Footwear Market Trends 2026: Running Shoes Drive Growth as Brand Share Shifts

.webp)

Running footwear is driving growth in 2025, while lifestyle segments soften and brand share shifts across retailers. Explore the latest footwear market trends, including channel performance, competitive dynamics, and changing consumer spend.

The US footwear market is entering a new phase of growth defined by shifting consumer preferences, evolving retail dynamics, and increasing competition across brands.

Recent data shows that while overall footwear growth remained modest, performance varied significantly across categories, channels, and brands. Running footwear is emerging as a key growth driver, while lifestyle segments and direct-to-consumer strategies face new pressures.

Running Footwear Is Driving Category Growth

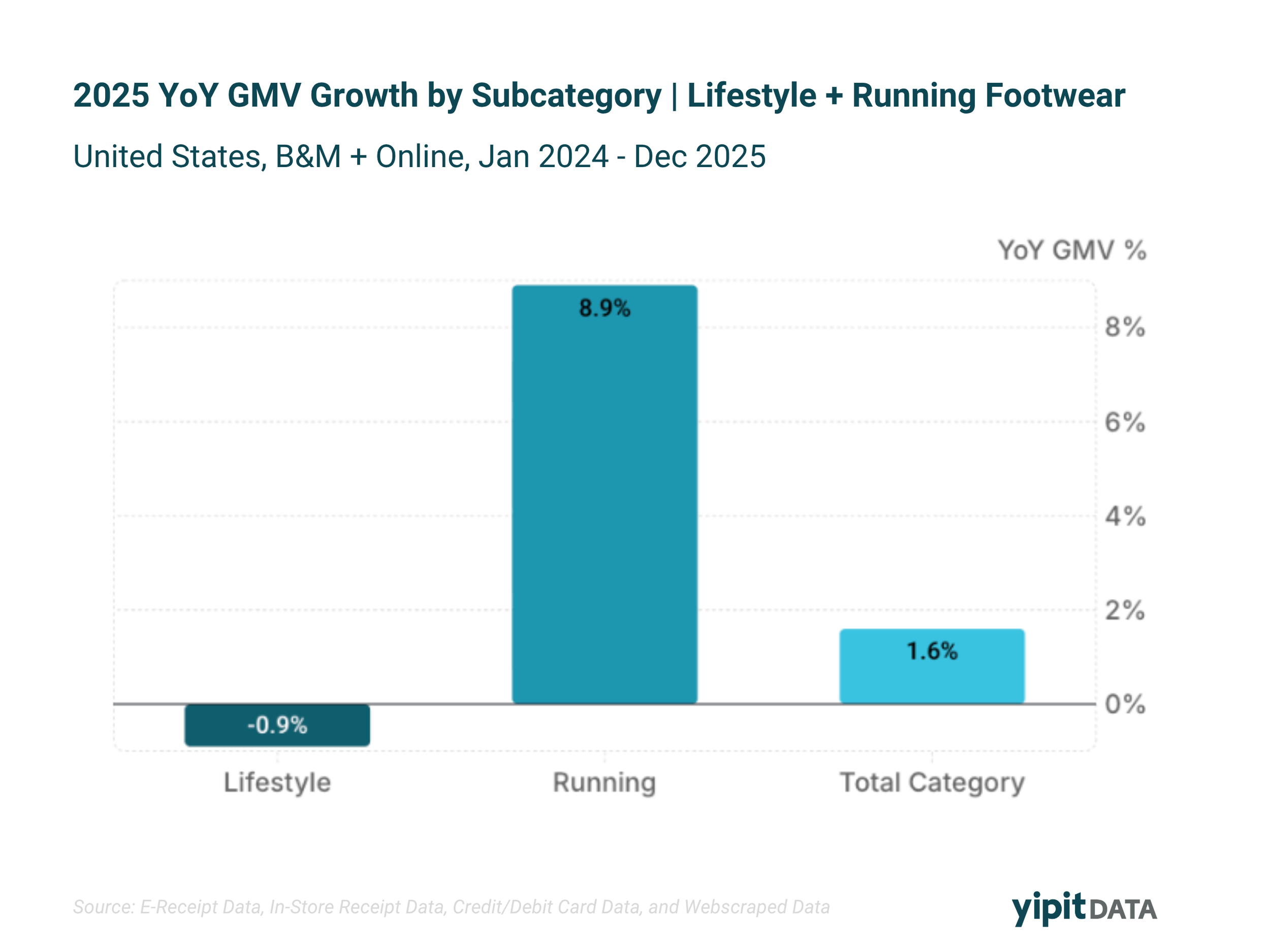

Growth in 2025 was not evenly distributed across the footwear market. Running footwear significantly outperformed lifestyle segments, highlighting a shift in consumer demand.

- Running footwear grew +8.9% year over year

- Lifestyle footwear declined -0.9%

This divergence indicates that category growth is increasingly concentrated in performance-driven products rather than casual or fashion-oriented footwear.

