Is AI Replacing SaaS? Here’s What the Data Shows

.webp)

AI early adopters cut Asana and Monday.com spend by ~50%. But enterprise companies expanded it. YipitData's panel data reveals who's really replacing SaaS — and who isn't.

In this week’s B2B Spend Signals, we analyze how early AI adopters are reallocating software budgets across project management, customer support, and GTM tools using proprietary spend data from mid-market and enterprise companies.

This week, we tested a simple but powerful question: How are early AI adopters actually reallocating software spend?

AI adoption has triggered a wave of predictions about which categories of software will benefit and which may be disrupted. But speculation only goes so far. The more important question is what actual spending behavior looks like among companies already deploying AI at scale.

To answer that, we analyzed spending patterns among what we are calling AI Early Adopters, mid-market and enterprise companies with outsized and rapidly growing spend across a core set of AI vendors including OpenAI, Anthropic, Anysphere, Perplexity AI, and more. We then compared their software spend allocation against the rest of our panel. (See the “Data & Methodology” section at the bottom for more details.)

The goal: understand whether early AI adoption is replacing traditional SaaS spending or expanding it.

Here we examine three software categories often debated as the most vulnerable to AI, taking a magnifying glass to some of the largest vendors within each of these categories:

- Project management: Asana, Atlassian, monday.com

- Customer support: Zendesk, Intercom, Five9, Genesys

- Go to market: Sprout Social, Klaviyo, ZoomInfo

Project Management Software: Mid-Market Pressure, Enterprise Expansion

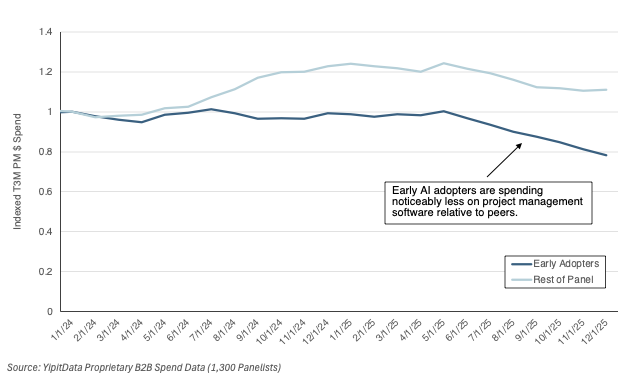

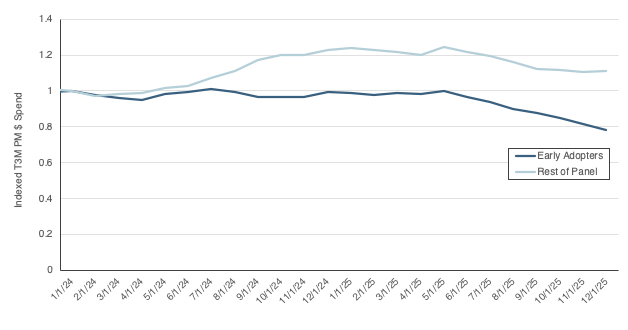

AI impact on B2B spend on Asana, Atlassian, and monday.com

Before examining the trends, it’s useful to validate the accuracy of the underlying spend data.

Across our panel of mid-market and enterprise companies, combined spend on Asana, Atlassian, and monday.com grew ~20% year-over-year in December 2025, closely tracking reported revenue growth of 22% year-over-year in 4Q25 across the three companies.

This alignment between spend data and reported results provides confidence that our panel reflects real market behavior.

Mid-market: AI adopters are reducing PM software spend

Among mid-market AI early adopters, project management software spending has been declining relative to peers.

While the broader mid-market panel has remained relatively stable, AI-intensive companies have been reallocating software budgets away from project management tools while significantly ramping spend on core AI platforms.

The decline in mid-market, early AI adopter spend across Asana, Atlassian, and monday.com has been steady over the course of 2025 and clearly under indexes relative to the rest of the panel.

Key trends Y/Y as of December 2025.

- Early AI adopters cut PM software allocation by ~50%

- The rest of the mid-market panel cut PM allocation by ~20% Y/Y

- Early AI adopters increased core AI spend by more than 300%

- The rest of the mid-market panel ramped core AI spend by ~120%.

Together, these trends suggest that among mid-sized companies, AI spending is directly competing with certain SaaS categories for budget allocation.

Enterprise: AI adopters are accelerating PM software spend

Interestingly, the pattern flips at the enterprise level.

Enterprise AI early adopters have expanded project management software spending, materially outpacing the rest of the panel.

This suggests that AI’s impact on PM SaaS changes significantly at scale.

Rather than reducing the need for PM software, AI has expanded the need for software that aids coordination among enterprises.

AI implementation may have enormous efficiency benefits but, so far, it has likely amplified operational complexity. As organizations deploy AI broadly, the need for coordination, visibility, and cross-functional orchestration software seems to have increased rather than declined.

Customer Support Software: Mid-market Expansion, Enterprise Stability

AI impact on B2B spend on Zendesk, Intercom, Five9, and Genesys

If the bear case is that AI agents will wipe out customer support software, the data does not support that — at least not yet.

Among mid-market AI early adopters, customer support software spend allocation generally expanded from 2024 to 2025, even as the rest of the mid-market panel pulled back. This could mean mid-market AI early adopters are higher growth companies with greater demand for customer support software even as demand among the rest of the panel tapers.

