Who’s Winning in AI Video? Synthesia vs HeyGen vs Runway (2026 Data)

.webp)

New YipitData analysis of 1,300+ companies shows HeyGen surging in adoption, Synthesia leading in spend, and Runway dominating AI video generation. See the latest trends.

New YipitData analysis of 900+ mid-market companies shows HeyGen surging in adoption, Synthesia leading in spend, and Runway dominating AI video generation. See the latest trends.

Who's gaining traction, how is monetization evolving, and where are competitive dynamics starting to take shape in the AI video market?

In the AI avatar creation landscape, HeyGen is outpacing Synthesia on customer growth by a wide margin, but Synthesia still generates far more revenue per customer. In AI video generation, Runway has established a clear lead over its peers.

Those are the headline findings from YipitData's B2B spend dataset, which tracks real spend from 1,300+ mid-market and enterprise companies across ~250,000 vendors — including, for this week's analysis, Synthesia, HeyGen, Runway, Luma AI, Pika Labs, and Stability AI.

To surface patterns like switching behavior, multi-vendor adoption, and cohort growth, we used our soon-to-be-launched Insight Agent.

Here's what we found.

AI Avatar Platforms: Synthesia vs HeyGen

AI Avatar Creation: Synthesia vs. HeyGen

Background

AI avatar video platforms like Synthesia and HeyGen allow companies to generate studio-quality video content using AI-generated avatars which help to significantly streamline traditional video production workflows.

Synthesia, founded in 2017, has established itself as the early category leader, particularly within enterprise use cases. The company recently raised a $200M Series E in January 2026, and its headcount has grown 44% Y/Y to 706 employees.

HeyGen, founded in 2020, has emerged as a fast-growing challenger, with its momentum apparently driven in part by a more accessible, creator-centric product model. The company raised a $60M Series A in January 2026, with headcount increasing 58% Y/Y to 332 employees.

B2B Spend Takeaways: HeyGen Is Gaining Adoption, While Synthesia Still Leads on Monetization

Within the mid-market, the data shows a clear divergence between adoption and monetization.

