by Anthropic-heavy customers? A higher delta on net adds means a vendor is pulling in Anthropic-heavy customers at an above-average rate — suggesting its value proposition is resonating with the same companies going deepest on Anthropic.

This analysis is powered by Signals, YipitData's proprietary B2B spend panel, which tracks real software usage and spend across 1,300+ mid-market and enterprise companies and provides visibility into ~250,000 AI and software vendors.

(See what 479 companies are actually paying for Anthropic, based on real contracts tracked in SpendHound.)

Anthropic Background

Anthropic’s rise has been historic:

- The company has reportedly agreed to a $30 billion fundraising round that would value it at $900B – just 3 months after raising at a $350B valuation.

- The company crossed a $30 billion annualized revenue run rate in April 2026 — up from roughly $9 billion at the end of 2025 — driven largely by enterprise demand.

- The number of customers spending over $1 million annually on Claude has more than doubled in recent months, reaching over 1,000 enterprise accounts.

- Claude Code, its agentic coding tool, hit $1 billion in annualized revenue within six months of launch, reaching over $2.5 billion in run-rate revenue by February 2026, with business subscriptions quadrupling since the start of 2026.

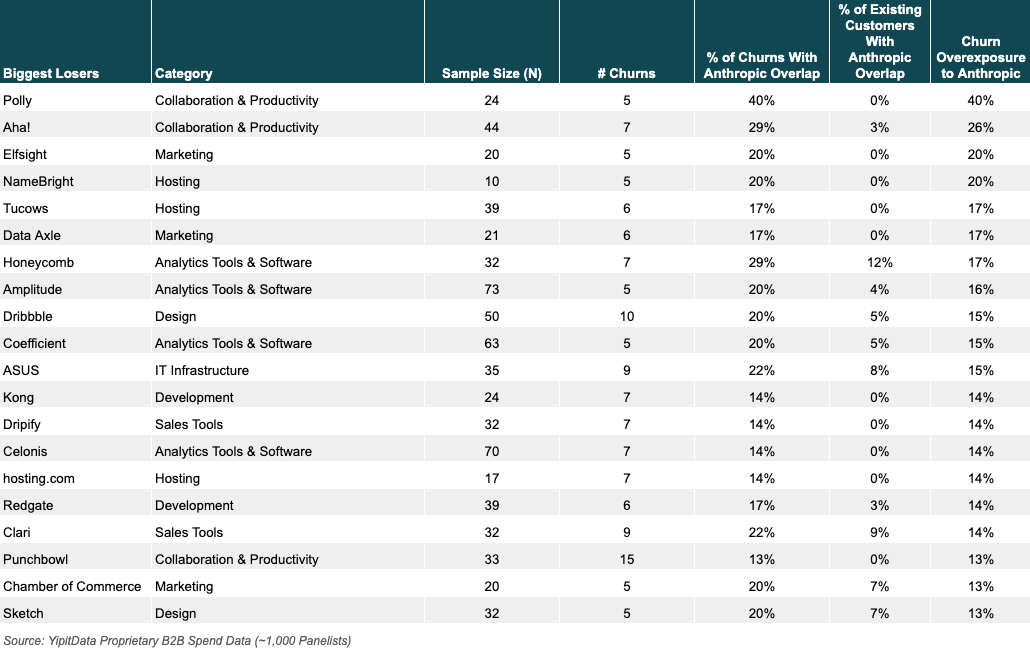

The Losers: Where Anthropic-Heavy Customers Are Churning

The vendors that Anthropic-heavy companies are disproportionately churning from skew toward companies that support relatively narrow or repeatable workflows: surveys, product planning, lightweight marketing, spreadsheet reporting, outbound automation.

Source: YipitData Proprietary B2B Spend Data (900+ Mid-Market Panelists)

Some takeaways:

Collaboration & Productivity: This category tops the list of losers with Polly (40% churn overexposure) and Aha! (26%). The pattern here is consistent with what we heard in last week's interviews: teams are increasingly asking whether AI can handle internal workflow and collaboration tasks before committing to — or renewing — a standalone tool. Both Polly and Aha! serve narrow use cases (employee pulse surveys and product roadmaps, respectively) where AI-assisted workflows are a plausible substitute.

GTM & Marketing: Elfsight, Data Axle, Dripify, and Clari all show churn heavily concentrated in Anthropic-heavy customers — suggesting AI-forward capabilities in this category are particularly strong.

Hosting: NameBright, Tucows, and hosting.com are a more nuanced signal. The appearance of these domain and legacy hosting providers may reflect broader infrastructure consolidation among AI-forward companies rather than direct AI substitution.

Analytics: Honeycomb (17%), Amplitude (16%), and Coefficient (15%) all show meaningful churn overexposure — suggesting that some analytics use cases are moving toward AI-native approaches. But as we'll see below, analytics tools also appear on the winner side, which points to a category in the middle of a more complex reshaping rather than straight displacement.

One important caveat: sample sizes in this analysis are relatively small for some vendors, and churn dynamics are influenced by many factors beyond Anthropic adoption. The vendors listed here are not necessarily losing because of Anthropic (particularly since Anthropic spend is a strong sign of AI adoption more broadly) — but their churning customers are disproportionately Anthropic-heavy, and that is a signal worth tracking.