Among enterprise AI early adopters, customer support software spend allocation trends are not meaningfully different from the rest of the panel. The data is more volatile here, but generally shows no sustained difference in trend between AI early adopters and the rest of the panel. This may be because customer support stacks could be more embedded in larger enterprises, making them less reactive to early AI adoption.

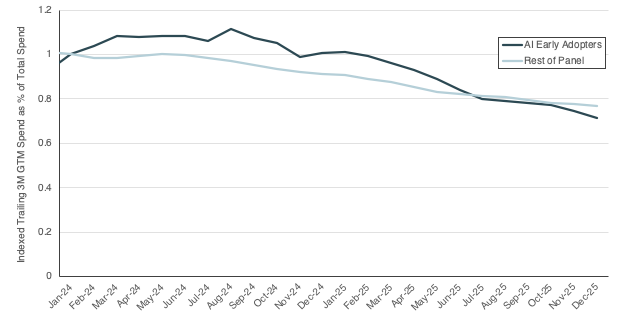

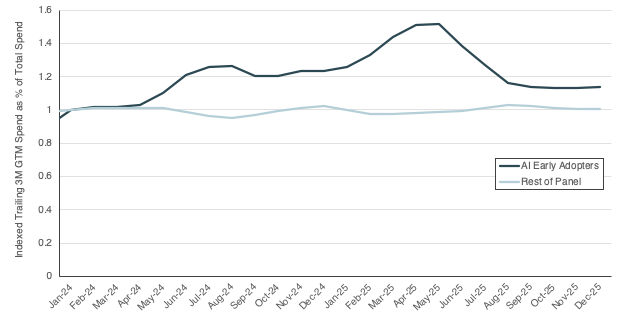

GTM Software: Mid-Market Stability; Slight Enterprise Expansion

AI impact on B2B spend on Sprout Social, Klaviyo, and ZoomInfo.

GTM software has been another category widely discussed as potentially vulnerable to AI disruption. But so far, the data shows little evidence of material change.

Among mid-market AI early adopters, GTM software spending trends have tracked closely with the rest of the panel.

Both groups trimmed GTM allocation slightly over the past several years, with no sustained divergence tied to AI adoption.

At the enterprise level, the data shows a slight increase in GTM spend allocation among AI adopters as compared to the rest of the panel. This could suggest that AI adoption is correlated with GTM budget expansion.

Data & Methodology Notes

Where is this data sourced from?

Data is sourced from our enterprise partners or comes from our panelists which are a cohort of companies that share anonymized data with us.

How large is the panel?

Mid-market panel size and selection: 900+ companies selected based on consistency and richness of data. The panel provides visibility into B2B software spend behavior among mid-sized businesses.}

Enterprise panel size and selection: 350+ enterprise companies selected to capture broad industry coverage and spend visibility across large organizations. The panel includes a meaningful sample of Fortune 1–500 companies, offering critical insights into large-scale software adoption.

How did you define the Early Adopter cohort?

We defined the group of AI Early Adopters as companies that met these conditions:

- In the top 50 by % Core AI spend allocation in December 2024. We use % of total software spend that is allocated to Core AI because it avoids biasing the cohort toward companies that simply have large budgets.

- Grew Core AI spend by at least 2x by December 2025. We’re looking for companies that were more than just experimenting with AI in a one-off kind of way but rather implemented and scaled AI adoption.

“Core AI” spend was defined as spend on this set of key AI companies: OpenAI, Anthropic, Anysphere (Cursor), Cohere, Mistral AI, Together AI, Fireworks AI, Hugging Face, Replicate Labs, Scale AI, Midjourney, ElevenLabs, Stability AI, and Perplexity AI.

This resulted in a set of 37 mid-market panelists and 18 enterprise panelists.

FAQ’S

- Is AI replacing SaaS software?

- The answer depends on company size and software category. YipitData analysis of 900+ mid-market companies shows AI early adopters cut project management software spending by ~50% year-over-year by December 2025. However, enterprise AI early adopters expanded PM software budgets as AI increased coordination complexity. Customer support and GTM software show no sustained decline in either segment as of December 2025.

- Are companies cutting Asana, Atlassian, and Monday.com spend because of AI?

- Among mid-market AI early adopters, yes — spending on these three vendors declined steadily through 2025, underperforming the broader panel. Enterprise AI early adopters showed the reverse: expanding PM software spend materially above the rest of the panel. YipitData panel spend grew ~20% YoY in December 2025, closely tracking the vendors' combined reported revenue growth of 22%.

- How much are AI early adopters increasing AI software spend?

- Mid-market AI early adopters increased core AI platform spend by more than 300% year-over-year by December 2025. The broader mid-market panel grew core AI spend by ~120% over the same period. Core AI vendors tracked include OpenAI, Anthropic, Anysphere (Cursor), Perplexity AI, and others.

- Is AI replacing customer support software like Zendesk and Intercom?

- Not yet, based on actual spend data. Mid-market AI early adopters expanded customer support software allocation from 2024 to 2025, while the broader mid-market panel pulled back. Enterprise AI early adopters showed no sustained difference from the rest of the panel as of December 2025.

- How did YipitData define AI Early Adopters for this analysis?

- AI Early Adopters were companies ranked in the top 50 by percentage of total software spend allocated to core AI in December 2024, who also grew core AI spend by at least 2x by December 2025. This produced 37 mid-market panelists and 18 enterprise panelists — companies that scaled AI adoption rather than simply experimenting with it.

Connect with us!

.svg)