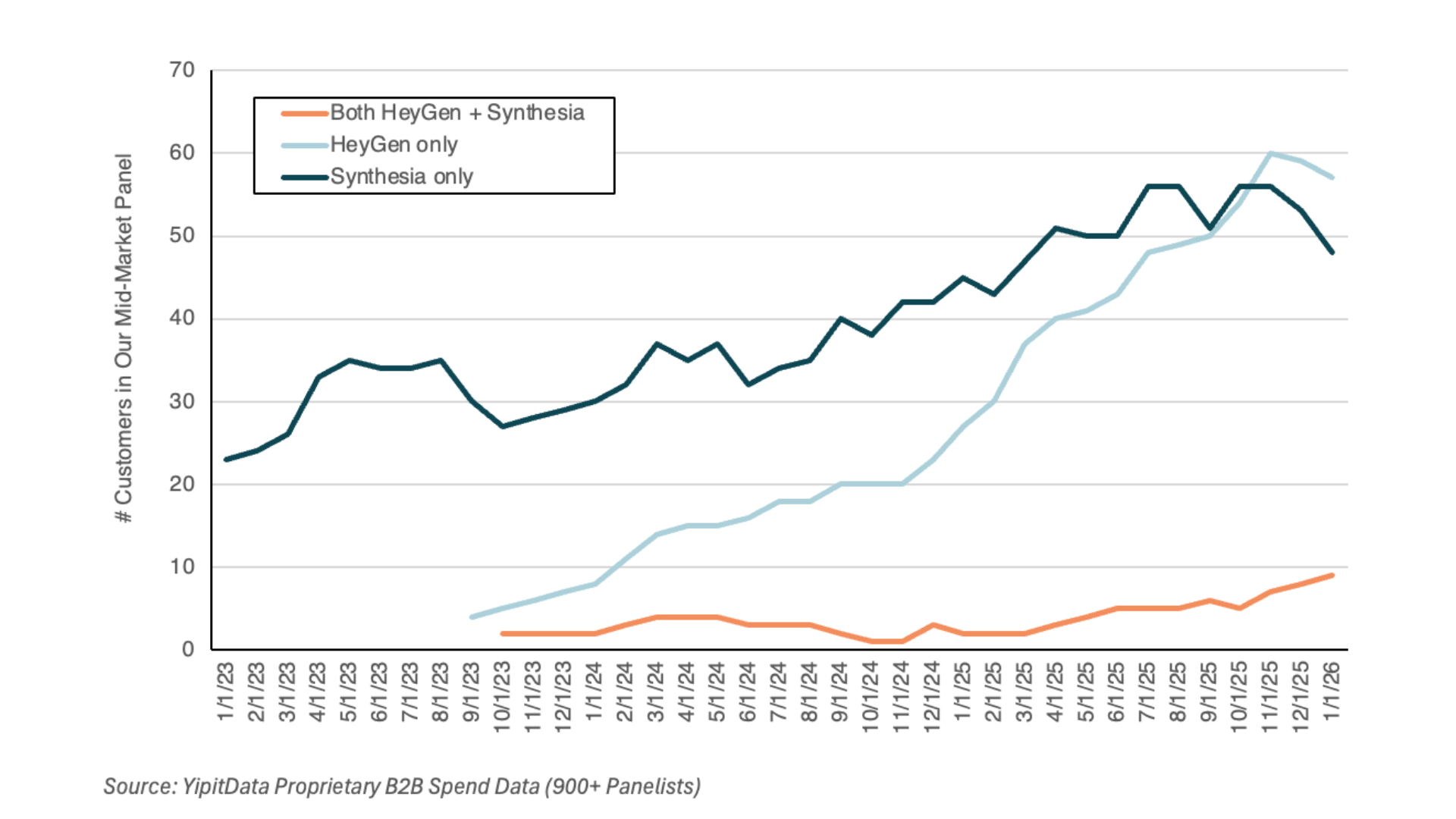

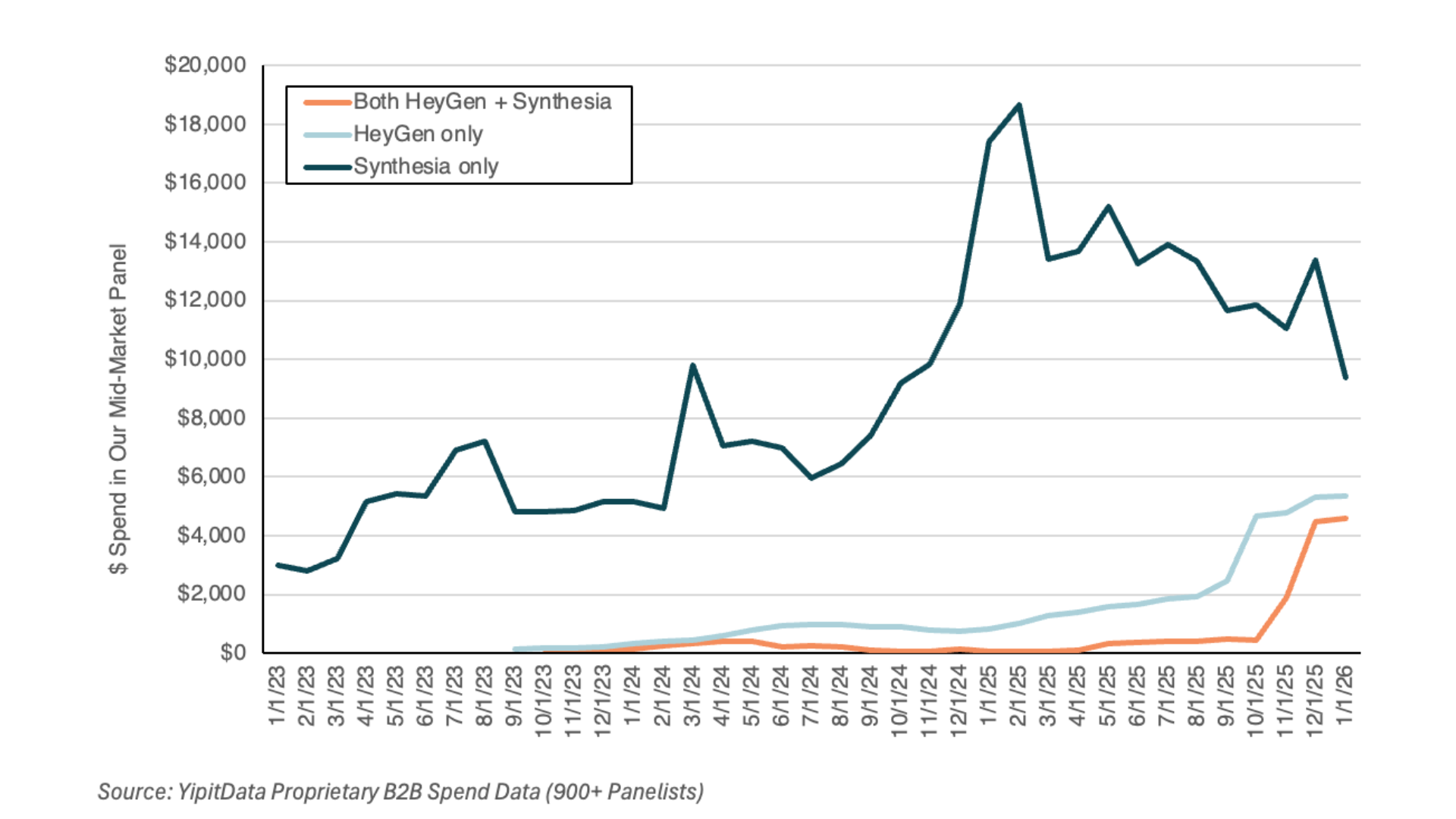

HeyGen is growing significantly faster in terms of customer count. As of January 2026, its mid-market customer base grew 152% Y/Y, compared to approximately 30% growth for Synthesia. This rapid expansion allowed HeyGen to close much of the gap in customer count by late 2025.

At the same time, Synthesia continues to lead on spend. Its average contract values are more than three times higher than HeyGen’s, which translates into a meaningful lead in total mid-market revenue.

However, there are early signs that HeyGen is beginning to make progress on monetization. In late 2025, the data shows a noticeable acceleration in HeyGen’s monetization efforts, suggesting it’s starting to convert its growing customer base into higher-value contracts.

Taken together, the category currently shows a split dynamic: HeyGen is gaining traction on adoption, while Synthesia maintains a strong lead on revenue.

Growth Is Being Driven by Expansion, Not Displacement

An important question is whether HeyGen’s growth is coming at the expense of Synthesia.

So far, the data suggests that is not the case.

The majority of customers — approximately 92% — are using one platform or the other only. While there is some increase in multi-vendor adoption, it remains relatively limited.

When overlap does occur, the most common pattern is Synthesia customers adding HeyGen to their stack, rather than switching away from Synthesia entirely. Direct displacement remains minimal.

There was also a small uptick toward the end of 2025 in HeyGen customers adding Synthesia, though this behavior is still relatively limited.

Overall, this suggests that HeyGen’s growth is being driven primarily by new customer acquisition and incremental adoption, rather than direct competitive replacement.

AI Video Generation: Runway, Luma AI, Pika Labs, Stability AI

Background

AI video generation platforms — including Runway, Luma AI, Pika Labs, and Stability AI — enable users to create video content from text prompts or simple inputs. These tools are opening up new workflows across creative production, marketing, and design.

Runway, founded in 2018, has emerged as an early leader in this category, combining strong model capabilities with a more developed application layer. The company recently announced a $315M Series E in February 2026.

Luma AI and Pika Labs are newer entrants that have gained traction through rapid model innovation and frequent product releases. Luma AI raised a $900M Series C in November 2025, while Pika Labs last raised an $80M Series B in June 2024.