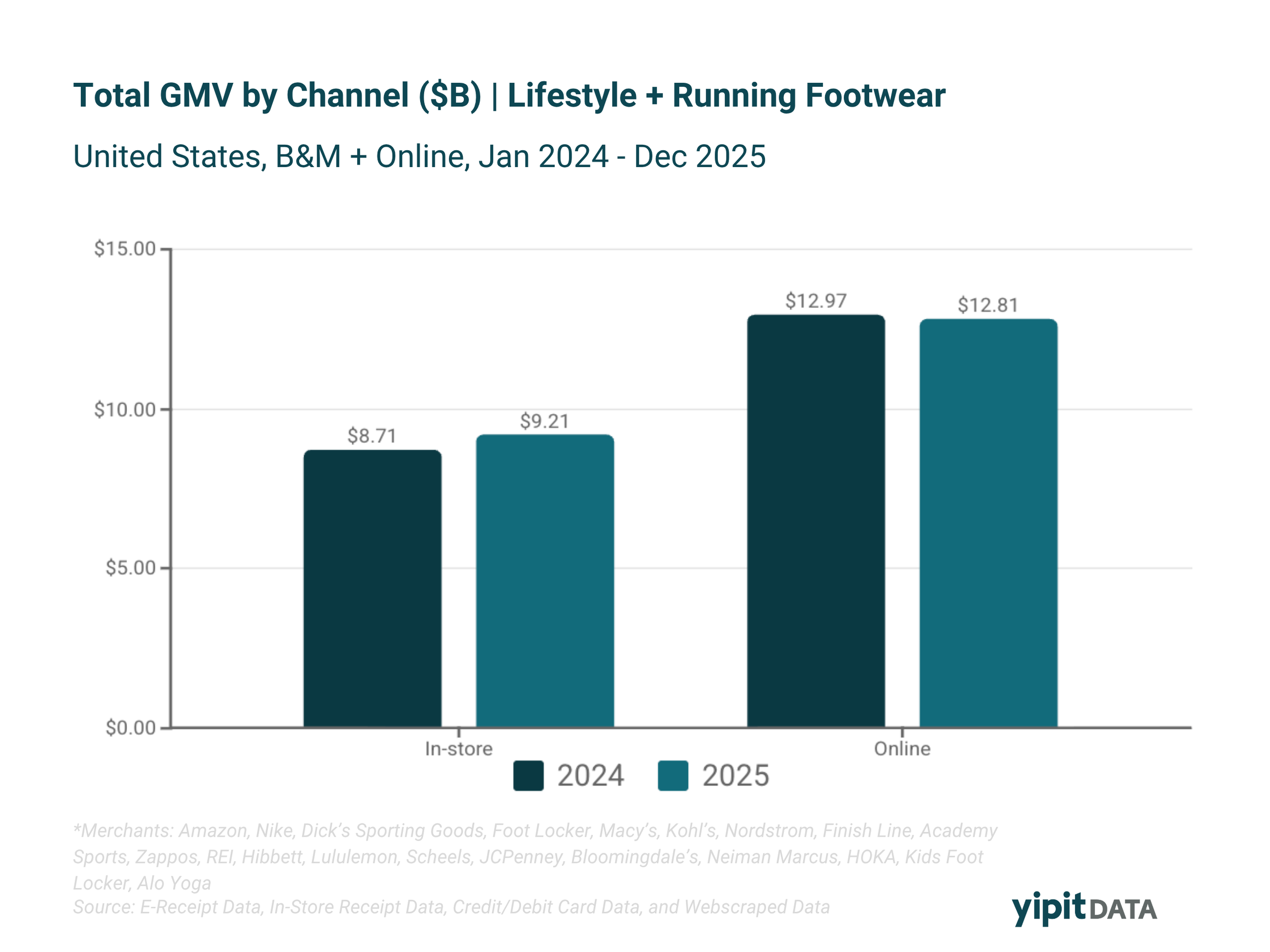

In-Store Sales Are Rebounding While Online Softens

Channel performance diverged in 2025, with physical retail gaining momentum.

- In-store GMV increased +5.8%

- Online GMV declined -1.3%

Despite these shifts, overall channel mix remained relatively stable, suggesting that growth is occurring within existing structures rather than through a major reallocation between online and offline.

