How Kohl’s Grew it’s Customer Base with a Sephora Partnership

So far this year, Beauty leads all other product categories, including food, in H1 2023 sales growth. But Beauty’s popularity isn’t just a fleeting fad. Beauty retail sales at generalist retailers have experienced double-digit growth for the past 4 years, with Amazon dominating Walmart and Target in Beauty sales.

To defend against share loss to Amazon, in July 2021, Target launched a partnership with Ulta and committed to spread the shop-in-shop format to 800 stores. Then in August 2021, Kohl’s partnered with Ulta rival, Sephora, to launch a similar shop-in-shop experience. With two stores entering partnerships with Beauty retailers, we used our email and physical receipt panel to assess and evaluate each partnership’s impact on Beauty sales.

Beauty Basket Share

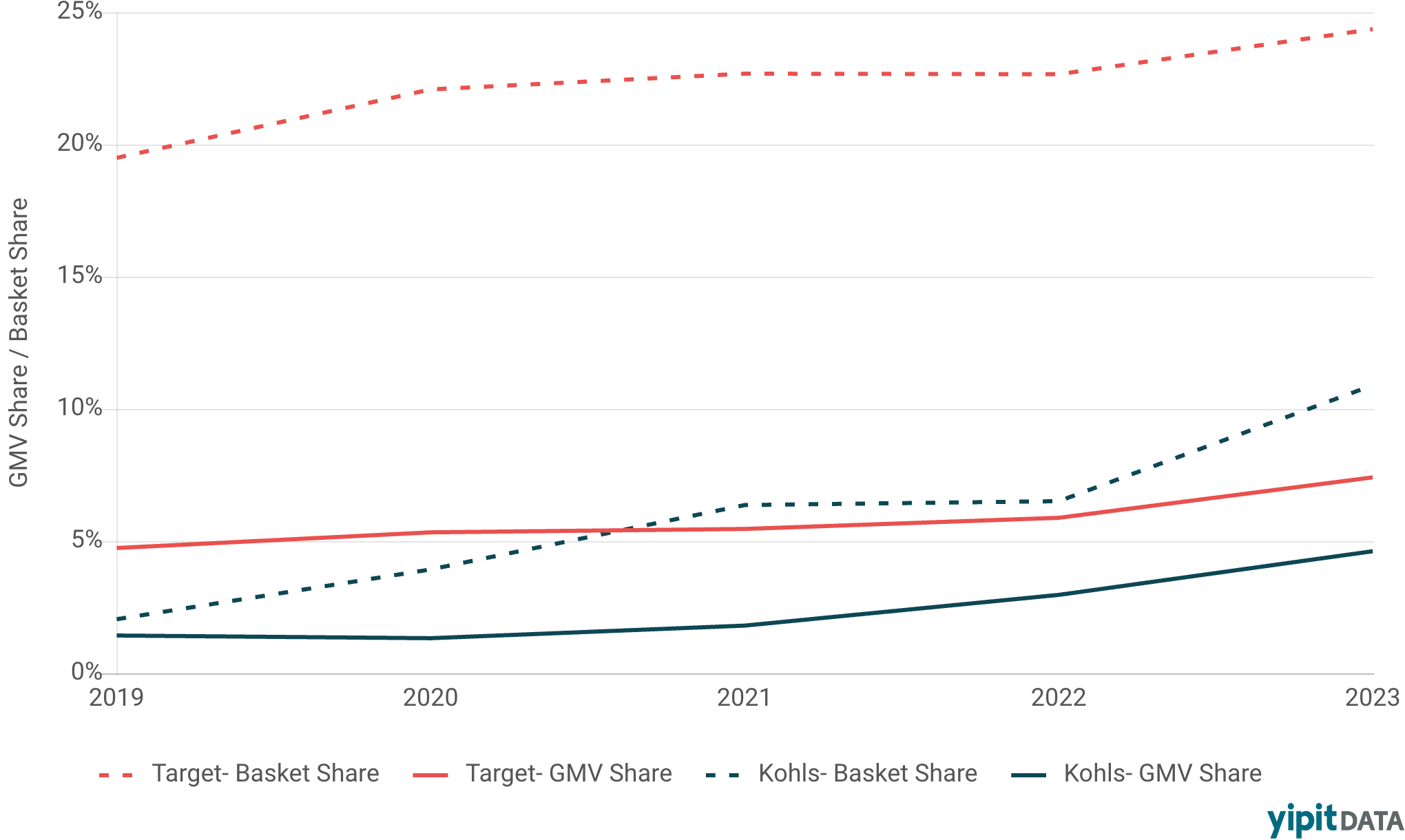

Although Beauty products are more frequently in Target baskets than Kohl’s, Kohl’s saw a more pronounced boost in Beauty basket share growing from 6.4% in 2021 to 10.9% in 2023 (+4.5 pp).

Beauty GMV Share and Basket Share, Target vs Kohl's

United States | Online and B&M Sales | H1 2019 - 2023

Target also saw an increase in the percentage of baskets containing Beauty products growing from 22.7% in 2021 to 24.3 % in 2023 (+1.6 pp).

Beauty GMV Share

GMV share saw similar trends, with Kohl’s experiencing more pronounced growth. Beauty GMV share at Kohl’s grew +2.8 pp from 1.8% in 2021 to 4.6% in 2023.However, Target Beauty GMV share grew only +1.9 pp from 5.5% in 2021 to 7.4% in 2023.

New Customers Who Shopped Beauty

So, which partnership was most successful in bringing in new customers to make a Beauty purchase? Using our receipt panels, we identified Kohl's shoppers that hadn’t shopped at Kohl’s prior to the partnership and who also made a Beauty purchase after the partnership launch. Impressively, the percentage of Kohl’s shoppers who fell into this “new customer - Beauty shopper” category, grew from 6.8% in 1Q 2022 to almost 13.7% just one year later (+6.9 pp).

Conversely, Target saw no significant growth in the “new customer - Beauty shopper” category since the launch of the Ulta partnership.

Kohl’s New Customers - Beauty Shopper (% of overall customers)

United States | Online and B&M Sales | 3Q 2021 - 1Q 2023

Overall, it seems Kohl’s is benefiting more than Target from their shop-in-shop Beauty partnership. Kohl’s relationship with Sephora is both growing their GMV and Order share of Beauty, in addition to bringing new customers Beauty shoppers through their doors.

Interested in understanding if your marketing initiatives are successfully recruiting new shoppers?

Sources: In-Store Receipt Data, Proprietary Email Receipt Data

Want to stay up to date on the latest trends in home improvement? Subscribe to our blog.