Stability AI — best known for its open-source approach to text-to-image models — has seen more limited traction in video. The company last raised an undisclosed round in June 2024.

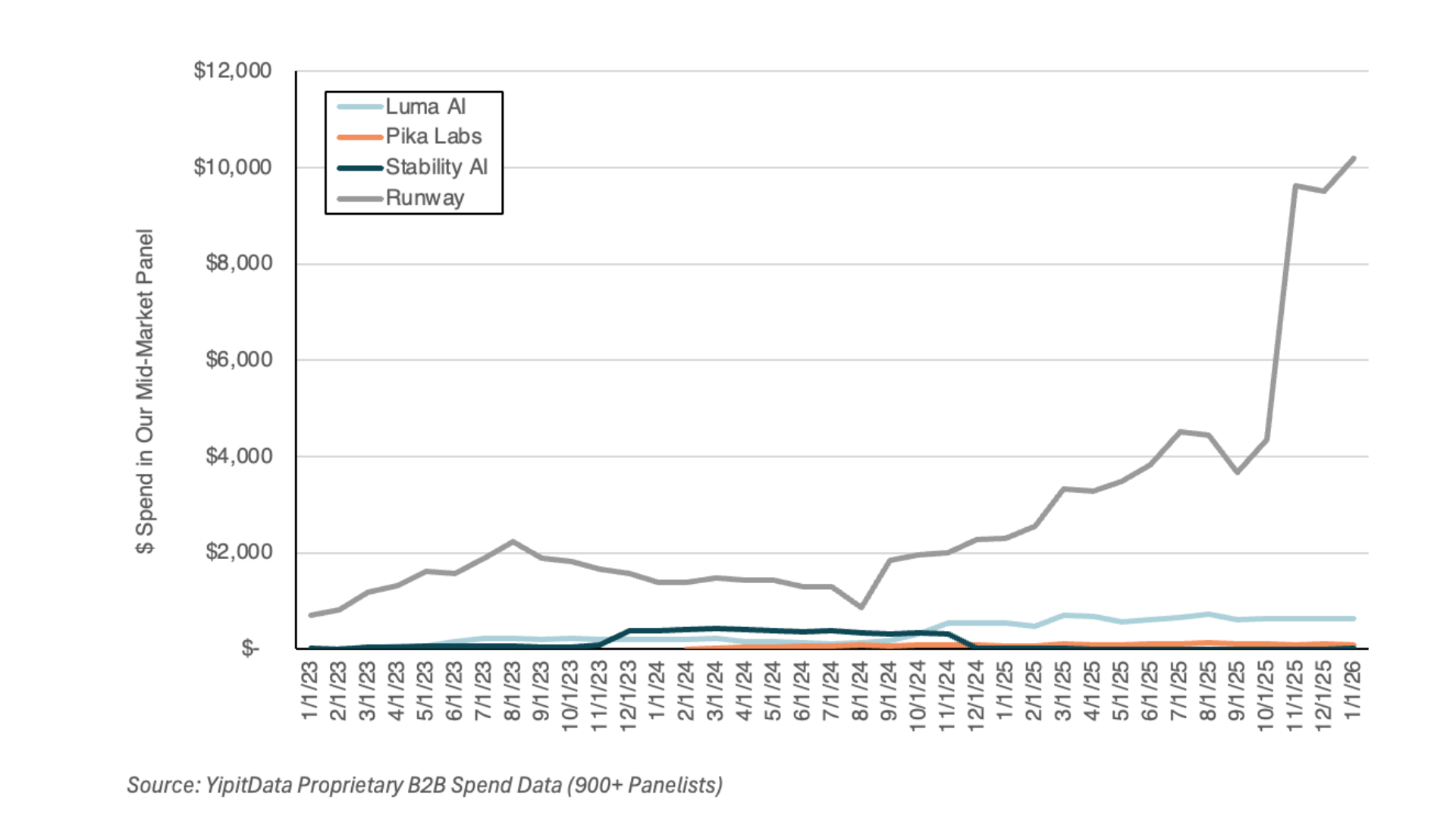

B2B Spend Takeaways: Runway Is the Clear Category Leader in Adoption and Monetization

Within AI video generation, the data shows a more consolidated pattern.