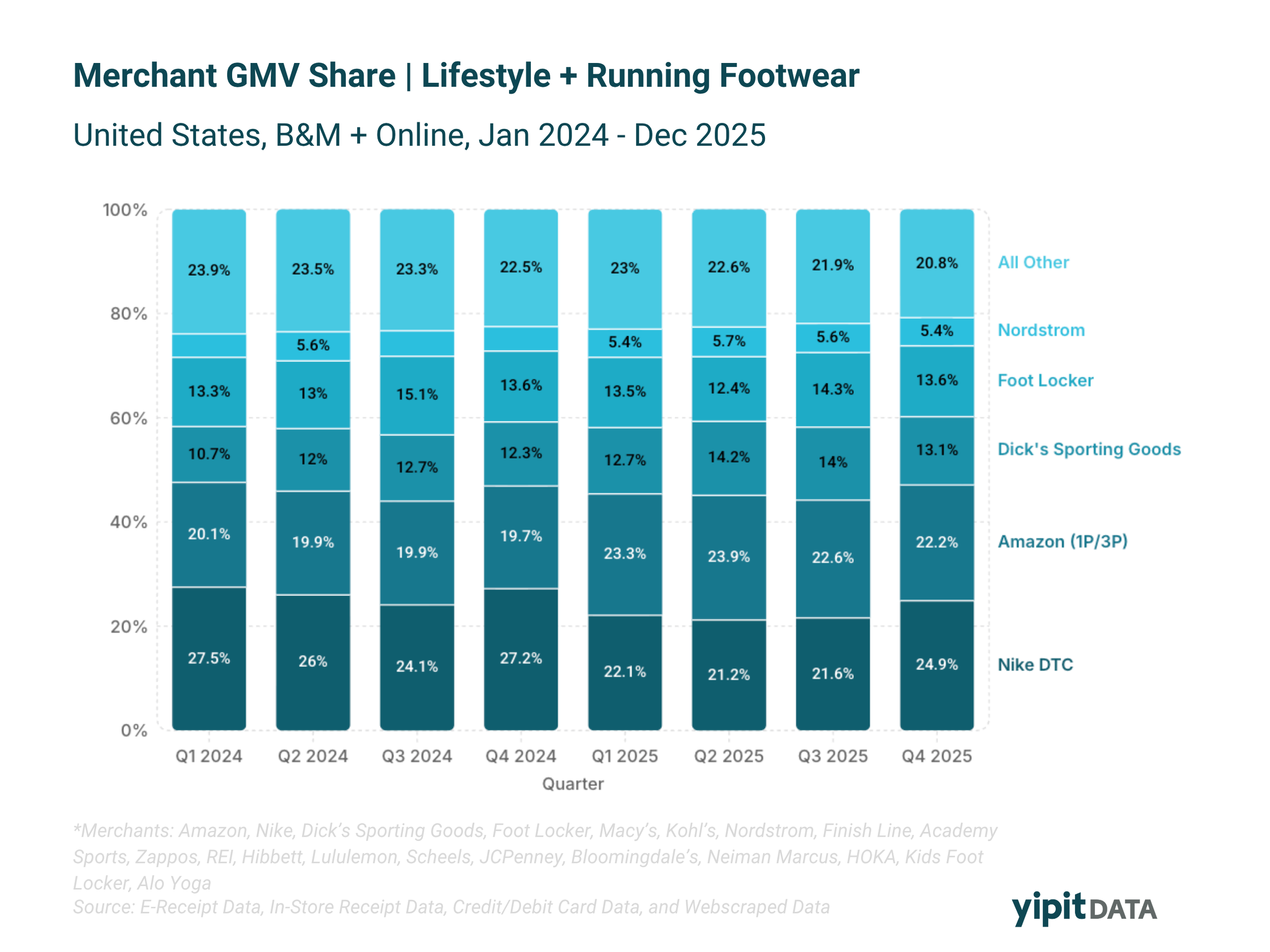

Market Share Is Shifting Across Retailers

Footwear market share continued to redistribute across major retail partners.

- Marketplace and wholesale players gained share

- Direct-to-consumer channels declined

Amazon and Dick’s Sporting Goods were among the retailers gaining share, while Nike’s direct channels trended downward. These changes reflect redistribution within the existing competitive set rather than expansion of new players.

