AI Early Adopter Series: How AI Is Reshaping Software Budgets in 2026

By Jenny Liu, Director of Product @Yipitdata

We're tracking 100 of the most AI-aggressive companies in our B2B spend panel — following their software budgets, interviewing their finance and operations leaders, and publishing what we find. This is the first installment of our AI Early Adopter series.

Among the 100 most AI-aggressive companies in YipitData's B2B spend panel, one pattern keeps showing up: AI isn't replacing SaaS — but it is making companies more reluctant to increase their SaaS spend. We see teams layering AI into workflows and building capabilities internally, but the spend cuts most analysts expected in legacy software haven't yet fully materialized.

This is the first installment of our AI Early Adopter series, where we combine observed spend data from our 1,300+ company B2B spend panel with direct interviews with the finance, procurement, and operations leaders driving those decisions. Our cohort: 100 companies defined by both early AI adoption and rapid AI spend growth between February 2024 and February 2026.

This work is powered by our proprietary B2B spend panel, which tracks real software usage and spend across 1,300+ mid-market and enterprise companies, providing visibility into ~250,000 AI and software vendors.

What makes this new series particularly powerful is that we’re not just observing spend patterns — we can also speak directly with the decision makers behind them. This allows us to go beyond what companies are spending to understand how they’re making decisions, where they expect budgets to shift, and the rationale behind those changes.

Our goal: understand not just which AI tools companies are adopting, but how budgets are shifting underneath the surface.

Our first takeaway: AI isn’t replacing SaaS — but it is slowing it, reshaping it, and challenging it.

Defining Our AI Early Adopter Cohort (n = 100)

To understand how AI is reshaping software budgets, we first needed to identify the companies leaning in earliest and most aggressively.

For this series, we define our AI early adopters as a cohort of 100 companies drawn from our proprietary B2B spend panel. Specifically, we start with the top 200 companies by AI spend in February 2024, and from that group select the 100 companies that have grown their AI spend the most (on an absolute basis) through February 2026.

For the purposes of this analysis, we define AI spend as spend on OpenAI, Anthropic, and Anysphere (Cursor).

(Check out what teams are actually paying for OpenAI, Anthropic, and Anysphere (Cursor) based on real contracts tracked in SpendHound. And browse the SpendHound marketplace for more real pricing reports.)

This approach allows us to focus on companies that were both:

Early users of AI, with meaningful baseline spend, and

Rapid adopters, significantly increasing their investment over time

Importantly, this cohort is not meant to represent the average company. Instead, it captures a leading indicator group — companies that tend to adopt new technologies earlier and more aggressively, and whose behavior often precedes broader market trends by several months.

As a result, the patterns we observe in this cohort — both in terms of where spend is increasing and where it is being pulled back — can provide an early signal of how AI may reshape software budgets more broadly over time.