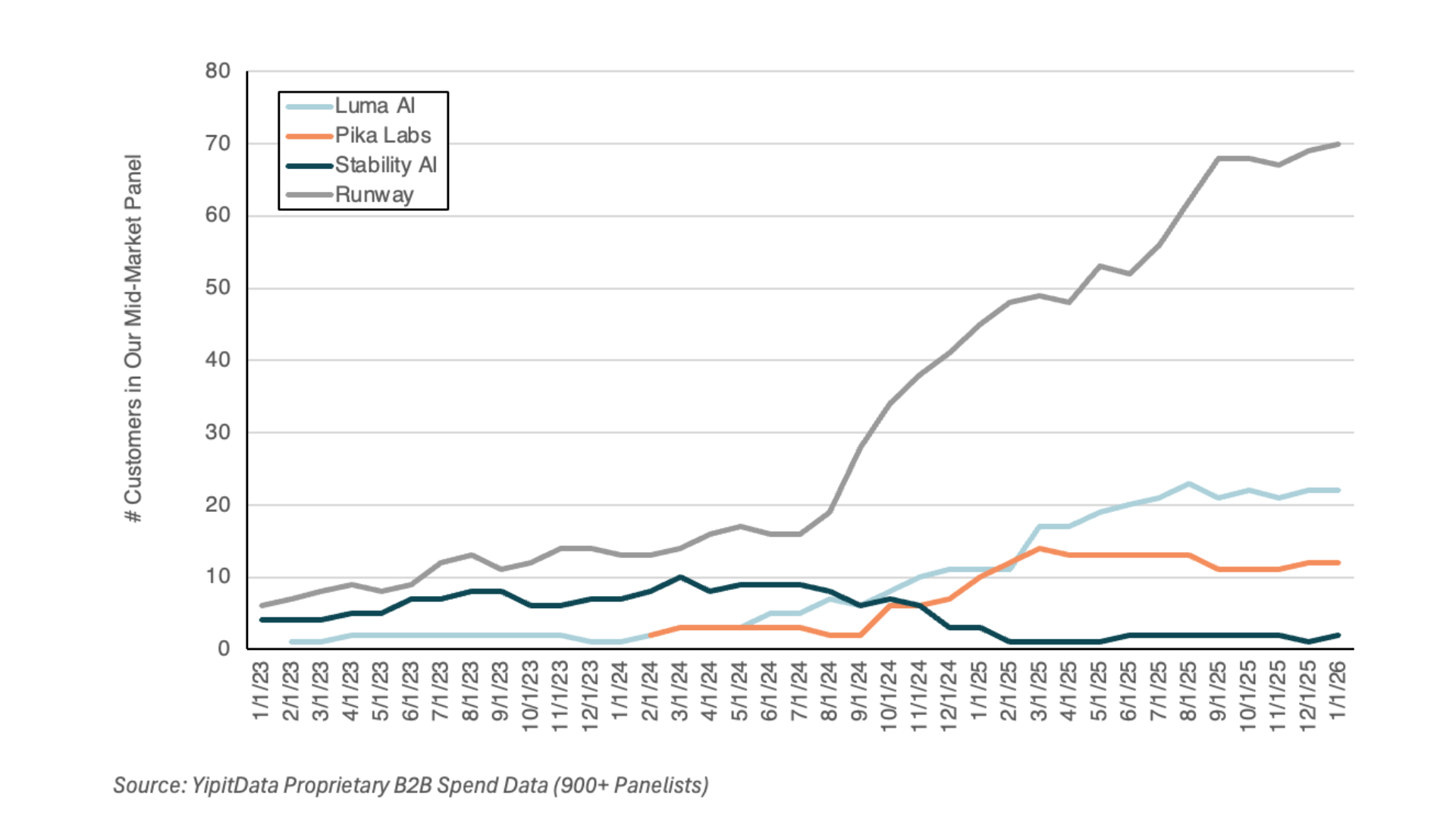

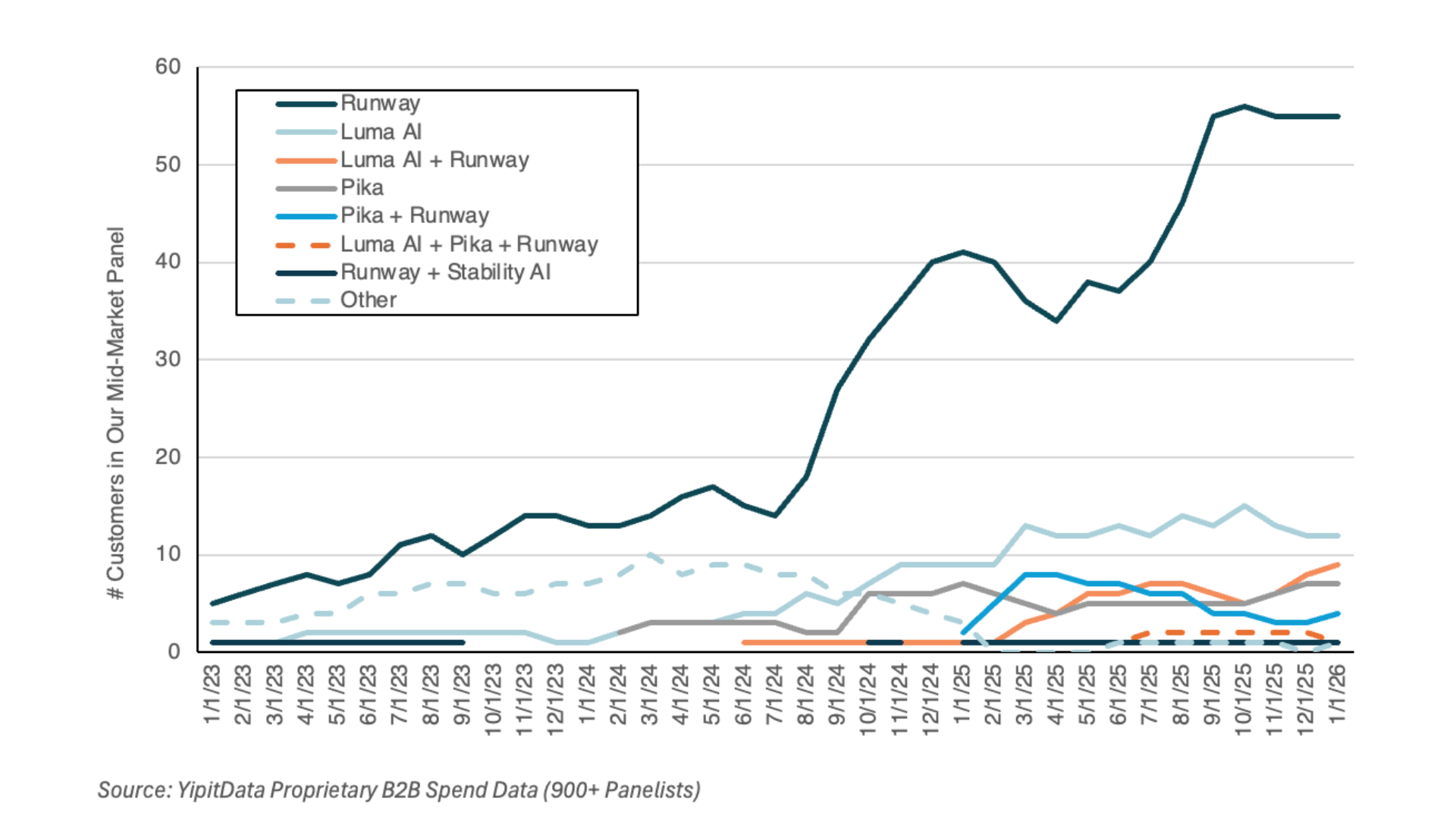

Runway leads the category in mid-market adoption by a significant margin. Its customer count has scaled rapidly over the past year, reaching approximately 70 customers in our panel by early 2026 — far outpacing peers.