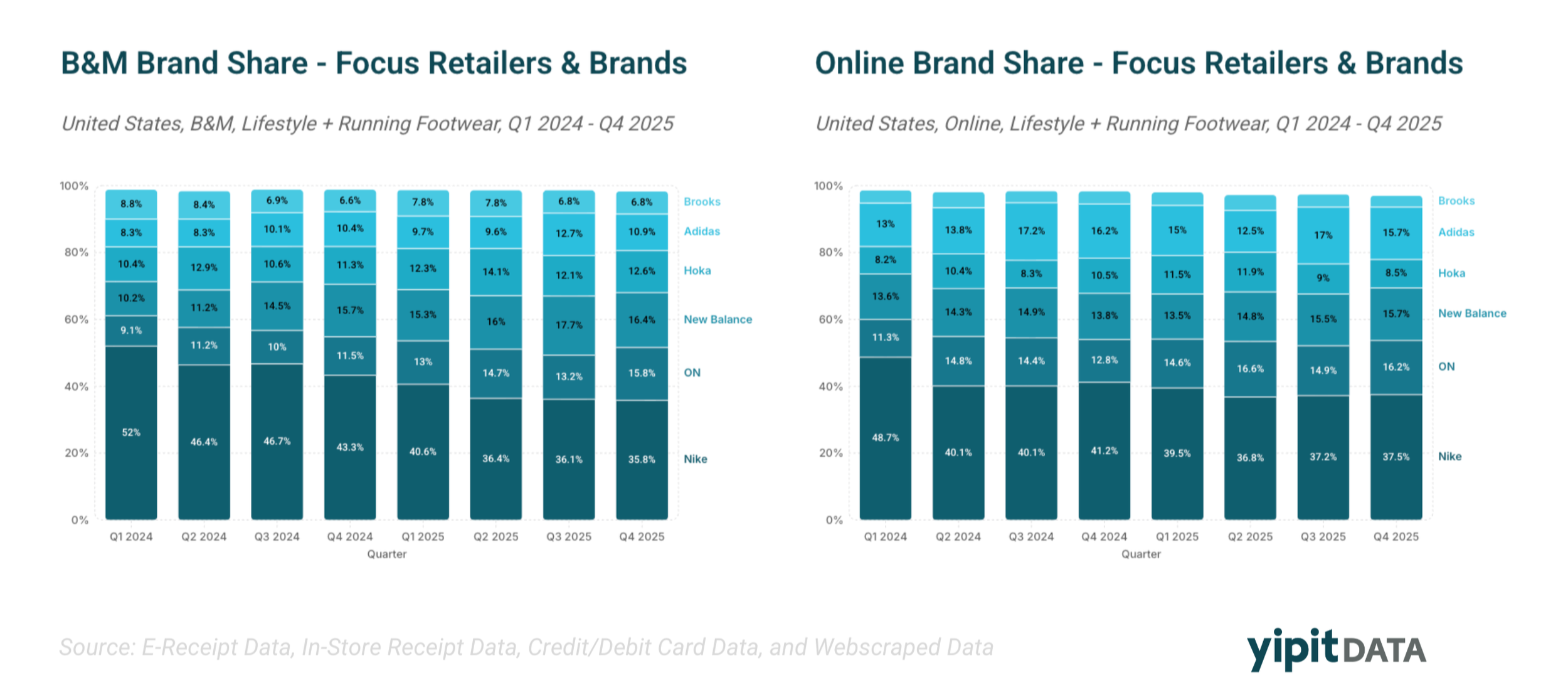

Nike Is Losing Share While Competition Fragments

Nike’s share declined across both in-store and online channels in 2025.

Rather than consolidating into a single competitor, this share shifted across multiple brands, indicating a more fragmented competitive landscape. Brands such as Hoka, ON, New Balance, and Adidas are participating in these gains.