Where AI Early Adopters Are Spending More — and Less

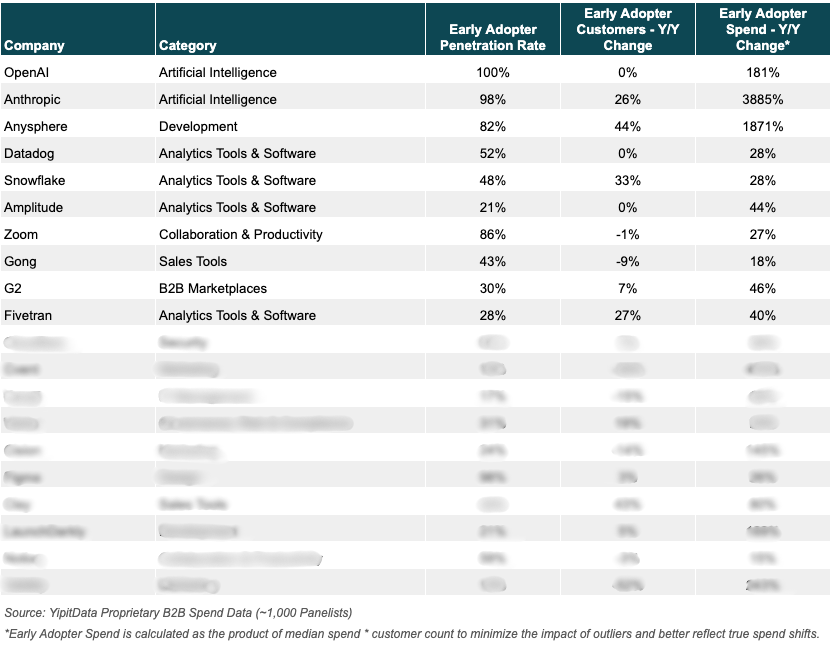

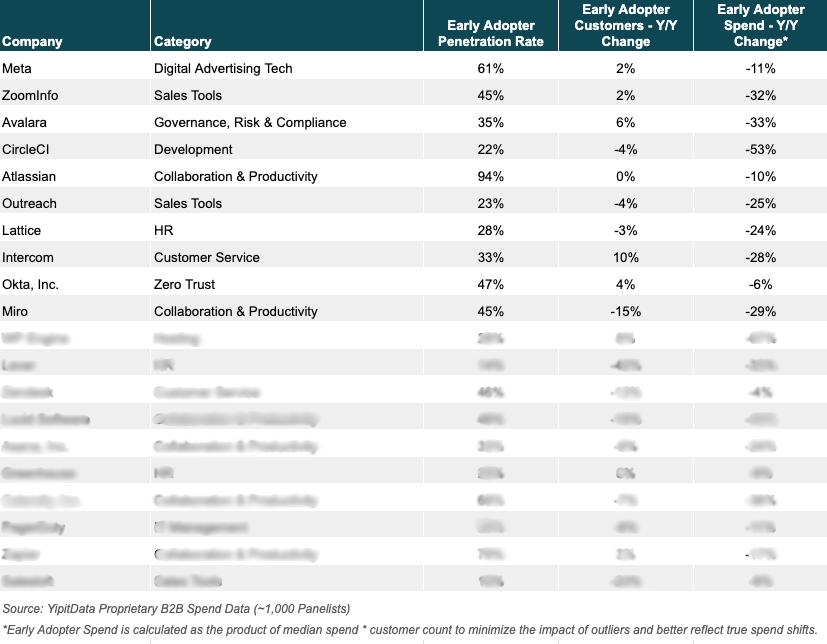

To see where budgets are actually moving, we analyzed which vendors AI early adopters are ramping and trimming spend on. The tables below show the top 20 vendors by spend growth and decline. We ranked vendors using median spend multiplied by customer count to minimize the impact of outliers and better reflect true spend shifts.

Exhibit 1: Top 20 Companies Where AI Early Adopters Are Growing Spend

*For the full list, email jenny@yipitdata.com

Exhibit 2: Top 20 Companies Where AI Early Adopters Are Cutting Spend

*For the full list, email jenny@yipitdata.com

Interview Takeaways

To complement the spend data, we conducted a series of 1:1 interviews in March and April with finance, procurement, and operations leaders within the AI Early Adopter group to better understand the organizational dynamics driving AI budget allocation, platform consolidation, and vendor adoption decisions.

Participants (n = 5)

For this initial piece, we spoke with finance, procurement, and operations leaders across five AI-forward, midsize companies (100-999 employees) from our AI Early Adopter group, including:

A conversational AI platform (Software), speaking with a financial analyst and IT/operations lead

A nonprofit fundraising software company (Software), speaking with a vendor management lead within business operations

A virtual assistant platform (Business & Professional Services), speaking with a VP of Finance

A payments and rewards platform (Financial Services), speaking with a finance manager

A field service management software company (Software), speaking with a CFO/COO

AI Isn’t Replacing SaaS But It’s Slowing SaaS Growth

Across every company we spoke with, teams are experimenting with multiple LLMs, layering AI into workflows, and leveraging AI to build new capabilities internally. But that growth generally isn’t being funded by cutting software.

Instead, companies are becoming more cautious about adding new tools.

One finance leader described the shift simply: rather than replacing software outright, AI is allowing them to “maintain what we have without growing.”

That sentiment came up repeatedly. Before committing to new tools — especially multi-year contracts — teams are increasingly asking a different question first: can we solve this with AI?

As another operator explained, “before we commit to a multi-year SaaS contract… let’s explore if we can solve it with AI first.”

This change in behavior matters. It doesn’t show up as churn. It doesn’t show up as cancellations. But it does show up in slower expansion — fewer seats, fewer new tools, and more friction in the renewal & buying process.

Core SaaS Remains Surprisingly Sticky

If AI were truly replacing SaaS, we would expect to see early cracks in core systems — CRM, ERP, customer support. Instead, those systems remain firmly in place.

Across interviews, operators consistently described these tools as difficult — and often risky — to replace. The issue isn’t whether better alternatives exist; it’s the cost of switching.

One operator summed it up bluntly: “If a customer comes in and I cannot open the ticket…I’m screwed.”

Another pointed to the sheer complexity of replacing foundational systems: “Switching an ERP is brutal… that’s the stickiest one.”

Even tools that teams don’t particularly love tend to persist. One company admitted they revisit alternatives every year, but still end up renewing because they “still didn’t find an alternative.”