Luma AI and Pika Labs have seen moderate traction, but both remain meaningfully behind Runway and appear to be plateauing relative to its growth. Stability AI shows limited and declining presence in this category.

In addition to leading on adoption, Runway is also the only platform in this group meaningfully monetizing its mid-market customer base. It generates the vast majority of observed spend in the category, and recent increases in contract value drove more than a 2x increase in spend within the panel in late 2025.

Multi-Vendor Usage Remains Limited

Another notable dynamic in AI video generation is how these tools are being adopted.

Unlike the avatar creation category, where there are early signs of multi-vendor usage, most customers in the AI video generation segment are using a single platform. In practice, Runway is typically adopted as the primary tool rather than being used alongside competitors.

Co-usage does exist, but it remains relatively small.

This suggests that, at least for now, the category is developing around a primary-platform model rather than a multi-tool ecosystem.

What This Means for the AI Video Market

We’re continuing to track how AI video evolves — particularly whether HeyGen can translate mid-market adoption into sustained monetization, and whether Runway’s early lead holds as competition intensifies.

As the category matures, the data points toward consolidation rather than fragmentation — at least in video generation, where Runway's lead is already significant and multi-vendor usage remains limited. The avatar segment is one to watch: Whether HeyGen can convert its adoption lead into revenue parity with Synthesia will be a meaningful signal for where that market is heading.

What other AI and software trends are emerging across your portfolio?

FAQ’s

- Which AI video platform is growing the fastest: HeyGen or Synthesia?

- Based on YipitData’s B2B spend data, HeyGen is growing significantly faster in terms of mid-market customer adoption. As of January 2026, HeyGen’s customer count grew 152% Y/Y, compared to roughly 30% Y/Y growth for Synthesia. This rapid growth allowed HeyGen to close much of the gap in total customer count by late 2025.

- Why does Synthesia still lead in revenue despite HeyGen’s growth?

- Synthesia continues to lead in mid-market spend because its average contract values (ACVs), according to YipitData data, are more than three times higher than HeyGen’s. While HeyGen is adding customers quickly, Synthesia generates more revenue per customer, which allows it to maintain a strong lead in total spend. However, HeyGen began accelerating monetization in late 2025, indicating progress in closing this gap.

- Is HeyGen taking customers away from Synthesia?

- The YipitData B2B spend data suggests that HeyGen’s growth is not driven by displacing Synthesia. Most companies (about 92%) use only one platform, and when multi-vendor adoption occurs, the more common pattern is Synthesia customers adding HeyGen rather than switching away from Synthesia. Direct displacement between the two platforms remains limited.

- Which company is leading in AI video generation tools?

- Runway is the clear leader in AI video generation among mid-market companies, according to YipitData B2B spend data. It has the largest customer base — reaching approximately 70 customers in our panel by early 2026 — and generates the vast majority of observed spend in the category. It is also the only platform in this group meaningfully monetizing at scale.

- Are companies using multiple AI video tools at the same time?

- Multi-vendor usage varies by category. In AI avatar platforms, there are early signs of companies using both Synthesia and HeyGen. In contrast, AI video generation tools show limited overlap, with most companies adopting a single platform — typically Runway — as their primary solution.

- Where does YipitData’s software spend data come from?

- The insights in this analysis are derived from YipitData’s B2B spend data, which aggregates anonymized software spending data from companies that share ERP-sourced transaction data with YipitData or through enterprise data partnerships. The platform tracks spending and adoption trends across 1,300+ mid-market and enterprise companies for ~250,000 AI and software vendors.

Connect with us!

.svg)