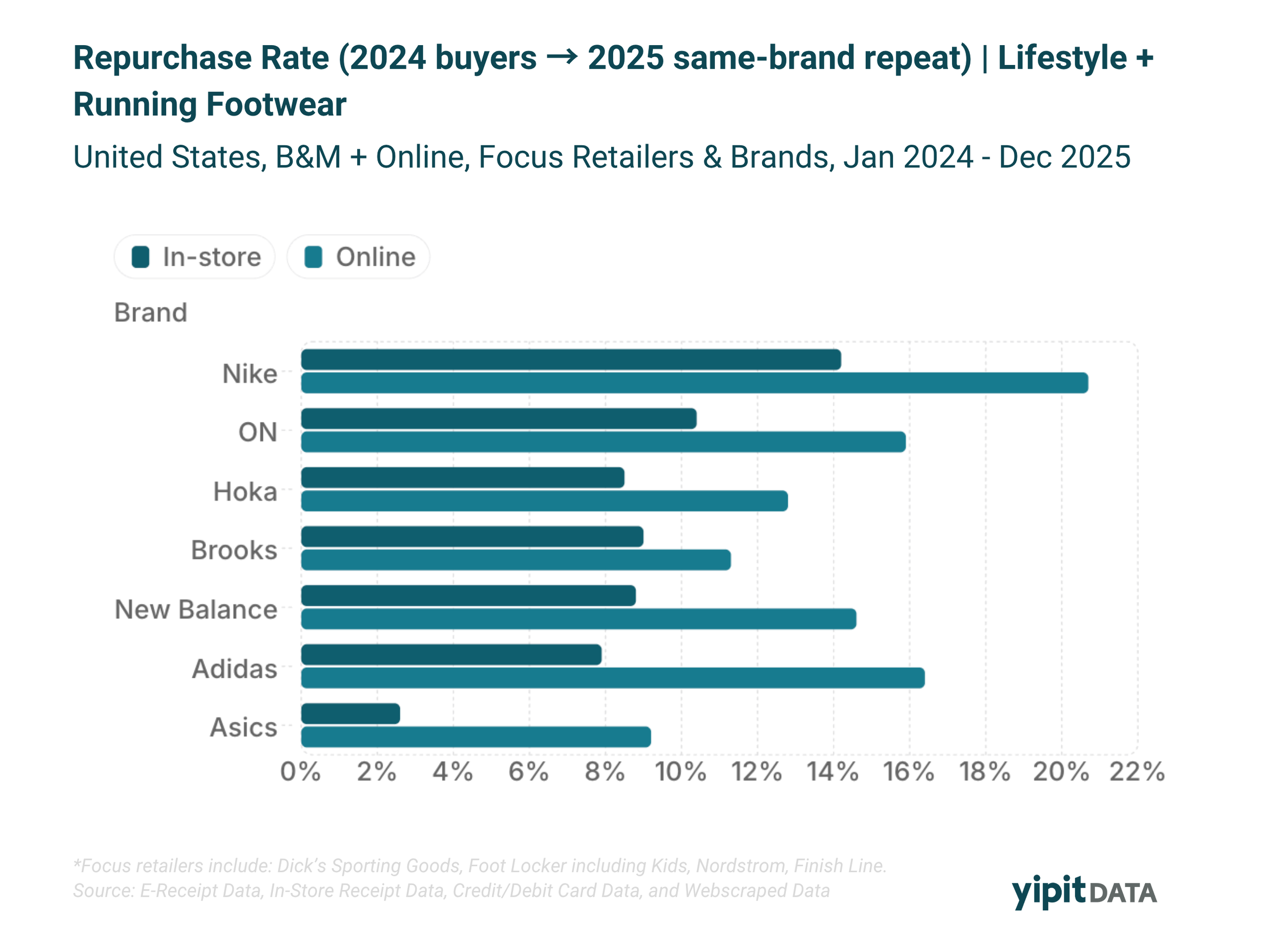

Customer Loyalty Varies Significantly by Brand

Retention metrics reveal clear differences in customer behavior across footwear brands.

- Nike leads in repurchase rates across channels

- ON, Adidas, and New Balance follow at lower but similar levels

- Hoka, Brooks, and Asics trail further below

A similar pattern appears in share of wallet, where Nike retains approximately half of customer spend, while other brands capture smaller portions.