That dynamic creates a clear divide:

Core systems of record remain sticky

The pressure shows up elsewhere

The First Real Disruption Is Happening in Internal Tools

While the core stack remains intact, the edges are starting to shift. The most consistent examples of AI-driven replacement we saw were not large platforms — they were internal tools and workflows.

In some cases, companies are already rebuilding parts of their stack from scratch. One company described replacing multiple tools outright, explaining that they had “replaced Expensify… replaced Lattice… it’s fully operational and live.”

But even outside of full replacements, the pattern shows up in smaller decisions. Instead of buying new tools, teams are increasingly solving problems internally.

One finance leader described evaluating a new modeling tool, only to decide against it after realizing that AI combined with existing tools like Google Sheets could handle the use case well enough.

Others described trimming smaller tools over time — not through large strategic cuts, but through gradual pruning as workflows shift.

These decisions tend to happen in areas where:

Use case is internal

Workflow is flexible

Risk of failure is low

That’s what makes them vulnerable. Internal, horizontal tools are the first place where “good enough” AI can compete with SaaS.

AI Adoption Is Messy and Shifting Quickly

If there’s one consistent theme, it’s this: AI adoption is messy, decentralized, and hard to control.

Some companies are introducing structure — budgets, trials, ROI frameworks — while others let teams experiment freely. But even the most organized are still figuring it out.

As one operator put it: “We’re building ROI calculators” — because the framework didn’t exist before.

And without tight oversight, costs can escalate quickly: “Take your eye off the ball… AI spend doubles.”

Part of the challenge is fragmentation. AI usage is often spread across teams, with no single owner — making it harder to forecast and control than traditional SaaS. At the same time, switching costs are far lower. Unlike SaaS, where contracts are long and integrations are deep, AI vendors are interchangeable and buyers treat them that way.

Companies are actively comparing OpenAI, Claude, Gemini, and others, switching based on performance and cost. In some cases, the impact is dramatic: One of our interviewees noted: “We moved from $60–70k a month to ~$2k just by switching models.”

The result is a fundamentally different market dynamic: AI vendors are competing in a fluid, price-sensitive environment.

What This Means

The early impact of AI on software isn’t a collapse. It’s a shift.

SaaS remains sticky at the core but expansion is slowing at the margins

AI spend is growing — and difficult to control

Vendor loyalty in AI is low and constantly shifting

Taken together, these trends point to a more nuanced reality than the original narrative. AI isn’t replacing SaaS — it’s reshaping how companies spend, how they grow, and how they decide what software they actually need.

Want to see what other companies are winning or losing as AI takes off?

FAQ’s

-

Based on YipitData Signals B2B spend data and interviews with finance and operations leaders at 100 AI-forward companies, early AI adopters are not broadly cutting SaaS spend. But they are becoming more cautious about adding new tools — asking whether AI can solve a problem before committing to new software contracts. Core systems like CRM and ERP remain in place. This new pressure shows up in slower expansion, fewer new seats, and more friction at renewal.

-

The clearest examples of AI-driven displacement that we see are with internal tools and workflows rather than large platforms. Companies in YipitData's AI Early Adopter cohort described replacing point tools like expense and performance management software by rebuilding those workflows with AI. The pattern is most common where the use case is internal, the workflow is flexible, and the risk of failure is low.

-

AI spend management is still nascent. Companies in the YipitData AI Early Adopter cohort are actively building ROI frameworks and budget structures that didn't previously exist. Without oversight, spend can escalate quickly — one interviewed operator noted that taking your eye off AI costs can cause spend to double. AI usage is often fragmented across teams with no single owner, making it harder to forecast and control than traditional SaaS.

-

Vendor loyalty in AI is low. Companies actively compare OpenAI, Claude (Anthropic), Gemini, and others, and switch based on performance and cost. Unlike SaaS, where contracts are long and integrations are deep, AI models are treated as interchangeable. One operator in the YipitData AI Early Adopter cohort described moving from $60–70K per month to approximately $2K by switching models.

-

YipitData’s insights are powered by Signals, a proprietary B2B spend panel derived from anonymized ERP transaction data across 1,300+ mid-market and enterprise companies. This provides visibility into real software purchasing behavior across ~250,000 vendors — capturing momentum earlier than traditional signals like funding or headcount. For this AI Early Adopter series, this spend data has been supplemented with 1:1 interviews with finance, procurement, and operations leaders representing the 100 companies from our panel that grew AI spend the most (on an absolute basis) through February 2026. AI spend is defined as spend on OpenAI, Anthropic, and Anysphere (Cursor).