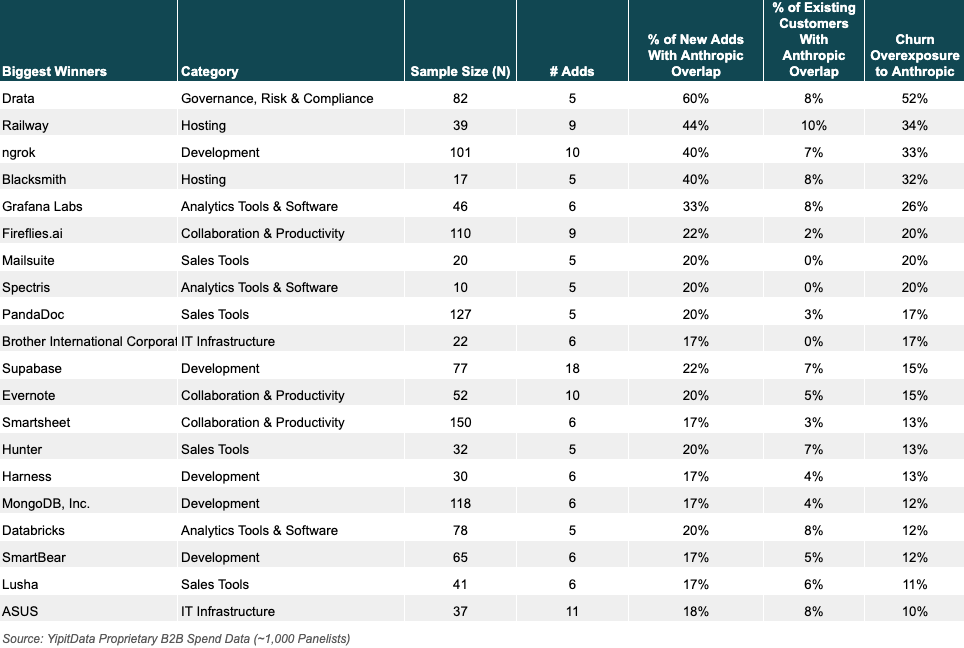

The Winners: Where Anthropic-Heavy Customers Are Adding

The vendors with the highest net add overexposure to Anthropic skew heavily toward infrastructure, development, and compliance — categories where Anthropic adoption tends to accelerate build cycles and raise the stakes for governance and security tooling.

Some takeaways:

Drata is at the top of the winners list — a finding that dovetails with our compliance AI analysis from two weeks ago, where Drata was already showing strong momentum in the category. The connection is intuitive: as companies build production-level AI systems on Anthropic, compliance and audit readiness for those systems becomes a near-term necessity.

The key theme here is that Anthropic’s rise is benefiting companies that help developers build, deploy, connect, test, and scale software built with AI. Anthropic-heavy customers are disproportionately adding tools that help teams build and ship faster — deployment platforms like Railway, backend/data platforms like Supabase and MongoDB, developer connectivity tools like ngrok, CI/CD infrastructure like Blacksmith and Harness, and testing/API quality platforms like SmartBear.

How Anthropic Is Reshaping Software Budgets

The companies feeling the most pressure as Anthropic adoption rises have products that are narrow, horizontal and internal — the kind of tools where "good enough" AI substitution is easiest to justify.

The companies gaining alongside Anthropic skew toward infrastructure, developer tooling, data, observability, and compliance — products that become more important as Anthropic’s customer base builds, deploys, and scales more software.

The longer Anthropic’s momentum continues, the more visible this reallocation may become. Customers appear likely to keep investing in the systems that help them build and manage around Claude, while reassessing tools that feel duplicative or replaceable.

Want to see what other companies are winning or losing?

See our B2B spend data in action

FAQ’s

- Which software vendors are losing customers as Anthropic adoption grows?

- Based on YipitData Signals B2B spend data, vendors with narrow, horizontal workflows are seeing the most churn from Anthropic-heavy customers. Collaboration and productivity tools like Polly and Aha!, GTM and marketing tools like Elfsight, Dripify, and Clari, and lightweight analytics tools like Coefficient all show disproportionate churn overlap with companies growing their Anthropic spend. The data seems to suggest that these are categories where AI-assisted workflows are easiest to justify as a substitute.

- Which software vendors are winning as Anthropic adoption grows?

- Developer infrastructure and compliance tools are the clearest beneficiaries as Anthropic adoption grows. YipitData Signals data shows Anthropic-heavy companies disproportionately adding vendors like Railway, Supabase, MongoDB, ngrok, Harness, Blacksmith, and SmartBear — tools that help teams build and ship AI-powered software faster. Drata, a compliance platform, tops the winners list, reflecting the governance requirements that come with production-level AI deployments.

- What does "Churn Overexposure to Anthropic" mean?

- Churn Overexposure to Anthropic is a metric YipitData developed to identify vendors at risk from Anthropic adoption. Using Signals B2B spend data, we compare the share of a vendor's churning customers that have Anthropic overlap against the share of its existing customer base with Anthropic overlap. A higher delta means churning customers are disproportionately Anthropic-heavy — a signal that Anthropic adoption may be a contributing factor to churn, even if it isn't the sole cause.

- Is Anthropic directly causing vendors to lose customers?

- The analysis based on YipitData Signals data does not prove direct causation: that Anthropic is directly causing vendors to lose customers. Churn dynamics are influenced by many factors. However, Anthropic spend is itself a strong indicator of broader AI adoption, and vendors whose churning customers skew heavily Anthropic-heavy are worth monitoring closely. The pattern is most consistent with displacement in narrow, internal, and easily-substituted workflow tools.

- Where does YipitData's AI and software data come from?

- YipitData’s insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors — capturing momentum earlier than traditional signals like funding or headcount.

Connect with us!

.svg)