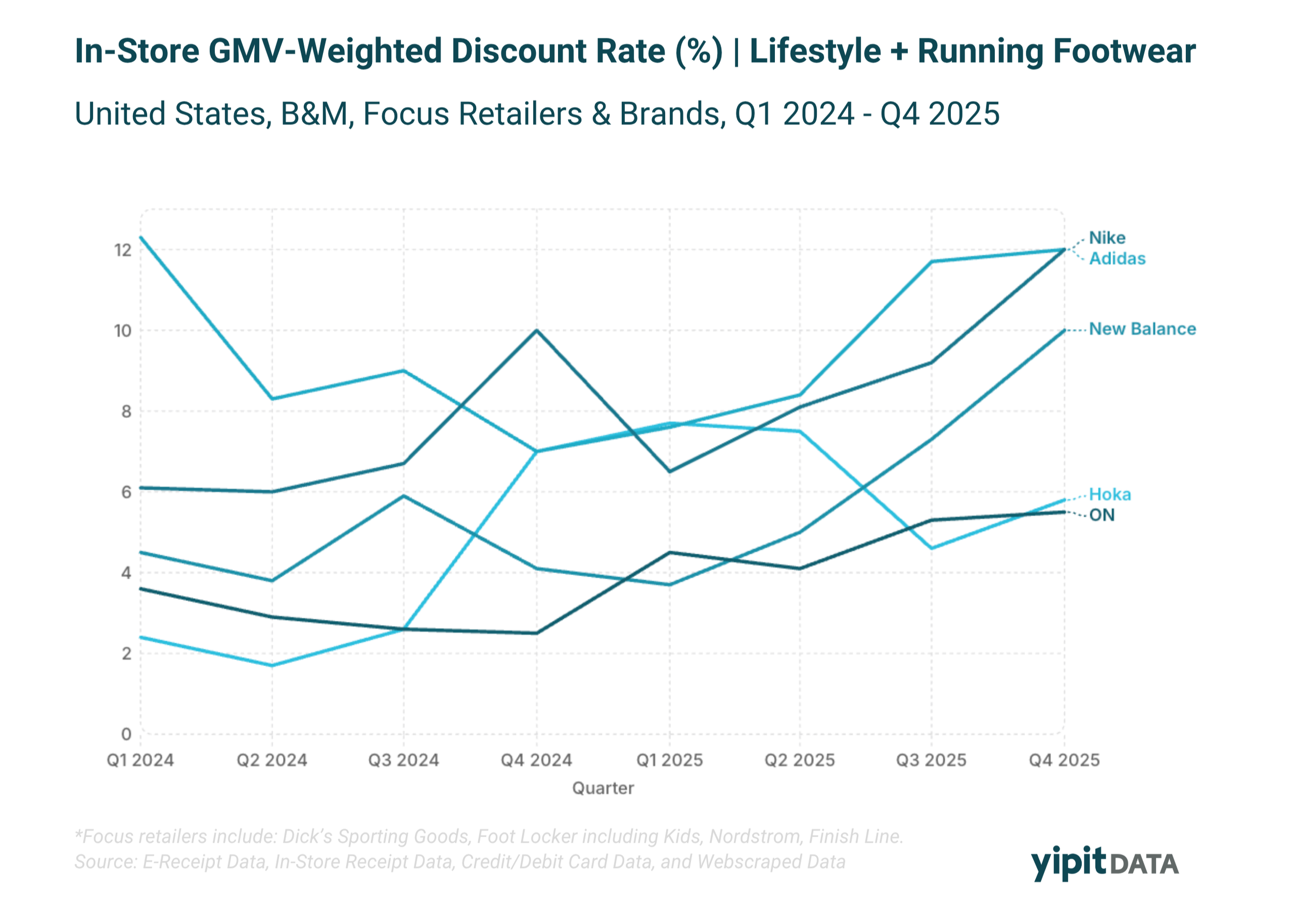

Discounting Increased Across the Market

Promotional activity expanded in 2025, particularly among major brands.

- Nike, Adidas, and New Balance increased discounting levels

- ON maintained lower discount rates relative to peers

This suggests variation in pricing strategies across brands, with some relying more heavily on promotions while others maintain more consistent pricing structures.

The footwear market in 2025 shows a clear shift in where growth is concentrated. Running footwear continues to outperform while lifestyle segments soften, and in-store sales are gaining momentum relative to online. At the same time, market share is redistributing across retailers and brands, with increased competition and more variation in customer retention and pricing strategies.

Understanding these shifts requires a detailed view of consumer behavior and channel dynamics. If you’re looking to go deeper into footwear and apparel trends or see how these changes impact your business, reach out to a YipitData analyst to learn more.

FAQ’s

- What does YipitData do for apparel brands?

- YipitData provides detailed market and shopper insights across apparel categories, including footwear, outerwear and activewear. Using transaction-level data, YipitData helps brands and retailers understand market share, category growth, and changing shopper behavior.

- What insights can brands get from apparel and footwear data analytics?

- Apparel and footwear data analytics can help brands understand category growth trends, identify shifts between online and in-store sales, track brand performance, and analyze customer retention. These insights are commonly used to monitor competitive positioning, evaluate pricing strategies, and understand changes in consumer spend across segments like running and lifestyle footwear.

- How does YipitData measure footwear and apparel market share?

- YipitData measures market share in apparel and footwear by analyzing aggregated transaction data across major retailers and brands. This includes both direct-to-consumer and wholesale channels, allowing for a comprehensive view of how market share shifts over time across key players like Nike, Adidas, and emerging brands.

- How can apparel and footwear brands use data to identify growth opportunities?

- Apparel and footwear brands can use data analytics to identify growth opportunities by analyzing category trends, tracking shifts in consumer demand, and monitoring performance across channels. Data can highlight which segments, such as running footwear or premium apparel, are growing faster, as well as where brands are gaining or losing share. This helps companies prioritize product categories, optimize distribution strategies, and better align with changing consumer spending patterns.

Speak to our Insights team

.svg)